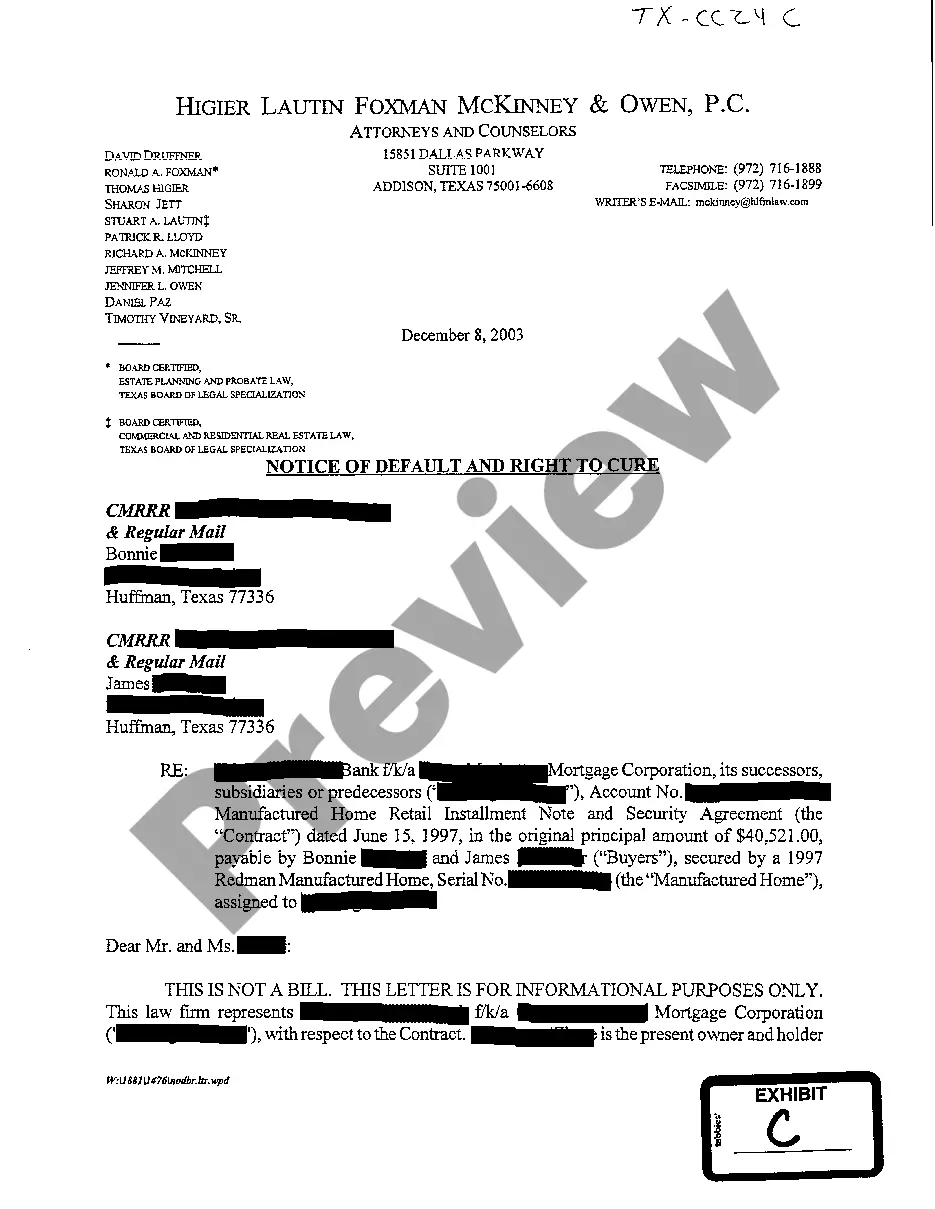

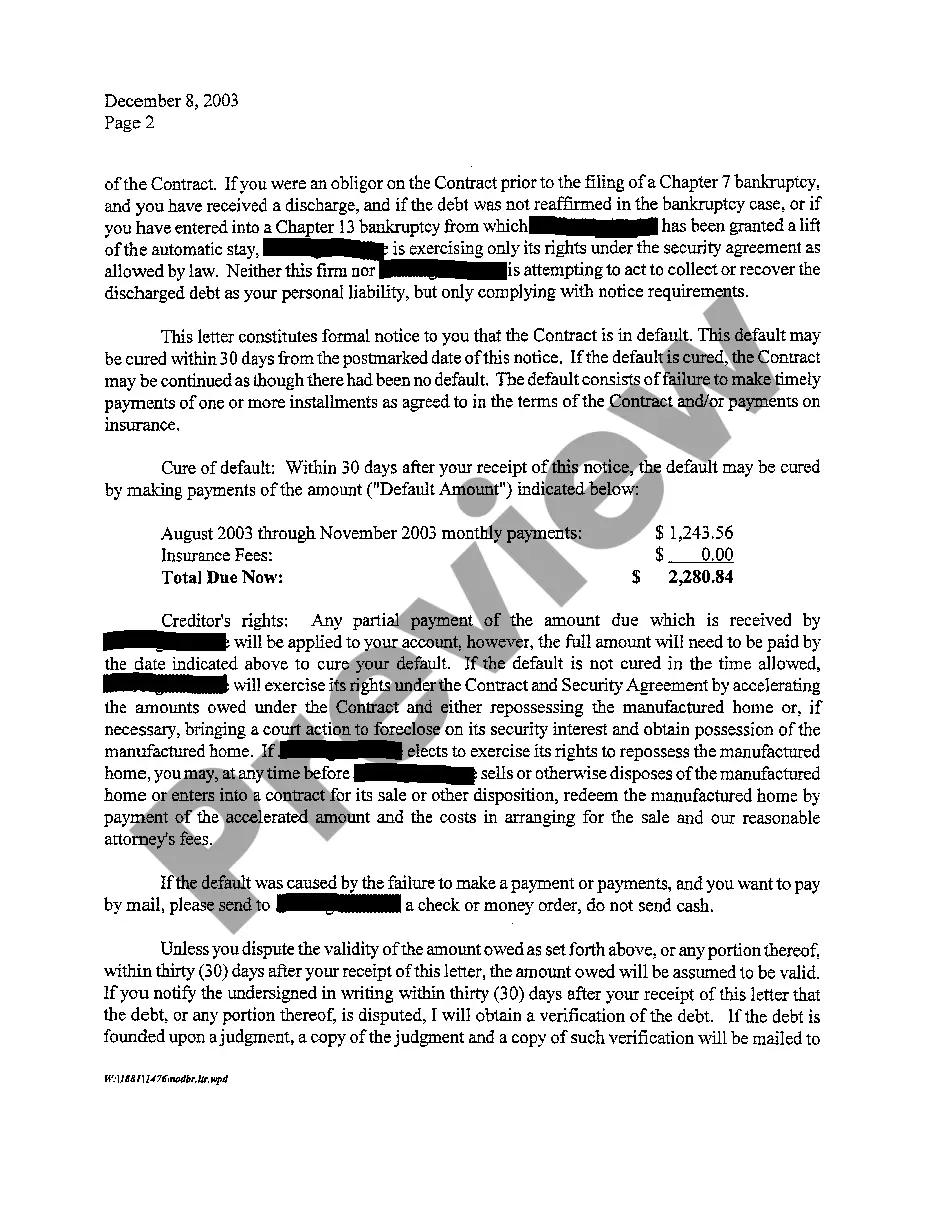

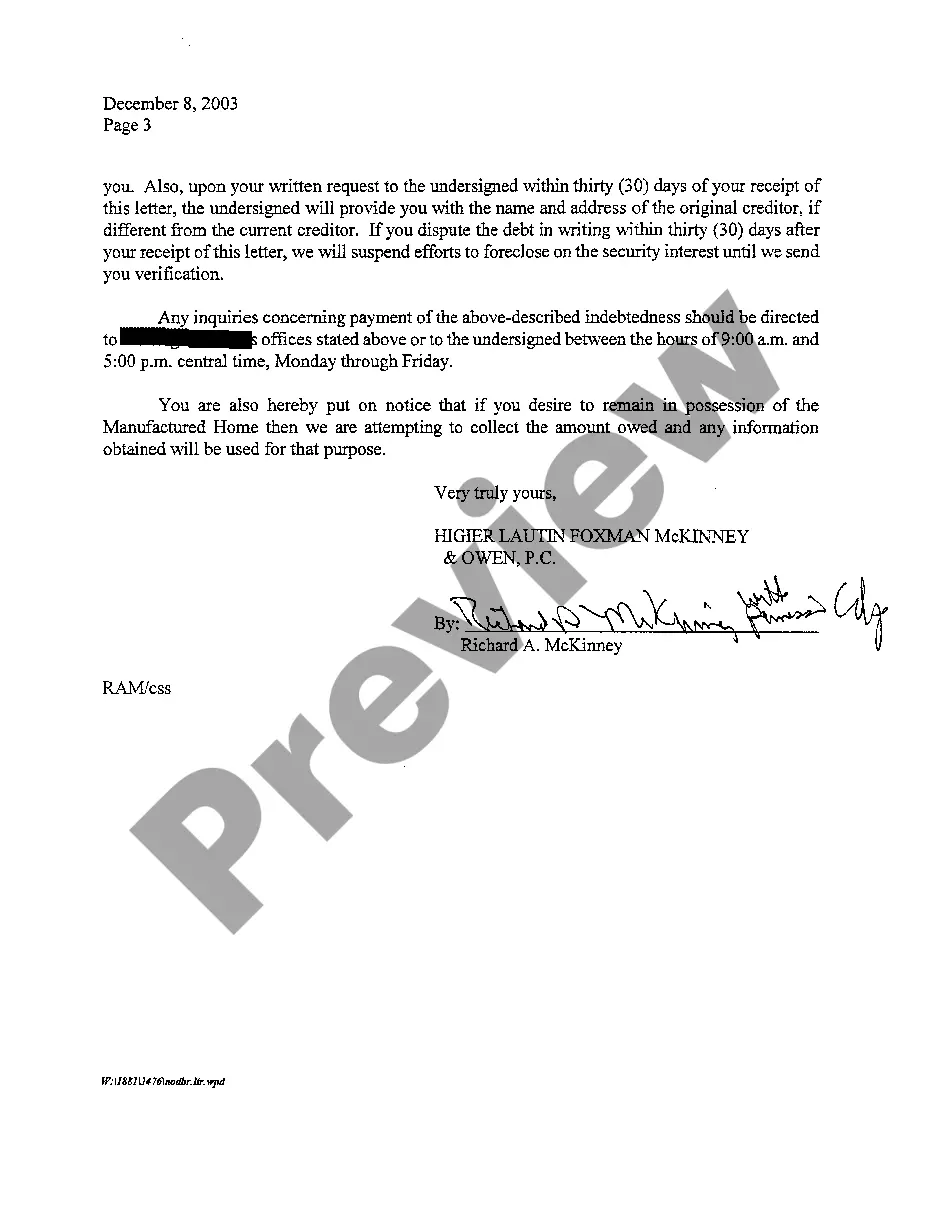

College Station Texas Notice of Default and Right To Cure is an important legal document that serves as a warning to borrowers about their delinquent mortgage payments. It outlines the lender's intention to initiate foreclosure proceedings if the outstanding balance is not settled promptly. The notice also explains the borrower's right to cure the default by bringing their payments up to date within a specified time period. In College Station, Texas, there are two types of Notice of Default and Right To Cure: the formal Notice of Default and the Notice of Right To Cure. The formal Notice of Default is typically sent by the lender when a borrower fails to make payments on their mortgage for a specific period. This notice provides a detailed account of the amount owed, including principal, interest, late fees, penalties, and any other applicable charges. It states the consequences of non-payment and notifies the homeowner of their right to cure the default before foreclosure proceedings begin. On the other hand, the Notice of Right To Cure is issued by the lender when the borrower has fallen behind on their mortgage payments and seeks to inform them of their right to remedy the default in a shorter timeframe. This notice specifies the total amount owed, including any outstanding fees, and outlines the steps the borrower must take to cure the default within a specific period, which is often shorter than that stated in the formal Notice of Default. As per College Station, Texas regulations, borrowers are typically allowed a minimum period of 20 days to cure the default mentioned in the Notice of Default. However, this timeframe may vary depending on the individual mortgage contract terms and the lender's policies. It is crucial for borrowers to respond promptly and take necessary actions to address the default within the given time frame in order to avoid foreclosure. In conclusion, the College Station Texas Notice of Default and Right To Cure is a critical document that lenders utilize to initiate foreclosure proceedings due to delinquent mortgage payments. It notifies borrowers of their outstanding debt and provides them with an opportunity to cure the default before foreclosure is pursued. Borrowers must carefully review the notice, understand their rights, and promptly take the necessary actions to rectify their default in accordance with the specified time frame.

College Station Texas Notice of Default and Right To Cure

Description

How to fill out College Station Texas Notice Of Default And Right To Cure?

Finding verified templates specific to your local laws can be challenging unless you use the US Legal Forms library. It’s an online collection of more than 85,000 legal forms for both individual and professional needs and any real-life scenarios. All the documents are properly categorized by area of usage and jurisdiction areas, so searching for the College Station Texas Notice of Default and Right To Cure becomes as quick and easy as ABC.

For everyone already acquainted with our catalogue and has used it before, obtaining the College Station Texas Notice of Default and Right To Cure takes just a couple of clicks. All you need to do is log in to your account, select the document, and click Download to save it on your device. This process will take just a couple of additional steps to make for new users.

Adhere to the guidelines below to get started with the most extensive online form collection:

- Check the Preview mode and form description. Make sure you’ve selected the correct one that meets your needs and fully corresponds to your local jurisdiction requirements.

- Look for another template, if needed. Once you find any inconsistency, use the Search tab above to find the right one. If it suits you, move to the next step.

- Buy the document. Click on the Buy Now button and choose the subscription plan you prefer. You should create an account to get access to the library’s resources.

- Make your purchase. Give your credit card details or use your PayPal account to pay for the subscription.

- Download the College Station Texas Notice of Default and Right To Cure. Save the template on your device to proceed with its completion and obtain access to it in the My Forms menu of your profile whenever you need it again.

Keeping paperwork neat and compliant with the law requirements has major importance. Take advantage of the US Legal Forms library to always have essential document templates for any needs just at your hand!