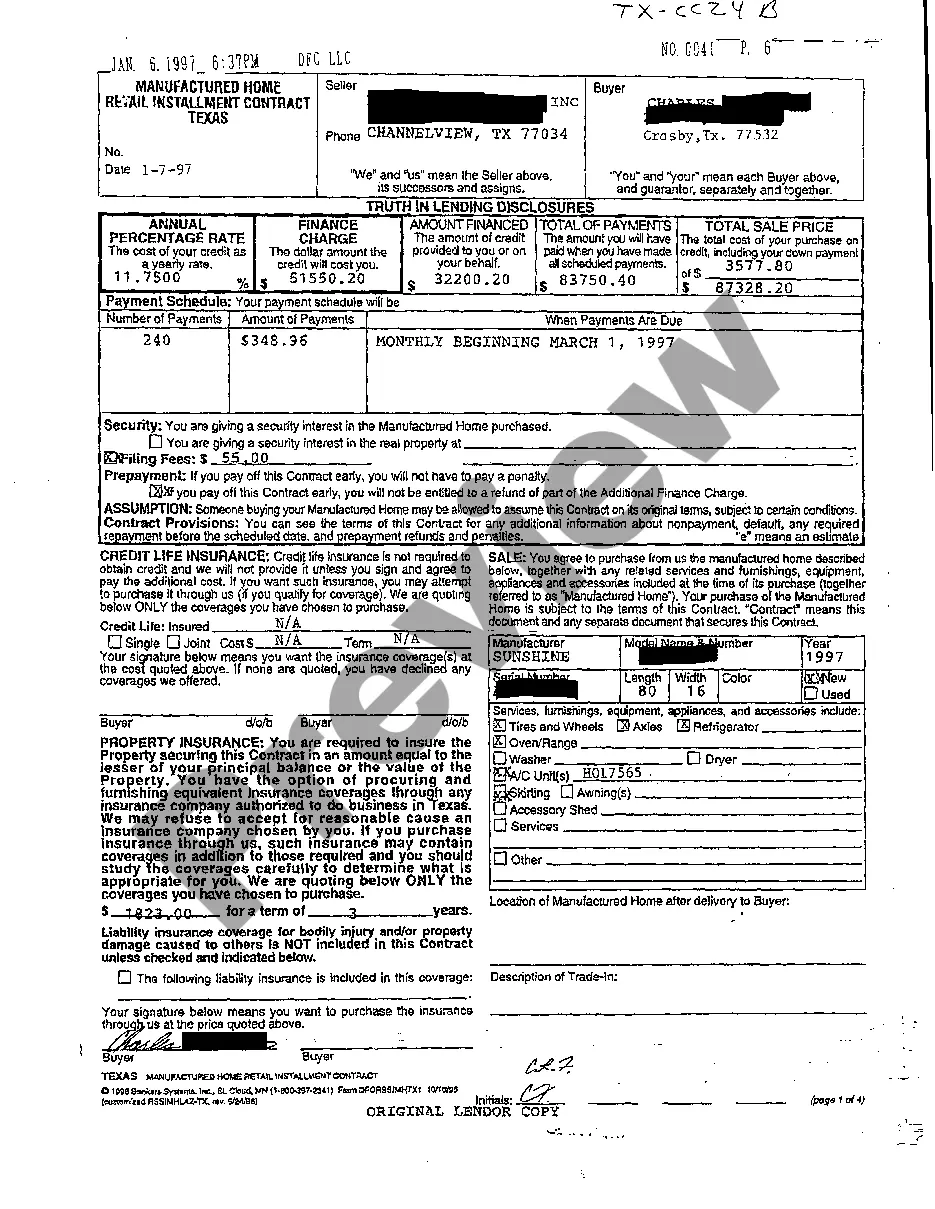

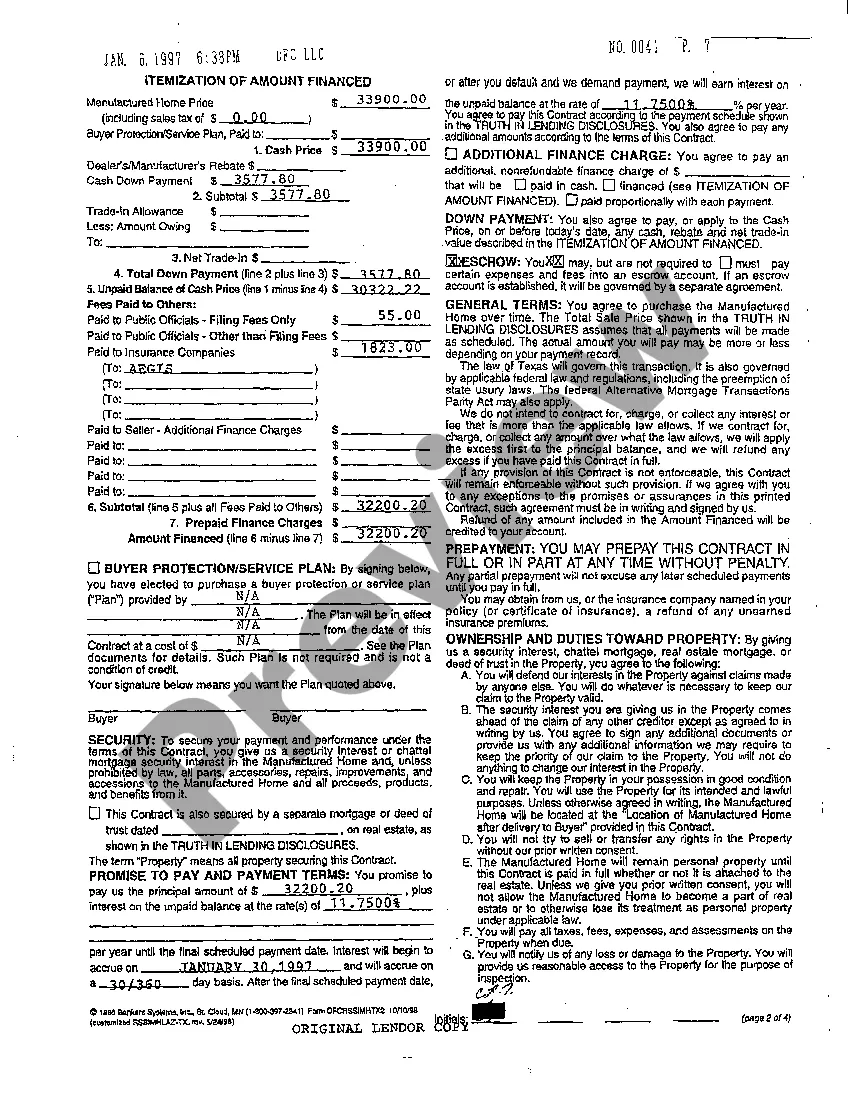

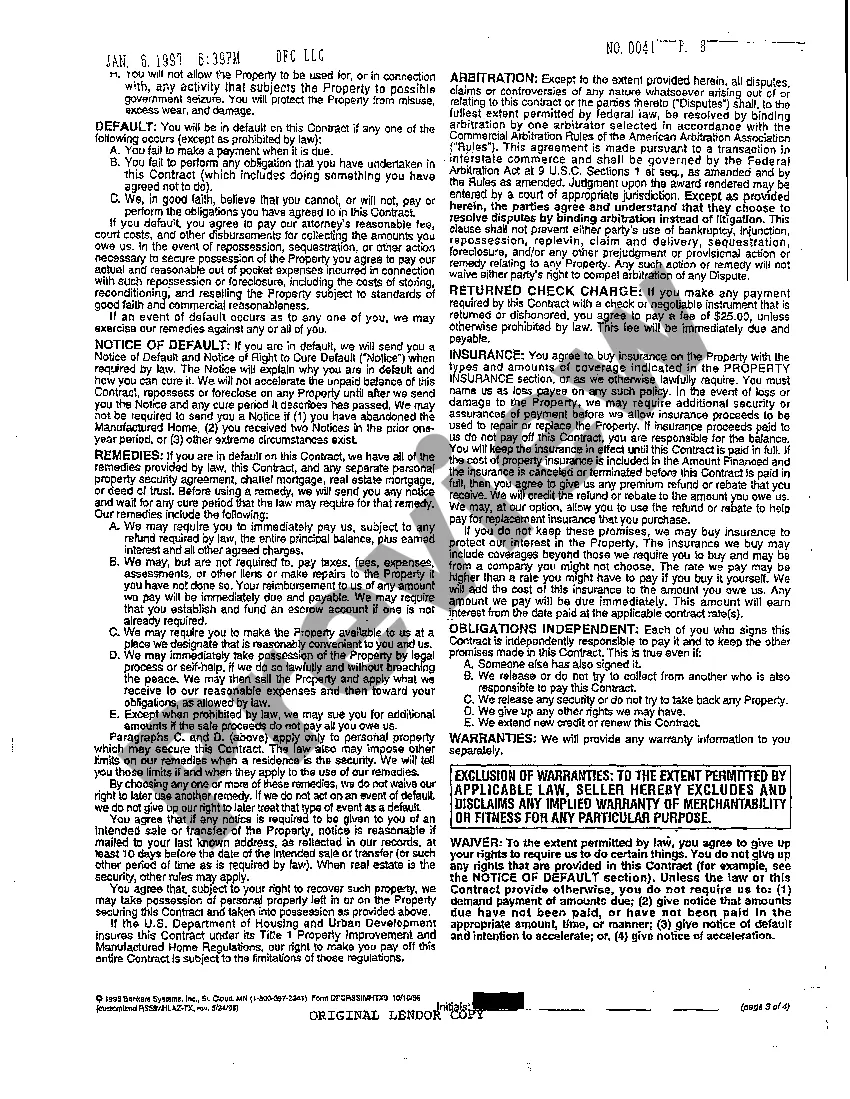

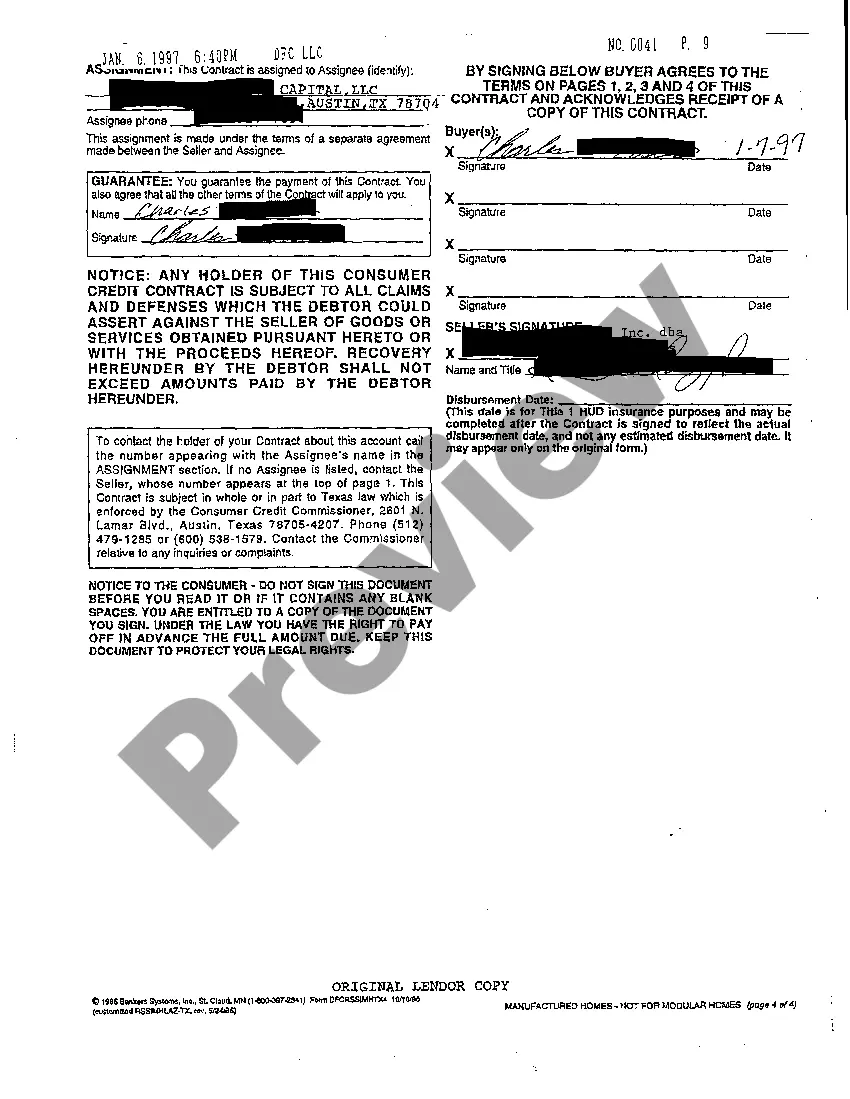

The Fort Worth Texas Truth In Lending Disclosures refer to the set of regulations implemented by the state of Texas under the Truth in Lending Act to ensure transparency and consumer protection in lending transactions. These disclosures aim to provide borrowers with accurate information regarding the terms and costs associated with a loan or credit agreement, allowing them to make informed decisions. The Truth In Lending Disclosures in Fort Worth Texas require lenders to provide certain key information to borrowers. This includes the annual percentage rate (APR), which represents the cost of credit expressed as a yearly interest rate. The APR enables borrowers to compare different loan offers and understand the total cost of borrowing, including interest rates and fees. In addition to the APR, the Truth In Lending Disclosures mandate the disclosure of other crucial details of the loan, such as the total amount financed, finance charges, payment schedule, and any prepayment penalties. These disclosures also include information on late fees, grace periods, and the total number of payments required to repay the loan. It is worth noting that the Fort Worth Texas Truth In Lending Disclosures may vary depending on the type of loan or credit agreement. Here are some of the common types of disclosures: 1. Closed-end loans: These are loans with a fixed repayment schedule, such as personal loans or auto loans. For closed-end loans, the disclosure requirements include the total amount financed, finance charges, and the total payment amount. 2. Open-end credit: This refers to revolving lines of credit, such as credit cards or home equity lines of credit (Helots). The Truth In Lending Disclosures for open-end credit include the periodic rate, which is the interest rate charged on the outstanding balance, and the method used to calculate the finance charges. 3. Mortgage loans: Mortgage loans have their own set of specific Truth In Lending Disclosures known as the TILA-RESPA Integrated Disclosure (TRIED). This includes the Loan Estimate, a document provided within three business days of applying for a mortgage, and the Closing Disclosure, which details the final loan terms and costs, provided at least three business days before the loan closing. By having these disclosures readily available, Fort Worth Texas borrowers can evaluate different loan offers, understand the true cost of borrowing, and make informed decisions that align with their financial goals. These regulations play a crucial role in promoting transparency, fairness, and consumer protection in lending transactions.

Fort Worth Texas Truth In Lending Disclosures

Description

How to fill out Fort Worth Texas Truth In Lending Disclosures?

No matter the social or professional status, filling out legal documents is an unfortunate necessity in today’s world. Very often, it’s virtually impossible for someone without any legal background to draft this sort of paperwork from scratch, mostly because of the convoluted terminology and legal subtleties they entail. This is where US Legal Forms comes to the rescue. Our platform offers a huge catalog with more than 85,000 ready-to-use state-specific documents that work for almost any legal case. US Legal Forms also serves as an excellent resource for associates or legal counsels who want to to be more efficient time-wise utilizing our DYI forms.

Whether you need the Fort Worth Texas Truth In Lending Disclosures or any other paperwork that will be valid in your state or county, with US Legal Forms, everything is at your fingertips. Here’s how you can get the Fort Worth Texas Truth In Lending Disclosures quickly using our trusted platform. In case you are presently an existing customer, you can go on and log in to your account to download the appropriate form.

However, in case you are unfamiliar with our platform, make sure to follow these steps before downloading the Fort Worth Texas Truth In Lending Disclosures:

- Be sure the form you have found is specific to your location since the rules of one state or county do not work for another state or county.

- Review the form and read a quick description (if provided) of cases the document can be used for.

- In case the one you picked doesn’t suit your needs, you can start over and search for the necessary form.

- Click Buy now and pick the subscription plan you prefer the best.

- with your login information or register for one from scratch.

- Pick the payment gateway and proceed to download the Fort Worth Texas Truth In Lending Disclosures as soon as the payment is completed.

You’re all set! Now you can go on and print the form or complete it online. In case you have any issues locating your purchased documents, you can easily access them in the My Forms tab.

Whatever situation you’re trying to sort out, US Legal Forms has got you covered. Give it a try today and see for yourself.