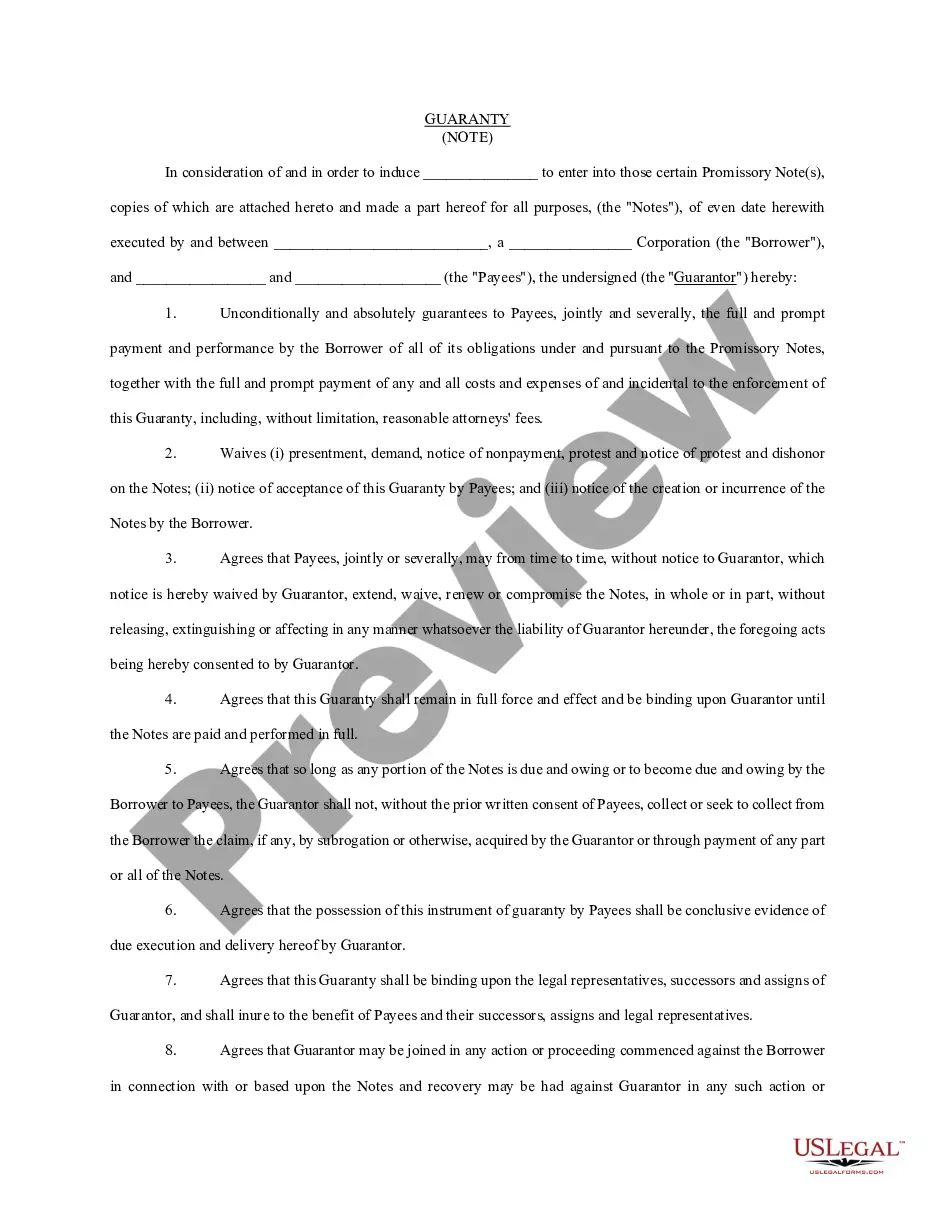

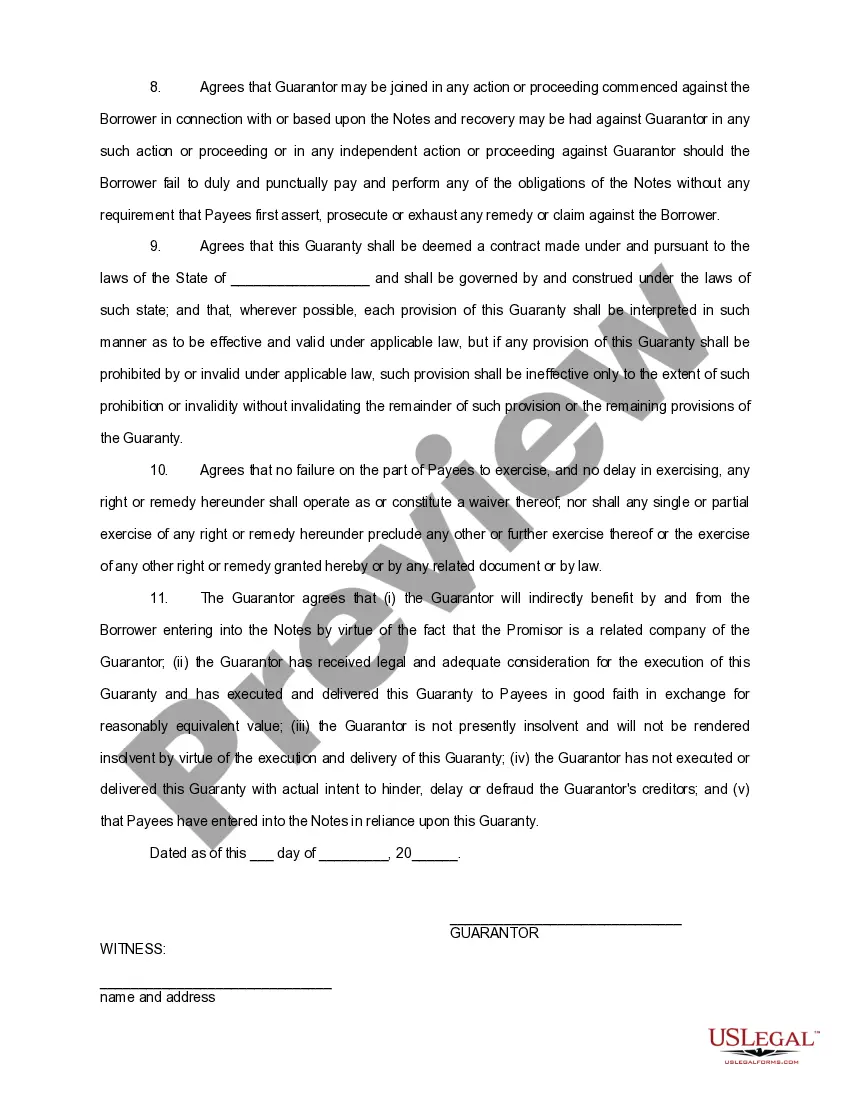

The Harris Texas Guaranty of Promissory Note by Individual — Corporate Borrower is a legally binding document that outlines the responsibilities and obligations of an individual guarantor towards a promissory note issued by a corporate borrower located in Harris County, Texas. It provides a detailed description of the terms and conditions under which the guarantor becomes liable for the repayment of the promissory note in case of default by the corporate borrower. Keywords: Harris Texas, guaranty of promissory note, individual, corporate borrower, responsibilities, obligations, terms and conditions, liable, repayment, default, legally binding. Types of Harris Texas Guaranty of Promissory Note by Individual — Corporate Borrower: 1. Limited Guaranty: The limited guaranty specifies a predetermined amount for which the individual guarantor would be liable in case of default by the corporate borrower. This amount is often capped and agreed upon by all parties involved. 2. Unlimited Guaranty: Unlike the limited guaranty, the unlimited guaranty does not have a predetermined amount. The individual guarantor is responsible for the entire outstanding balance of the promissory note, along with any interest, fees, or expenses incurred as a result of the corporate borrower's default. 3. Conditional Guaranty: A conditional guaranty imposes specific conditions and requirements on the individual guarantor. It may include provisions relating to the borrower's financial status, the occurrence of specified events, or the borrower's compliance with certain obligations. If these conditions are not met, the guarantor's liability may be waived. 4. Unconditional Guaranty: An unconditional guaranty does not impose any conditions or requirements on the individual guarantor. Once signed, the guarantor becomes directly and unconditionally liable for the repayment of the promissory note, regardless of the circumstances or actions of the corporate borrower. 5. Continuing Guaranty: A continuing guaranty extends the guarantor's liability beyond a specific period. It implies that the guarantor will remain liable for the promissory note's repayment until it is fully satisfied, even if the note undergoes extensions, renewals, or modifications. 6. Limited Recourse Guaranty: A limited recourse guaranty limits the remedies available to the lender against the individual guarantor in case of default by the corporate borrower. It may restrict the lender's ability to pursue certain assets of the guarantor or impose a cap on the total amount that can be recovered. By understanding the different types of Harris Texas Guaranty of Promissory Note by Individual — Corporate Borrower, individuals and corporate borrowers can select an appropriate guaranty that suits their specific needs, level of liability, and risk tolerance. It is essential to consult legal and financial professionals for advice before entering into any such agreement.

Harris Texas Guaranty of Promissory Note by Individual - Corporate Borrower

Description

How to fill out Harris Texas Guaranty Of Promissory Note By Individual - Corporate Borrower?

Laws and regulations in every area vary around the country. If you're not a lawyer, it's easy to get lost in countless norms when it comes to drafting legal documents. To avoid high priced legal assistance when preparing the Harris Guaranty of Promissory Note by Individual - Corporate Borrower, you need a verified template legitimate for your county. That's when using the US Legal Forms platform is so advantageous.

US Legal Forms is a trusted by millions web catalog of more than 85,000 state-specific legal templates. It's an excellent solution for professionals and individuals searching for do-it-yourself templates for various life and business situations. All the documents can be used many times: once you pick a sample, it remains available in your profile for subsequent use. Thus, if you have an account with a valid subscription, you can just log in and re-download the Harris Guaranty of Promissory Note by Individual - Corporate Borrower from the My Forms tab.

For new users, it's necessary to make a couple of more steps to obtain the Harris Guaranty of Promissory Note by Individual - Corporate Borrower:

- Take a look at the page content to make sure you found the right sample.

- Take advantage of the Preview option or read the form description if available.

- Look for another doc if there are inconsistencies with any of your requirements.

- Utilize the Buy Now button to get the template when you find the correct one.

- Choose one of the subscription plans and log in or create an account.

- Choose how you prefer to pay for your subscription (with a credit card or PayPal).

- Pick the format you want to save the document in and click Download.

- Fill out and sign the template in writing after printing it or do it all electronically.

That's the easiest and most affordable way to get up-to-date templates for any legal reasons. Find them all in clicks and keep your documentation in order with the US Legal Forms!