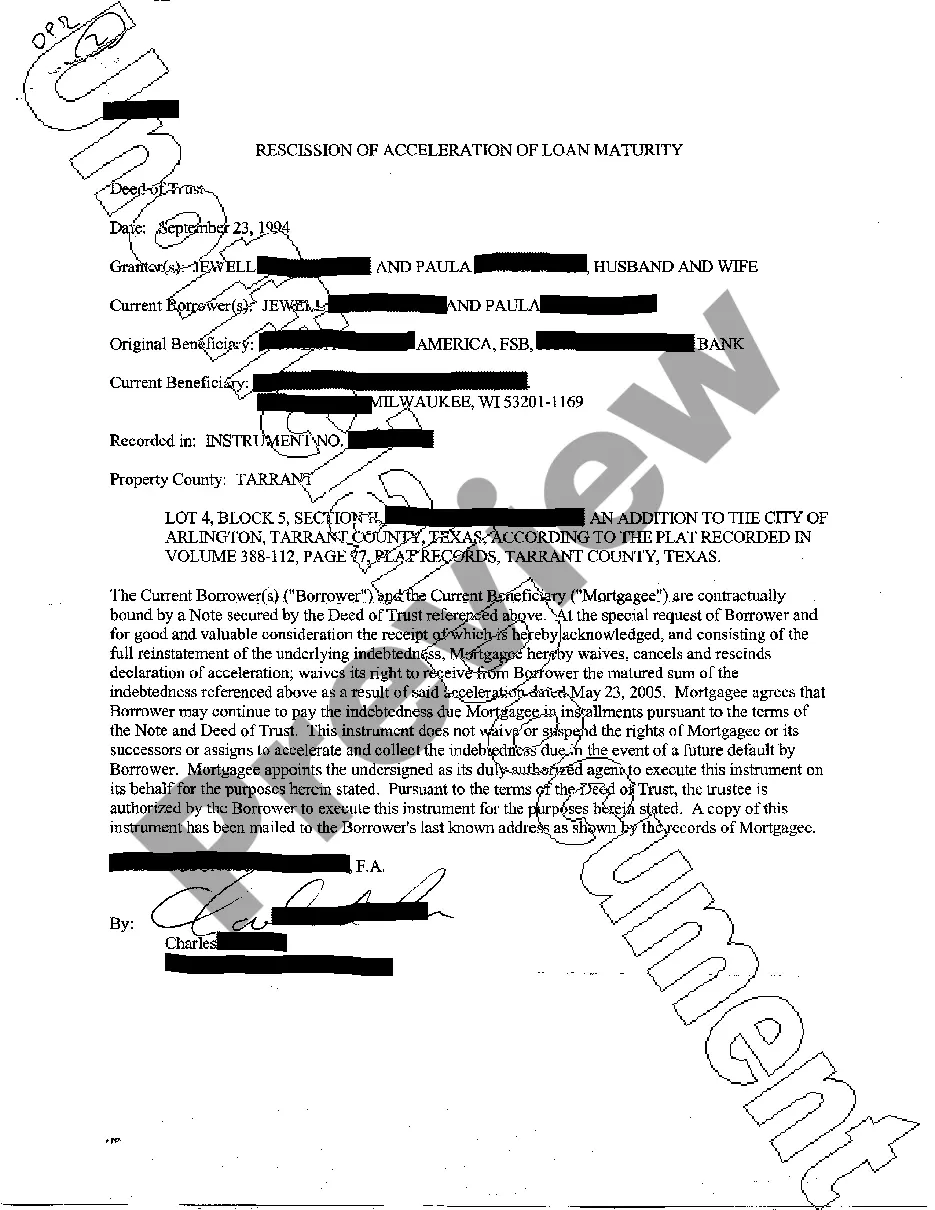

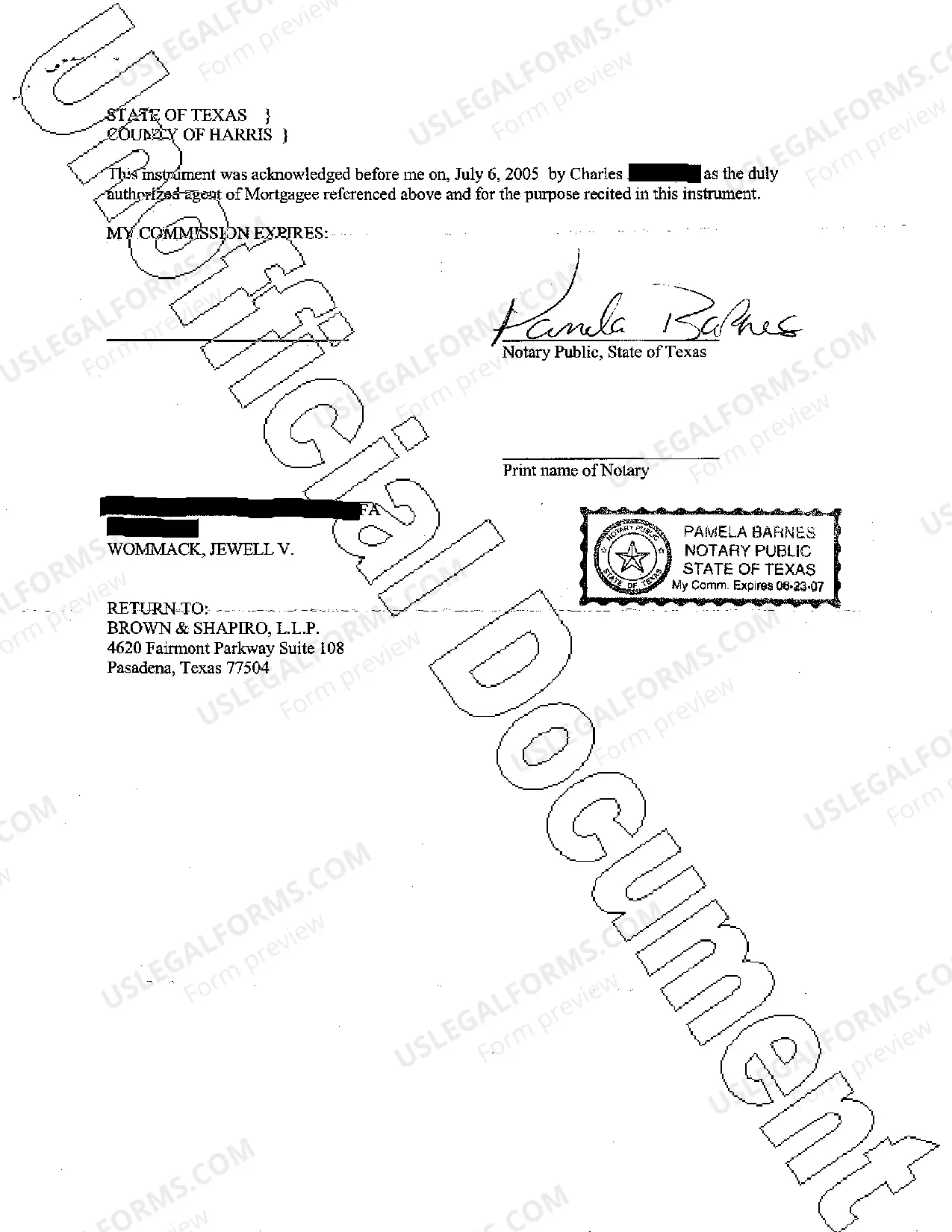

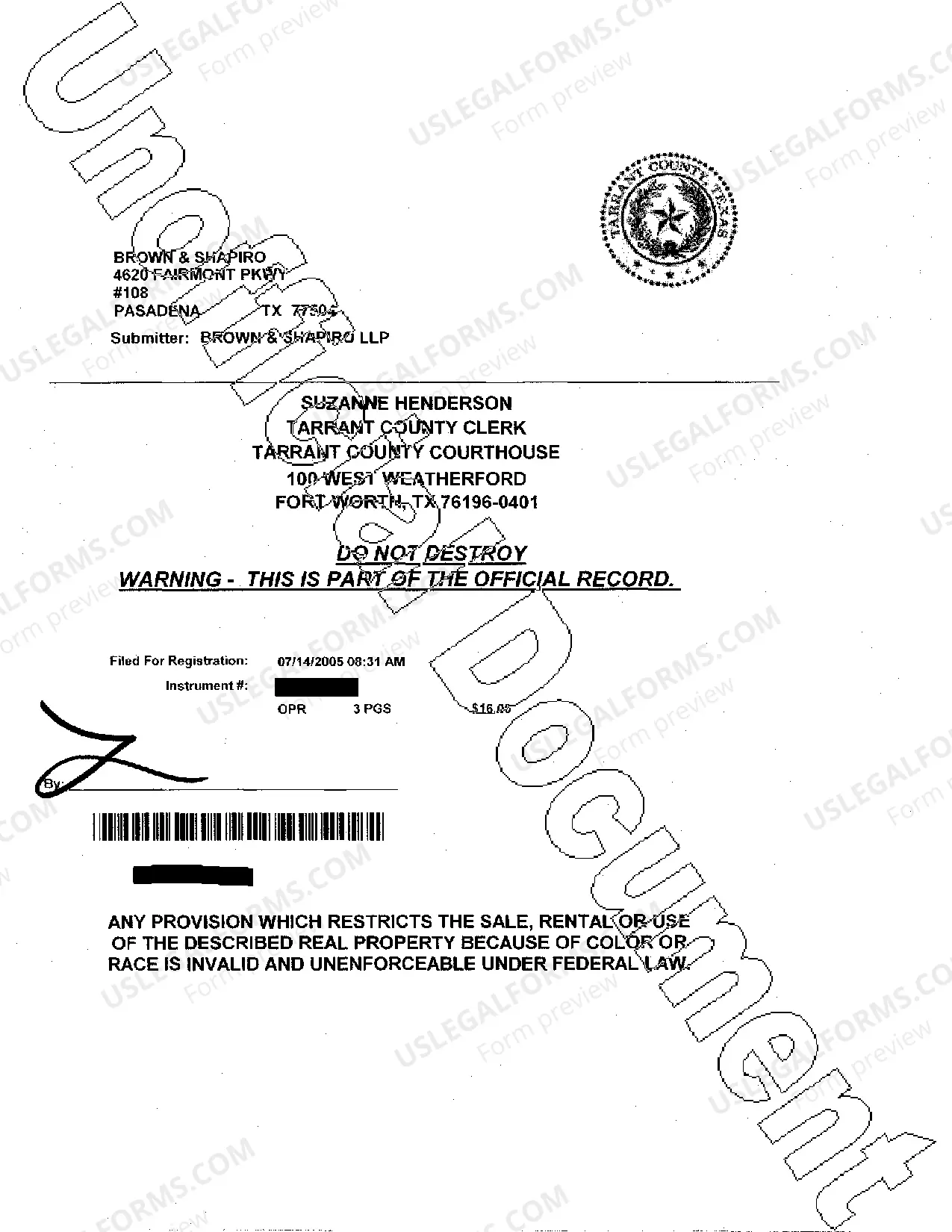

Houston Texas Rescission of Acceleration of Loan Maturity refers to a legal process in which a borrower in Houston, Texas, has the right to undo or reverse the acceleration of the maturity date of a loan. When a borrower defaults on their loan payments, the lender may choose to accelerate the maturity date of the loan, making the full amount of the loan due immediately. However, under certain circumstances, the borrower can exercise their right to rescind or reverse this acceleration. The Houston Texas Rescission of Acceleration of Loan Maturity can be applicable in various loan types, including mortgages, car loans, and personal loans. The key objective of this rescission is to provide the borrower with an opportunity to reinstate the loan by bringing the account current and resuming regular payments, thus avoiding foreclosure or repossession. It is crucial to note that there are no specific branches or types of Rescission of Acceleration of Loan Maturity unique to Houston, Texas. However, the general process for seeking rescission may differ based on the type of loan and the particular lender involved. To initiate the rescission process, the borrower typically needs to submit a written notice to the lender, explicitly stating their intent to rescind the acceleration of loan maturity. This notice should include relevant details such as the loan account number, borrower's contact information, and a clear explanation of why the borrower believes the acceleration should be rescinded. Additionally, the borrower may need to provide supporting documentation, such as proof of missed payments or financial hardship, to strengthen their case. It is crucial to ensure that the notice is sent within the designated timeframe specified in the loan agreement or under applicable Texas state laws. Once the lender receives the borrower's written notice of rescission, they must carefully review the situation and assess the merit of the borrower's request. The lender may consider factors like the borrower's payment history, repayment capacity, and other relevant circumstances before making a decision. If the lender agrees to rescind the acceleration of loan maturity, they will typically provide the borrower with written confirmation of this decision. The borrower will then have the opportunity to reinstate the loan by paying any outstanding arrears, late fees, or penalties, bringing the loan account current, and resuming the regular payment schedule. It is important for borrowers in Houston, Texas, to consult an experienced attorney or seek professional advice when dealing with the Rescission of Acceleration of Loan Maturity. By understanding their rights and following the proper procedures, borrowers can potentially avoid the adverse consequences of loan acceleration, such as foreclosure or repossession.

Houston Texas Rescission of Acceleration of Loan Maturity

Description

How to fill out Houston Texas Rescission Of Acceleration Of Loan Maturity?

If you are looking for a suitable document, it’s difficult to find a more accessible platform than the US Legal Forms site – one of the largest collections on the web.

Here you can discover numerous templates for business and personal use by categories and locations, or keywords.

Using our enhanced search feature, locating the most up-to-date Houston Texas Rescission of Acceleration of Loan Maturity is as simple as 1-2-3.

Complete the payment. Use your credit card or PayPal account to finalize the registration process.

Obtain the form. Specify the file format and download it to your device.

- If you are already aware of our platform and possess a registered account, all you need to obtain the Houston Texas Rescission of Acceleration of Loan Maturity is to Log In to your account and click the Download option.

- If you are using US Legal Forms for the first time, just adhere to the guidelines below.

- Ensure you have located the document you require. Review its description and utilize the Preview feature (if available) to examine its content.

- If it doesn’t satisfy your requirements, use the Search option at the top of the page to find the necessary file.

- Affirm your choice. Choose the Buy now option.

Form popularity

FAQ

The Notice of Acceleration is just one name for a document from your lender which advises you that ALL of your mortgage payments, including past missed payments, will be due within the next 30 to 90 days.

The good news is, borrowers are generally able to avoid acceleration by working out a loan modification or repayment plan with their lender to make up delinquent payments. This is called a mortgage reinstatement.

An acceleration clause allows the lender to require payment before the standard terms of the loan expire. Acceleration clauses are typically contingent on on-time payments. Acceleration clauses are most common in mortgage loans and help to mitigate the risk of default for the lender.

What Are Foreclosure Acceleration Clauses? Foreclosure proceedings are possible because most mortgage loan documentation contains an acceleration clause. This clause gives the lender the right to collect the entire amount due on the loan if the borrower fails to make the monthly mortgage payments.

An accelerated clause is a term in a loan agreement that requires the borrower to pay off the loan immediately under certain conditions. An accelerated clause is typically invoked when the borrower materially breaches the loan agreement.

Texas law requires that the lender/servicer must send the borrower a notice of default and intent to accelerate by certified mail that provides at least 20 days to cure the default before notice of sale can be given.

After the loan is accelerated, the borrower can no longer pay off the loan in installments; the loan changes from an installment contract to a debt that's due in a single, lump-sum payment.

After the loan is accelerated, the borrower can no longer pay off the loan in installments; the loan changes from an installment contract to a debt that's due in a single, lump-sum payment.

Delayed or Missed Payments ? Repeated missed payments may force the lender to effectuate an acceleration clause. Thankfully, making full mortgage payments before can reverse the process.

The Notice of Acceleration is just one name for a document from your lender which advises you that ALL of your mortgage payments, including past missed payments, will be due within the next 30 to 90 days.

Interesting Questions

More info

· Land Development Bank of Austin, TX Home Loan Sales Up 9% in FY2012. · Farm gate Home Loans, a subsidiary of Weyerhaeuser, Inc., reported on June 13, 2012, that bank lending to small business and agriculture clients is running above the prior year level and that home loans to both industries are doing well. · Farmers are experiencing higher levels of economic growth and more opportunities for farming. · The agriculture sector currently supports about 13,500 jobs and has the potential to support another 30,000 jobs by 2015. · In 2012, Farmers were able to use their farm capital to complete one out of every six of the more than 7 million farms in the end in 2012, the annual value of the capital raised was in excess of billion. · Agriculture also has lower unemployment rates and lower foreclosure rates compared to other sectors.

Disclaimer

The materials in this section are taken from public sources. We disclaim all representations or any warranties, express or implied, as to the accuracy, authenticity, reliability, accessibility, adequacy, or completeness of any data in this paragraph. Nevertheless, we make every effort to cite public sources deemed reliable and trustworthy.