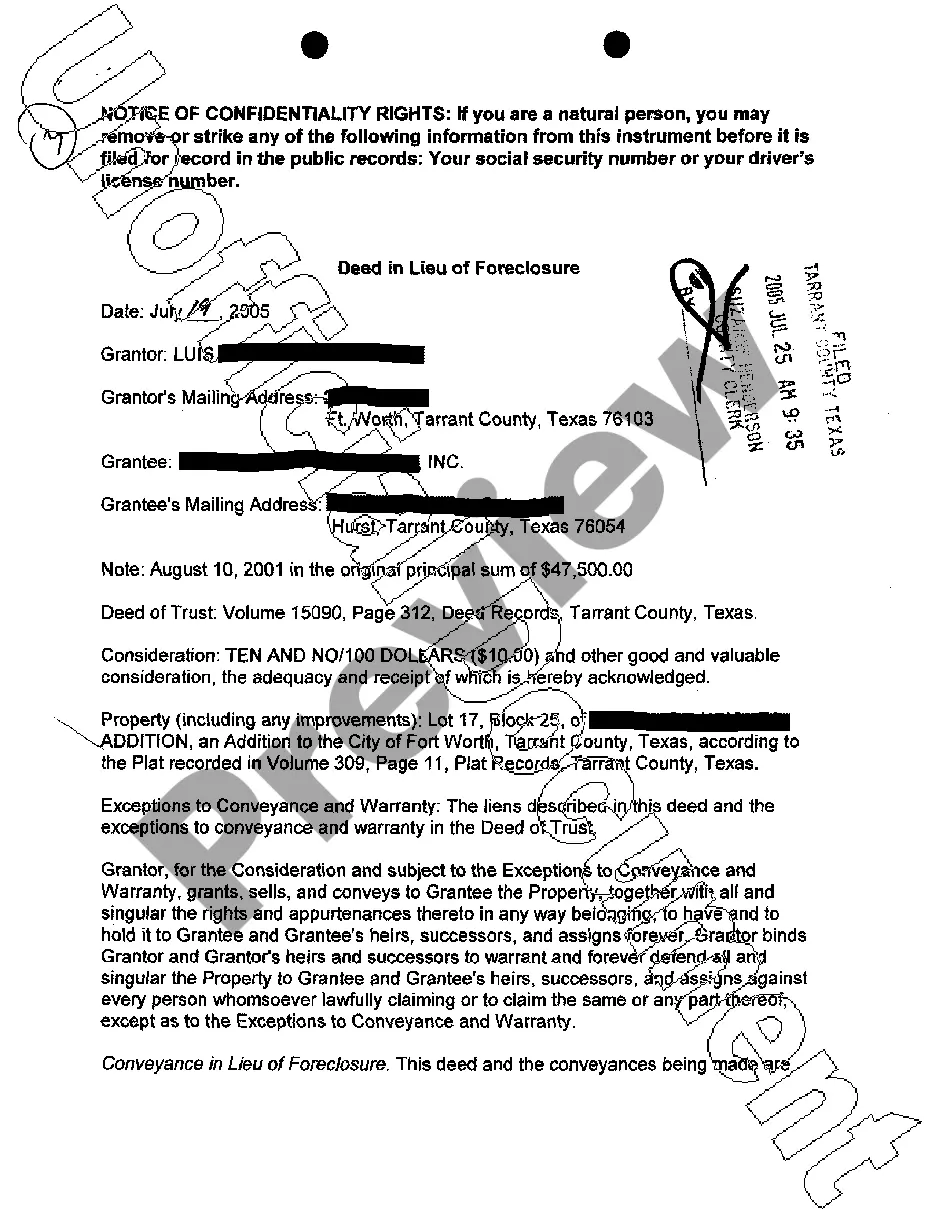

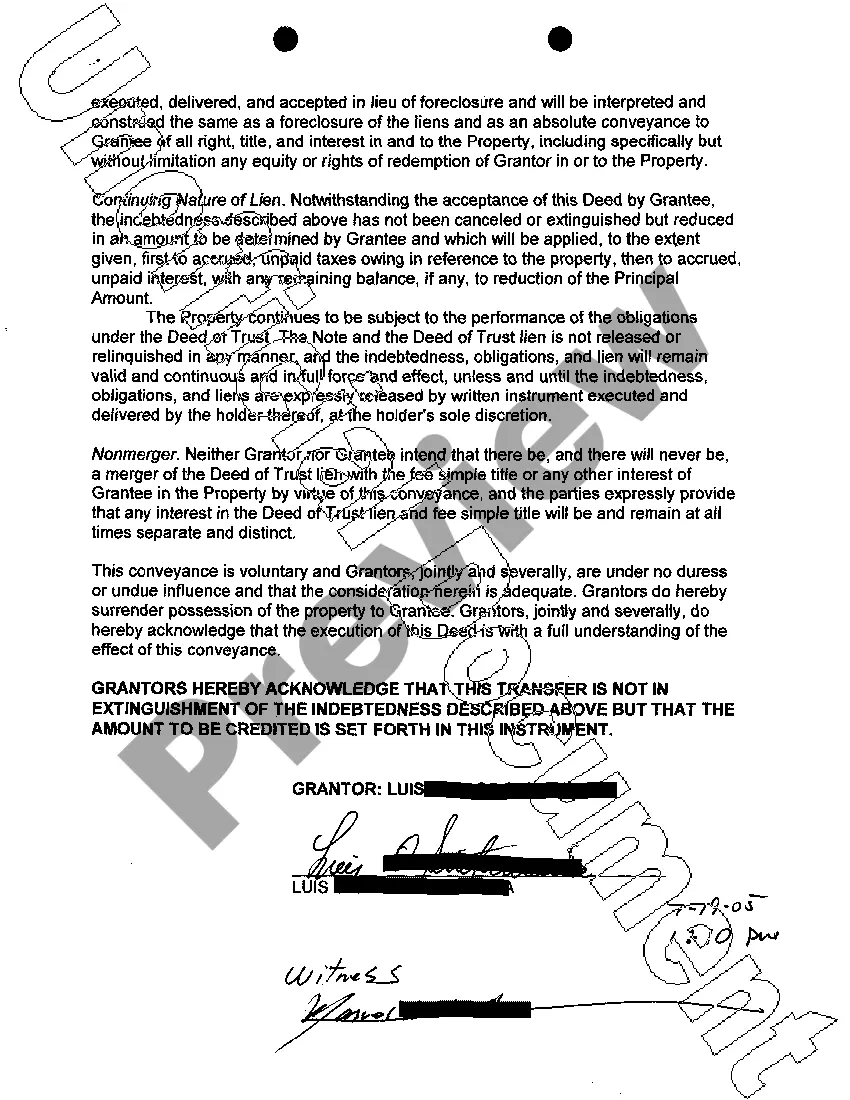

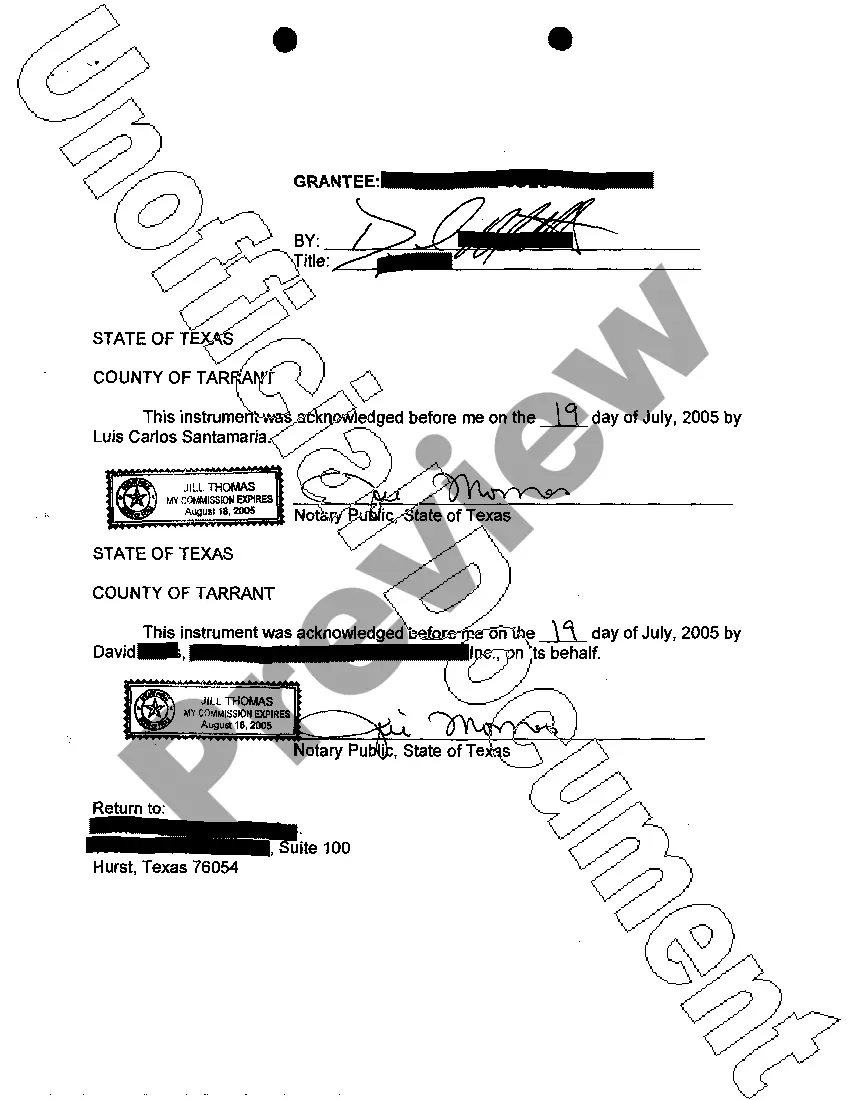

Killeen Texas Deed in Lieu of Foreclosure is a legal option available to homeowners who are facing foreclosure and are willing to voluntarily transfer the ownership of their property to the lender in exchange for the cancellation of their mortgage debt. This can be a viable alternative to foreclosure, providing homeowners with an opportunity to avoid the negative consequences associated with a foreclosure on their credit history. In a Killeen Texas Deed in Lieu of Foreclosure, the homeowner surrenders the property to the lender, who then takes ownership without going through the foreclosure process. This option allows the homeowner to avoid the time-consuming and costly foreclosure process and can provide them with a fresh start. It is important to note that this option is typically only available if the property's value is less than the outstanding loan balance and if the lender agrees to accept the deed. No two Killeen Texas Deed in Lieu of Foreclosure cases are exactly alike, as each situation is unique. However, there are a few variations that homeowners may encounter: 1. Traditional Deed in Lieu of Foreclosure: This is the standard option where the homeowner voluntarily transfers the property and the lender cancels the mortgage debt in return. 2. Cash for Keys: In some cases, lenders may offer homeowners cash incentives to leave the property quickly and in good condition. This option allows homeowners to receive a monetary payment in addition to the cancellation of their mortgage debt. 3. Relocation Assistance: In certain circumstances, the lender may also offer assistance to the homeowner in finding a new place of residence or cover moving expenses to facilitate a smooth transition. 4. Deficiency Waiver: In a Killeen Texas Deed in Lieu of Foreclosure, the lender may agree to waive any deficiency balance remaining after the property is sold. This can provide homeowners with further financial relief. It is crucial for homeowners considering a Killeen Texas Deed in Lieu of Foreclosure to consult with an experienced real estate attorney or a housing counselor to understand the legal implications and potential tax consequences associated with this option. Experts can provide guidance based on individual circumstances and negotiate on behalf of homeowners to ensure the best possible outcome.

Killeen Texas Deed in Lieu of Foreclosure

Description

How to fill out Killeen Texas Deed In Lieu Of Foreclosure?

Regardless of social or professional status, filling out law-related documents is an unfortunate necessity in today’s professional environment. Too often, it’s practically impossible for someone with no legal education to draft this sort of paperwork cfrom the ground up, mainly because of the convoluted jargon and legal subtleties they involve. This is where US Legal Forms comes to the rescue. Our service provides a massive catalog with more than 85,000 ready-to-use state-specific documents that work for practically any legal situation. US Legal Forms also is an excellent asset for associates or legal counsels who want to to be more efficient time-wise using our DYI tpapers.

No matter if you need the Killeen Texas Deed in Lieu of Foreclosure or any other paperwork that will be valid in your state or county, with US Legal Forms, everything is on hand. Here’s how to get the Killeen Texas Deed in Lieu of Foreclosure quickly using our trusted service. In case you are already an existing customer, you can go ahead and log in to your account to download the needed form.

However, if you are new to our platform, make sure to follow these steps before obtaining the Killeen Texas Deed in Lieu of Foreclosure:

- Ensure the form you have found is suitable for your location since the regulations of one state or county do not work for another state or county.

- Preview the document and go through a short outline (if available) of cases the paper can be used for.

- If the form you picked doesn’t suit your needs, you can start over and look for the needed form.

- Click Buy now and choose the subscription plan that suits you the best.

- utilizing your login information or create one from scratch.

- Choose the payment method and proceed to download the Killeen Texas Deed in Lieu of Foreclosure once the payment is through.

You’re all set! Now you can go ahead and print the document or fill it out online. In case you have any issues locating your purchased documents, you can quickly access them in the My Forms tab.

Whatever situation you’re trying to solve, US Legal Forms has got you covered. Try it out today and see for yourself.