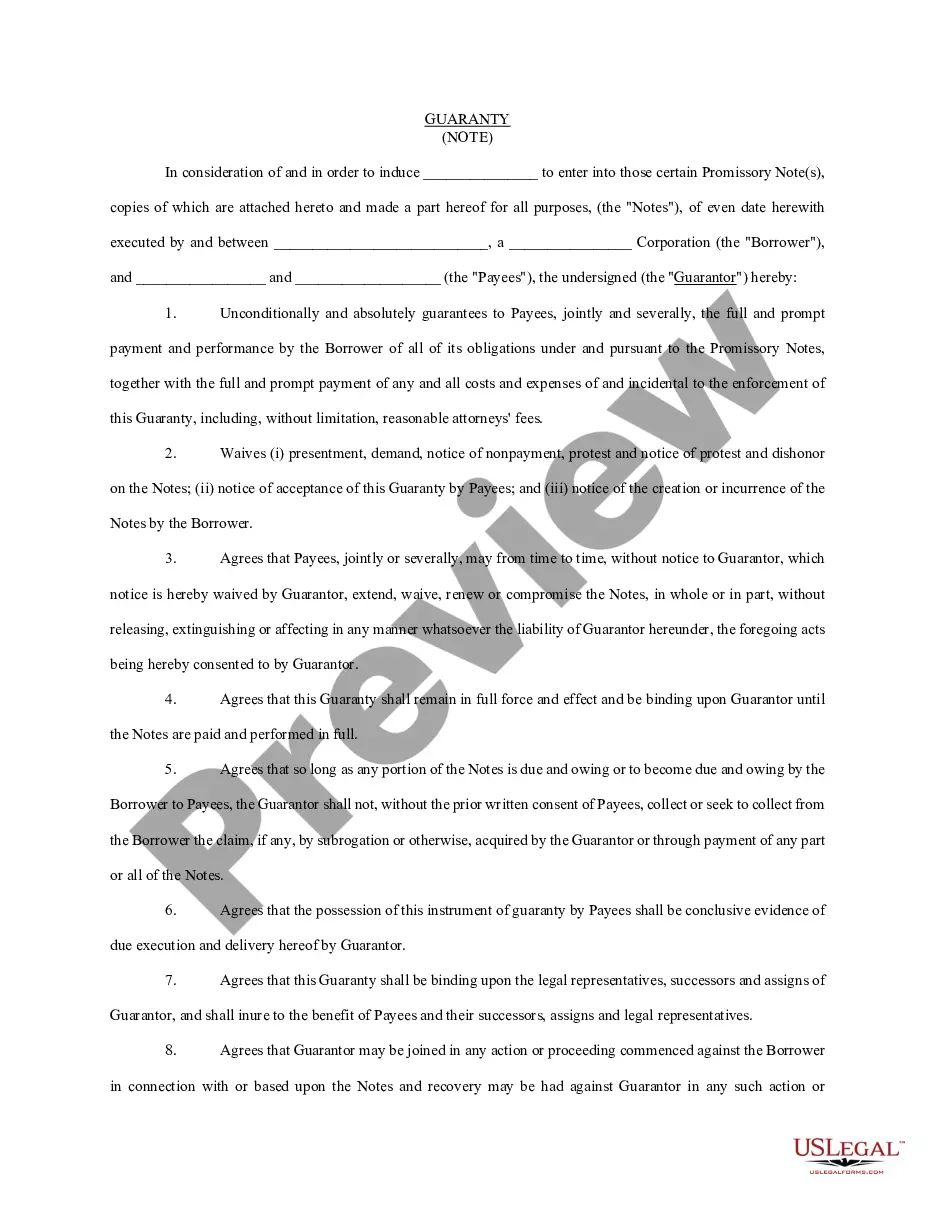

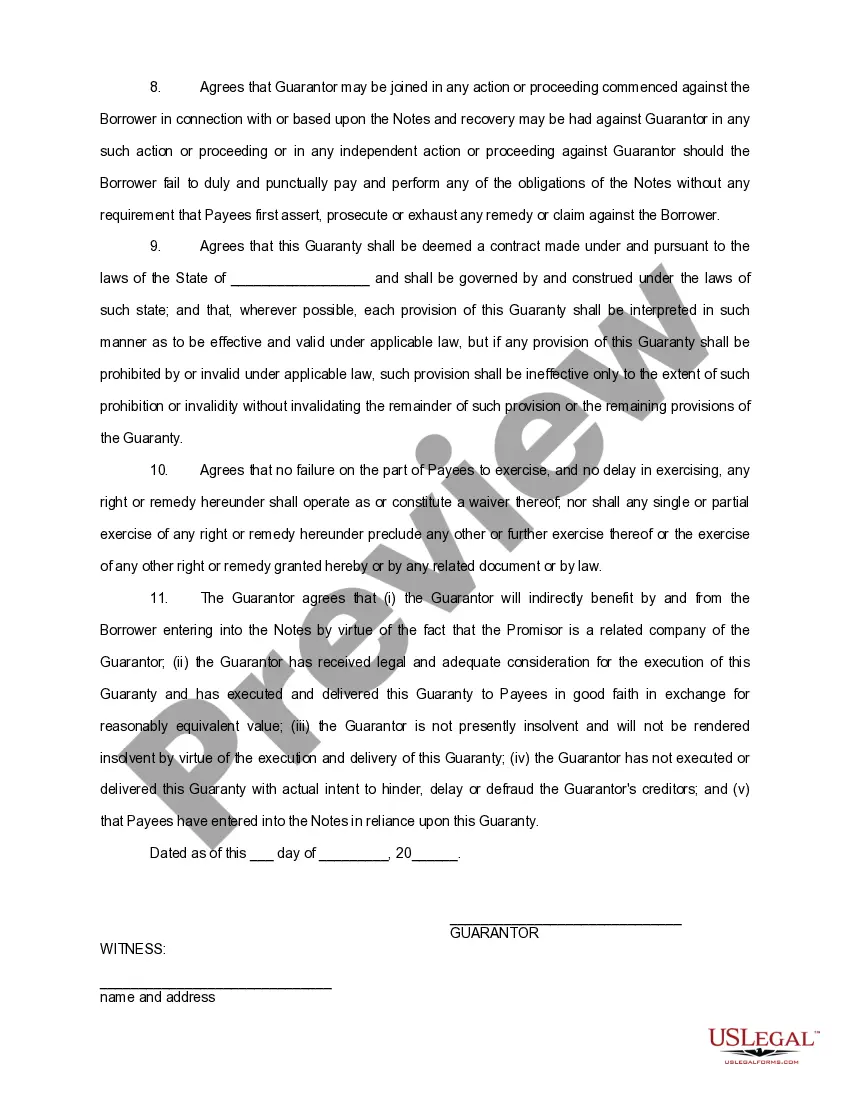

A Mecklenburg North Carolina Guaranty of Promissory Note by Individual — Corporate Borrower is a legal document that serves as a guarantee for the repayment of a promissory note by an individual on behalf of a corporate borrower. This type of agreement is commonly used in the business and financial sectors, where a corporate borrower seeks additional assurance that the borrowed funds will be repaid. The Mecklenburg North Carolina Guaranty of Promissory Note provides protection for the lender by offering an additional source of liability and repayment in case the corporate borrower defaults on the promissory note. The individual guarantor is legally bound to fulfill the obligations of the borrower if they fail to meet their repayment responsibilities. Thus, the lender can seek recourse from the guarantor to recover any outstanding amounts owed. There might be different variations of the Mecklenburg North Carolina Guaranty of Promissory Note by Individual — Corporate Borrower, depending on the specific terms and conditions agreed upon by the parties involved. For instance, some agreements may include specific provisions regarding interest rates, payment schedules, late payment penalties, or collateral requirements. These variations in the agreement allow for customization based on the unique needs and circumstances of the loan transaction. By signing this guaranty agreement, the individual guarantor assumes a significant responsibility as they become personally liable for any outstanding debt in case of default by the corporate borrower. It is imperative for both parties to carefully review and understand the terms outlined in the document before signing, as it establishes a legal commitment that can have far-reaching financial implications. In summary, the Mecklenburg North Carolina Guaranty of Promissory Note by Individual — Corporate Borrower ensures additional security for lenders by obtaining a personal guarantee from an individual on behalf of a corporate borrower. Its purpose is to mitigate the risk of default and offer an alternative source of repayment. Different variations of this agreement may exist to accommodate specific loan terms and conditions. However, it is essential to consult legal professionals to ensure compliance with relevant state laws and to fully understand the rights and obligations outlined in the document.

Mecklenburg North Carolina Guaranty of Promissory Note by Individual - Corporate Borrower

Description

How to fill out Mecklenburg North Carolina Guaranty Of Promissory Note By Individual - Corporate Borrower?

Draftwing documents, like Mecklenburg Guaranty of Promissory Note by Individual - Corporate Borrower, to take care of your legal matters is a challenging and time-consumming task. Many cases require an attorney’s involvement, which also makes this task expensive. Nevertheless, you can get your legal issues into your own hands and deal with them yourself. US Legal Forms is here to save the day. Our website comes with more than 85,000 legal forms created for a variety of cases and life circumstances. We ensure each form is in adherence with the laws of each state, so you don’t have to be concerned about potential legal problems compliance-wise.

If you're already familiar with our website and have a subscription with US, you know how effortless it is to get the Mecklenburg Guaranty of Promissory Note by Individual - Corporate Borrower template. Go ahead and log in to your account, download the template, and personalize it to your requirements. Have you lost your form? No worries. You can find it in the My Forms folder in your account - on desktop or mobile.

The onboarding flow of new customers is fairly easy! Here’s what you need to do before downloading Mecklenburg Guaranty of Promissory Note by Individual - Corporate Borrower:

- Ensure that your document is specific to your state/county since the rules for writing legal documents may differ from one state another.

- Learn more about the form by previewing it or going through a brief description. If the Mecklenburg Guaranty of Promissory Note by Individual - Corporate Borrower isn’t something you were hoping to find, then take advantage of the search bar in the header to find another one.

- Sign in or register an account to start utilizing our service and download the document.

- Everything looks good on your end? Click the Buy now button and choose the subscription option.

- Pick the payment gateway and type in your payment details.

- Your form is all set. You can go ahead and download it.

It’s easy to find and purchase the appropriate template with US Legal Forms. Thousands of businesses and individuals are already taking advantage of our extensive collection. Sign up for it now if you want to check what other benefits you can get with US Legal Forms!