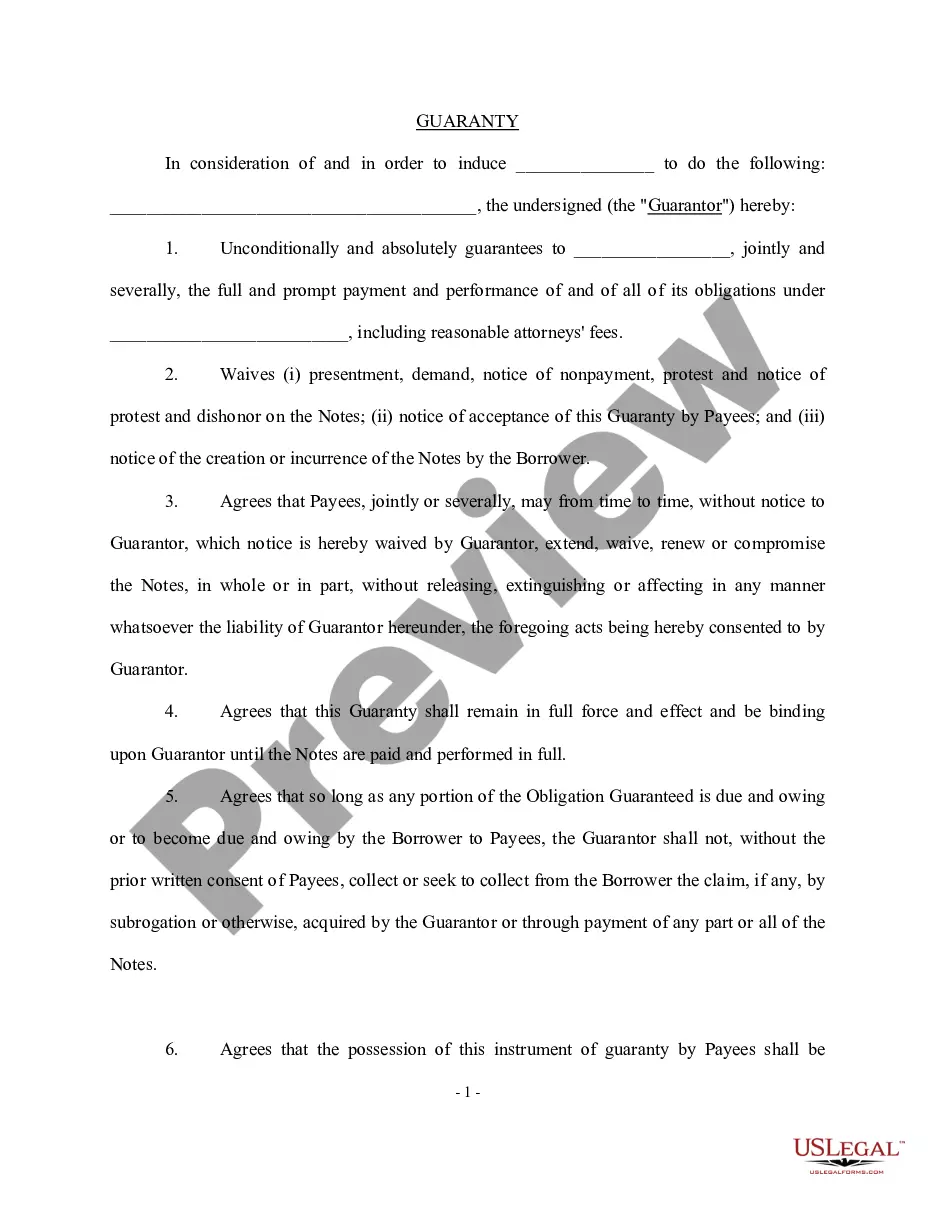

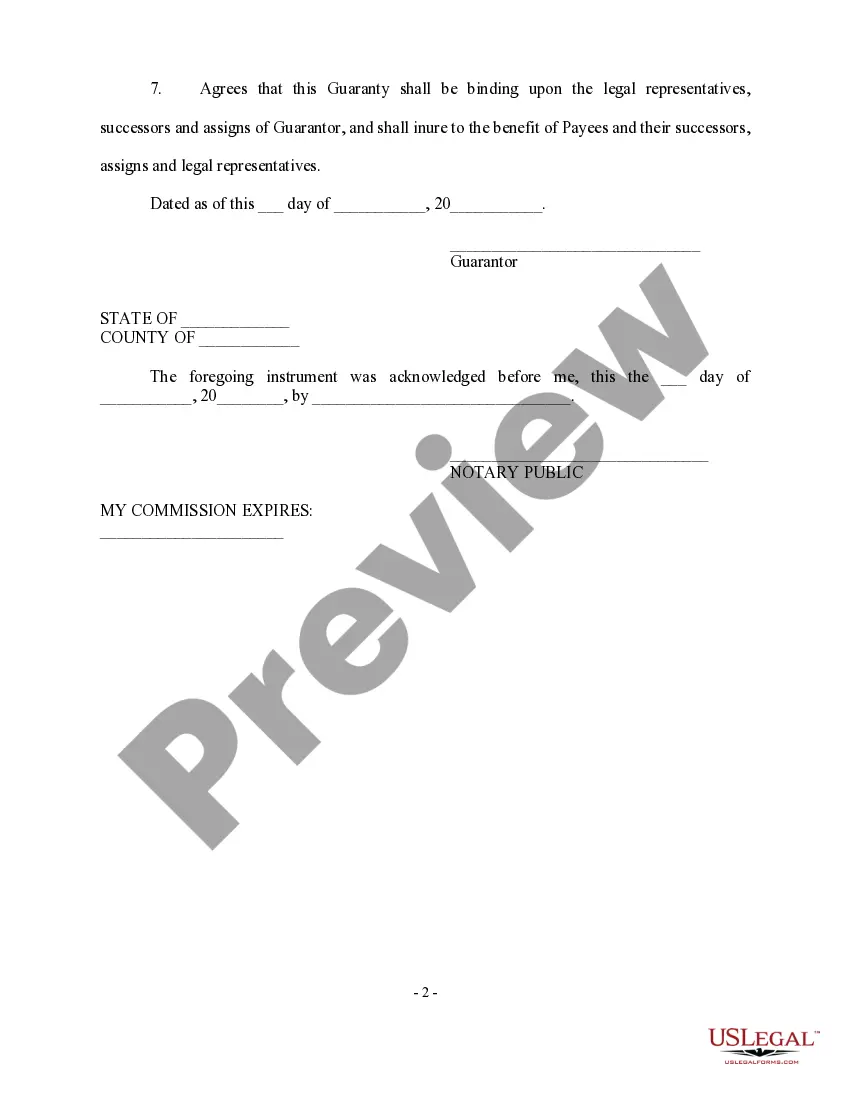

Maricopa, Arizona Personal Guaranty — General: An In-depth Explanation A Maricopa, Arizona personal guaranty is a legal agreement that involves a person (guarantor) assuming responsibility for fulfilling the financial obligations or debts associated with another individual or entity (debtor). This guarantee provides lenders, businesses, or creditors with an added layer of security, ensuring that they can recover their debts if the primary borrower defaults. Keywords: Maricopa, Arizona; personal guaranty; general; legal agreement; financial obligations; debts; individual; entity; guarantor; lender; businesses; creditor; layer of security; primary borrower; defaults. In Maricopa, Arizona, there may be various types of personal guaranty agreements tailored to specific situations. Though the main purpose remains the same, the terms and conditions can differ based on the nature of the debt or the involved parties. Here, we outline some common types of Maricopa, Arizona personal guaranty — general: 1. Business Loan Guaranty: This type of personal guaranty usually applies when a business entity seeks funding from a lender. In this case, the guarantor offers personal assets or guarantees a portion of their personal income to secure the loan's repayment. By signing this agreement, the guarantor becomes personally liable for the debt if the business defaults. 2. Lease Guaranty: When an individual or business leases a property, the landlord might require a personal guaranty from the lessee. This guarantee ensures that the landlord will receive rent payments even if the tenant fails to fulfill their obligations. In such cases, the guarantor may be liable for payments, property damages, or other lease-related expenses. 3. Contract Guaranty: Some contracts, such as construction or service agreements, may include a personal guaranty clause. This clause holds a specific individual accountable for fulfilling the contractual obligations if the party initially responsible fails to do so. The guarantor may be required to compensate for financial losses, complete the project, or provide alternative resources. 4. Credit Card Guaranty: In certain cases, when applying for a personal or business credit card, the credit card issuer may request a personal guaranty. By signing this agreement, the guarantor becomes jointly responsible for repaying the debt incurred on the credit card, should the primary cardholder default. While these are common examples, the types of personal guaranty agreements in Maricopa, Arizona can vary. It is crucial for both the guarantor and the debtor to fully understand the terms and implications of the agreement they are entering into. Seeking professional legal advice before signing any personal guaranty is highly recommended ensuring all parties are protected and aware of their obligations. Remember, a personal guaranty is a legally binding contract and should not be taken lightly. It is crucial for all parties involved to carefully review and comprehend the terms, potential risks, and obligations before making an informed decision.

Maricopa Arizona Personal Guaranty - General

Description

How to fill out Maricopa Arizona Personal Guaranty - General?

Dealing with legal forms is a must in today's world. Nevertheless, you don't always need to seek professional help to draft some of them from the ground up, including Maricopa Personal Guaranty - General, with a service like US Legal Forms.

US Legal Forms has more than 85,000 templates to choose from in different categories ranging from living wills to real estate papers to divorce papers. All forms are arranged according to their valid state, making the searching experience less overwhelming. You can also find information materials and tutorials on the website to make any activities related to paperwork execution straightforward.

Here's how you can locate and download Maricopa Personal Guaranty - General.

- Go over the document's preview and outline (if provided) to get a general information on what you’ll get after downloading the form.

- Ensure that the template of your choice is adapted to your state/county/area since state regulations can impact the legality of some records.

- Examine the related document templates or start the search over to find the appropriate file.

- Click Buy now and create your account. If you already have an existing one, select to log in.

- Choose the option, then a suitable payment method, and purchase Maricopa Personal Guaranty - General.

- Select to save the form template in any offered file format.

- Visit the My Forms tab to re-download the file.

If you're already subscribed to US Legal Forms, you can find the needed Maricopa Personal Guaranty - General, log in to your account, and download it. Needless to say, our website can’t take the place of a lawyer completely. If you have to cope with an exceptionally difficult situation, we advise using the services of a lawyer to review your form before signing and submitting it.

With more than 25 years on the market, US Legal Forms proved to be a go-to provider for various legal forms for millions of customers. Become one of them today and get your state-specific documents with ease!