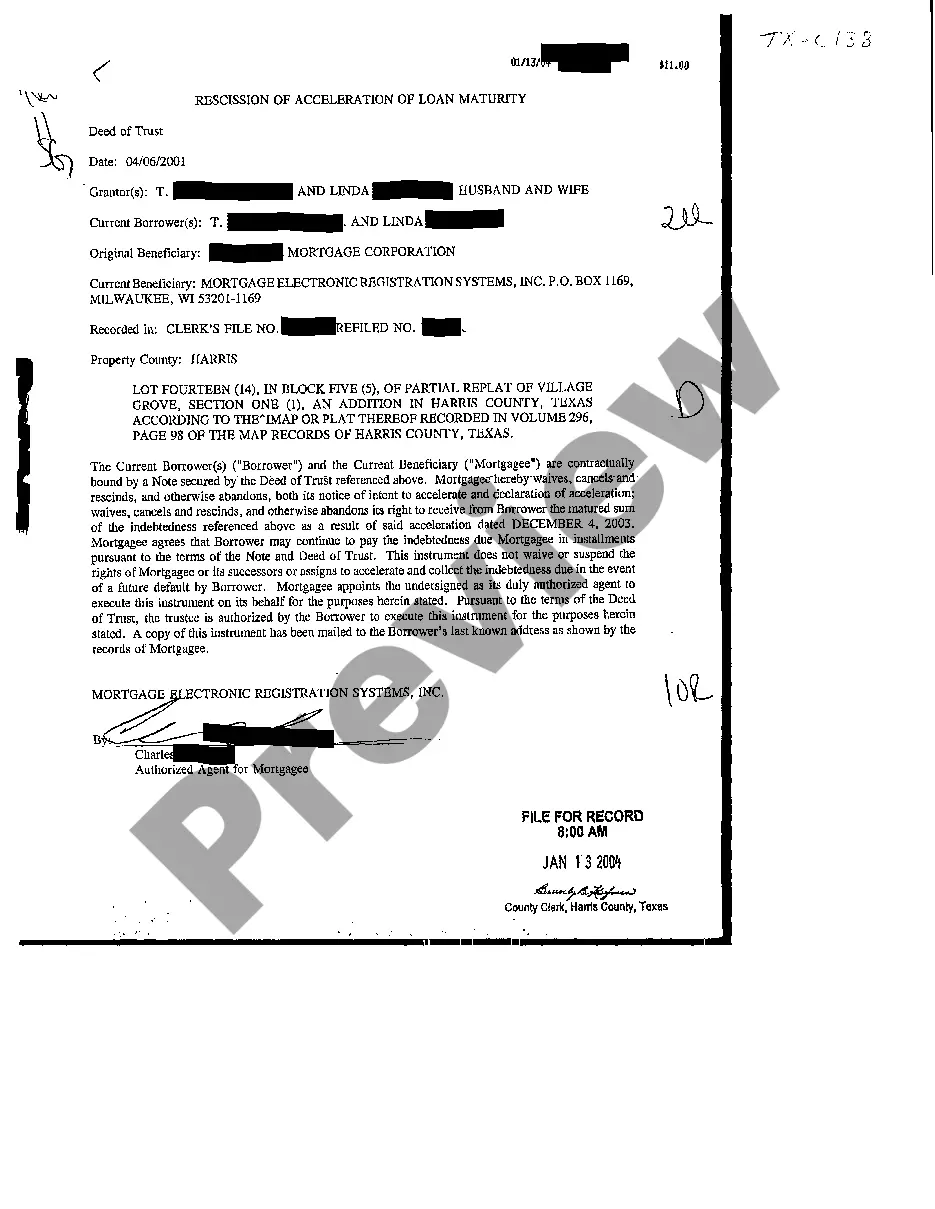

Harris Texas Rescission of Acceleration of Loan Maturity is a legal term used to describe the cancellation or reversal of a loan's accelerated maturity date in Harris County, Texas. When a loan is granted, it typically comes with a set maturity date, which is the date on which the borrower is required to fully repay the loan. However, certain circumstances may arise where the lender chooses to accelerate the maturity of the loan, meaning they demand immediate repayment of the outstanding balance. In such cases, the borrower may have the option to pursue a rescission of the acceleration, which essentially requests that the loan returns to its original repayment schedule. There are different types of Harris Texas Rescission of Acceleration of Loan Maturity, including: 1. Legal Actions: Borrowers may choose to challenge the acceleration through legal actions. This involves hiring an attorney who specializes in real estate or contract law to represent their interests in the matter. 2. Loan Modification: Instead of rescinding the acceleration entirely, borrowers may negotiate a loan modification with the lender. This could involve extending the loan term, reducing interest rates, or adjusting the repayment schedule to make it more manageable for the borrower. 3. Mediation or Arbitration: In some cases, borrowers and lenders may opt for mediation or arbitration to resolve the acceleration dispute. This involves bringing in a neutral third party to facilitate discussions and help both parties come to a mutually acceptable agreement. 4. Compliance with Loan Terms: In certain situations, borrowers can pursue a rescission by proving that they have met the conditions specified in the loan agreement. If the lender has wrongly accelerated the maturity date, the borrower can present evidence demonstrating their compliance with the loan terms to seek a rescission. Overall, Harris Texas Rescission of Acceleration of Loan Maturity refers to the process of undoing the acceleration of a loan's maturity date in Harris County, Texas. It involves various strategies such as legal actions, loan modifications, mediation, or proving compliance with loan terms to reach a satisfactory resolution between the borrower and lender.

Harris Texas Rescission of Acceleration of Loan Maturity

Description

How to fill out Harris Texas Rescission Of Acceleration Of Loan Maturity?

Regardless of social or professional status, completing law-related documents is an unfortunate necessity in today’s world. Too often, it’s practically impossible for a person with no law education to draft such paperwork cfrom the ground up, mainly because of the convoluted terminology and legal nuances they come with. This is where US Legal Forms comes to the rescue. Our service offers a huge library with more than 85,000 ready-to-use state-specific documents that work for almost any legal case. US Legal Forms also is an excellent asset for associates or legal counsels who want to to be more efficient time-wise utilizing our DYI tpapers.

Whether you need the Harris Texas Rescission of Acceleration of Loan Maturity or any other document that will be valid in your state or county, with US Legal Forms, everything is at your fingertips. Here’s how to get the Harris Texas Rescission of Acceleration of Loan Maturity in minutes employing our reliable service. If you are presently a subscriber, you can go on and log in to your account to get the appropriate form.

Nevertheless, if you are a novice to our platform, ensure that you follow these steps prior to obtaining the Harris Texas Rescission of Acceleration of Loan Maturity:

- Ensure the form you have found is good for your area considering that the regulations of one state or county do not work for another state or county.

- Review the document and go through a short outline (if provided) of cases the paper can be used for.

- In case the form you picked doesn’t suit your needs, you can start again and look for the needed document.

- Click Buy now and choose the subscription plan that suits you the best.

- with your credentials or create one from scratch.

- Choose the payment method and proceed to download the Harris Texas Rescission of Acceleration of Loan Maturity as soon as the payment is completed.

You’re good to go! Now you can go on and print out the document or fill it out online. If you have any problems getting your purchased documents, you can easily access them in the My Forms tab.

Whatever situation you’re trying to solve, US Legal Forms has got you covered. Try it out today and see for yourself.