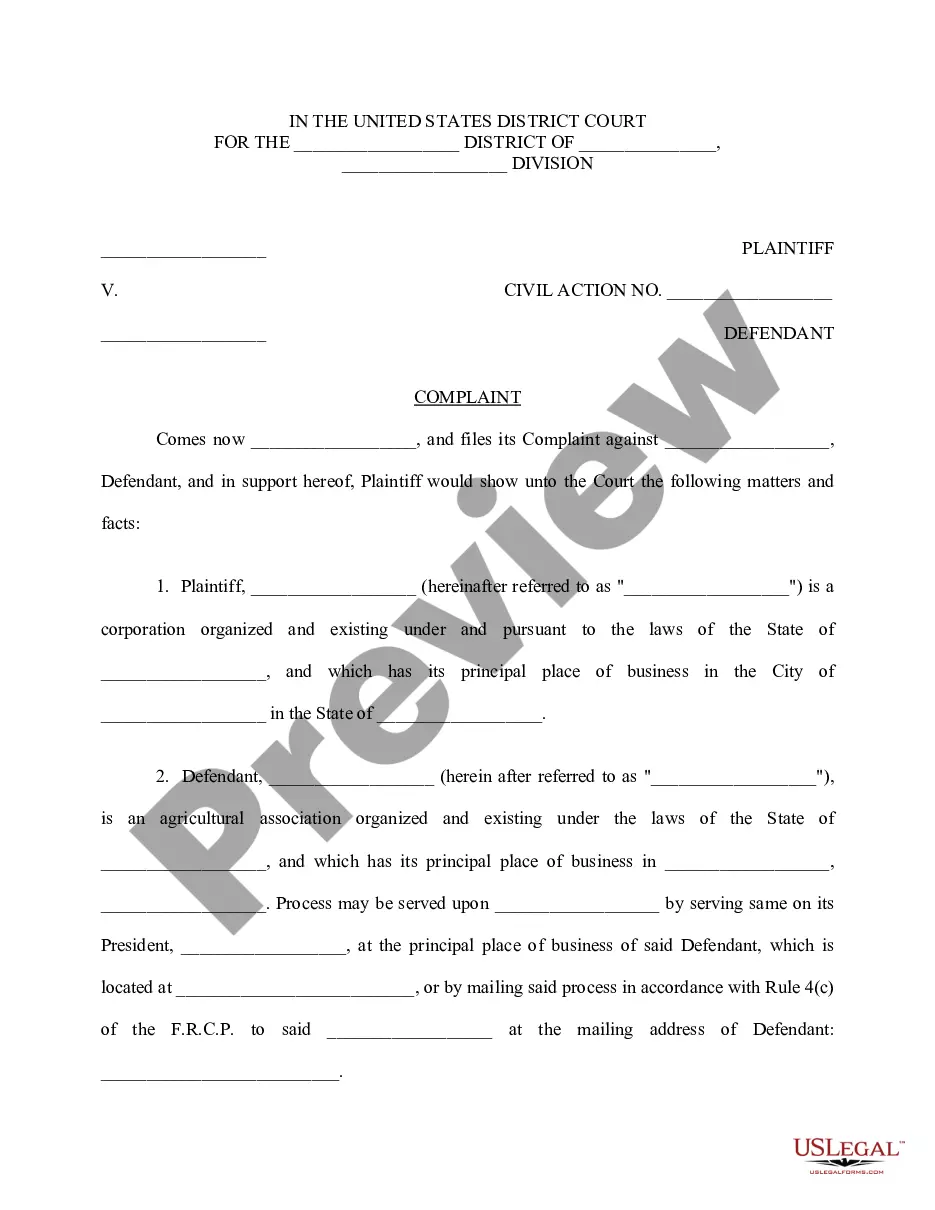

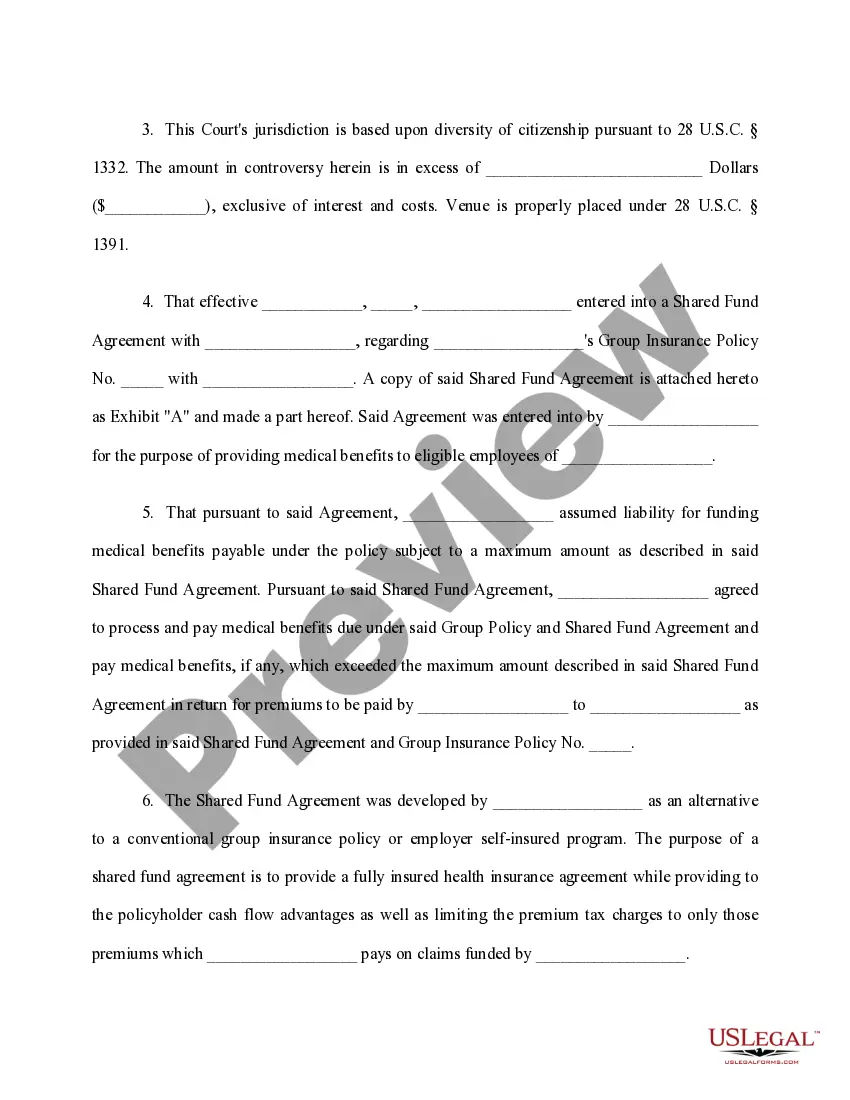

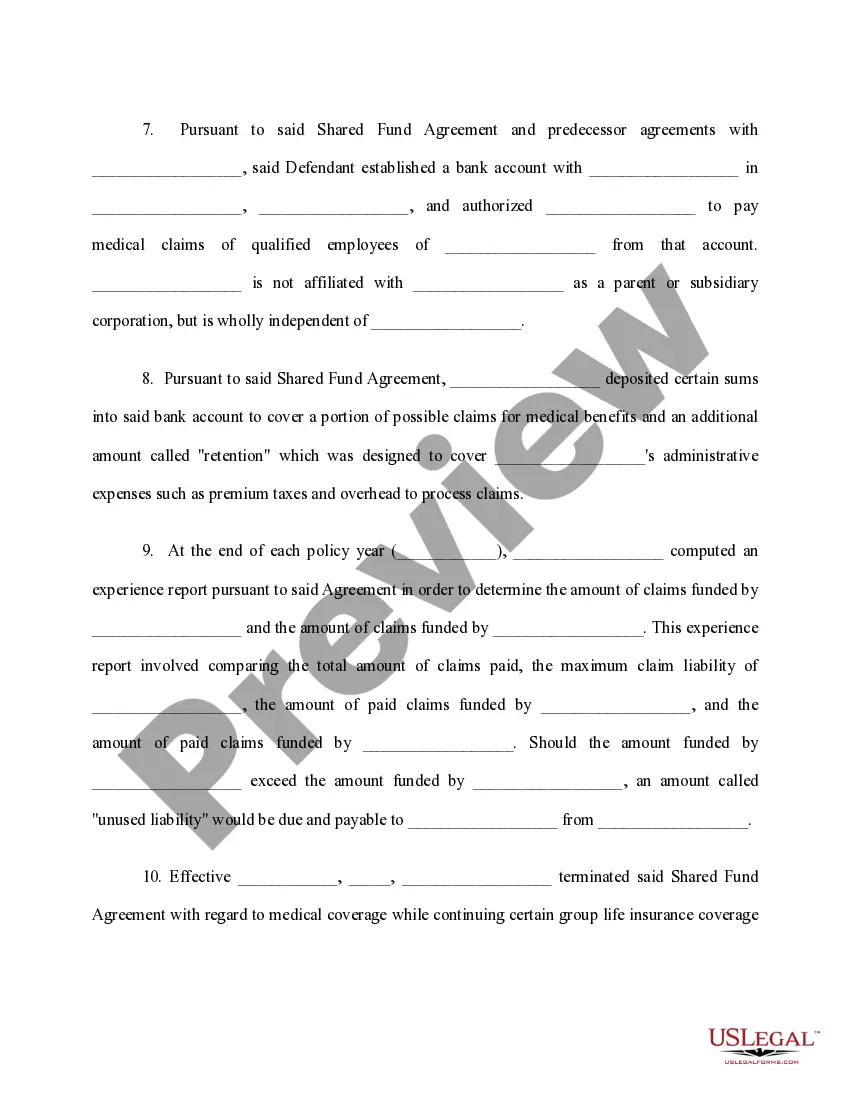

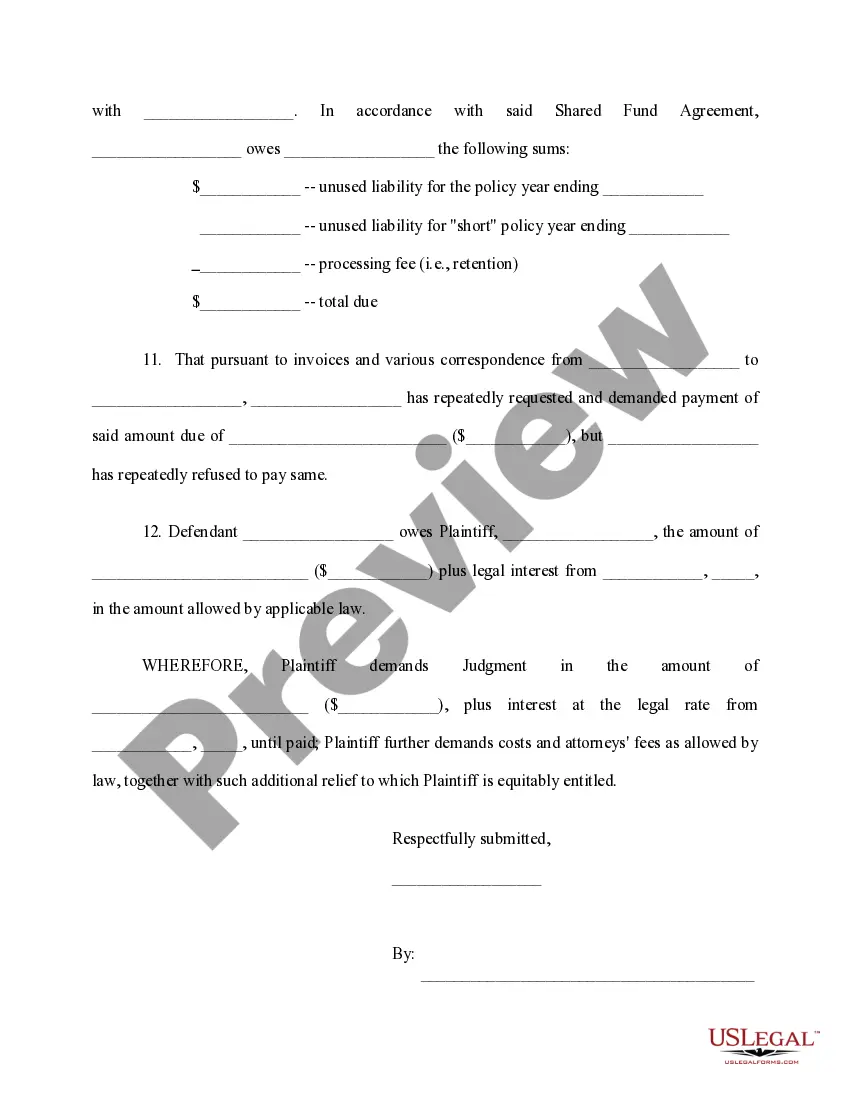

Mecklenburg North Carolina Complaints regarding Group Insurance Contract often refer to a variety of issues and concerns raised by individuals or organizations regarding their group insurance agreements. These complaints typically involve elements such as coverage discrepancies, claim denials, premium increases, policy limitations, and unsatisfactory customer service. By addressing these concerns, insurance providers and regulators can strive to improve their services and maintain a fair, efficient, and transparent insurance industry for all parties involved. Here are some common types of Mecklenburg North Carolina Complaints regarding Group Insurance Contract: 1. Coverage Denial Complaints: These complaints arise when individuals or organizations have their insurance claims denied due to perceived discrepancies between the terms of the contract and the actual coverage provided. Often, policyholders may argue that specific medical treatments, procedures, or conditions should be covered under their plan. 2. Claim Processing Complaints: These complaints involve dissatisfaction with the speed, efficiency, or accuracy of claim processing by insurance providers. Policyholders may encounter delays or face difficulties communicating and coordinating with insurance representatives, resulting in frustration and financial burden. 3. Premium Increase Complaints: Policyholders may express concerns over significant premium increases that exceed industry standards or were not adequately communicated beforehand. These complaints often relate to the lack of transparency and unexpected financial strain imposed on individuals or organizations. 4. Policy Limitation Complaints: Some policyholders may complain about the limited nature of their coverage, particularly when they believe certain services or conditions should be included as stated in their contract. These complaints usually focus on perceived gaps in coverage that hinder adequate healthcare or protection. 5. Customer Service Complaints: These complaints pertain to poor customer service experiences, including difficulties in reaching insurance representatives, unresponsiveness, lack of clear communication, or inadequate assistance in resolving policy-related issues. 6. Contract Interpretation Complaints: Policyholders might dispute the interpretation of specific contract terms, arguing that they are unjust or inconsistent with the industry norms. Complaints in this category often revolve around ambiguous or misleading policy wording, which policyholders claim adversely affects their coverage. It is essential for insurance providers and regulatory bodies to address these complaints promptly and adequately. By doing so, they can work towards improving transparency, policy design, claim processing, customer service, and overall customer satisfaction within the group insurance sector of Mecklenburg, North Carolina.

Mecklenburg North Carolina Complaint regarding Group Insurance Contract

Description

How to fill out Mecklenburg North Carolina Complaint Regarding Group Insurance Contract?

Creating documents, like Mecklenburg Complaint regarding Group Insurance Contract, to take care of your legal affairs is a challenging and time-consumming process. A lot of situations require an attorney’s participation, which also makes this task expensive. Nevertheless, you can consider your legal affairs into your own hands and deal with them yourself. US Legal Forms is here to save the day. Our website features more than 85,000 legal documents created for a variety of cases and life circumstances. We make sure each form is in adherence with the laws of each state, so you don’t have to be concerned about potential legal problems compliance-wise.

If you're already aware of our website and have a subscription with US, you know how effortless it is to get the Mecklenburg Complaint regarding Group Insurance Contract form. Simply log in to your account, download the template, and personalize it to your requirements. Have you lost your form? No worries. You can find it in the My Forms tab in your account - on desktop or mobile.

The onboarding process of new customers is just as easy! Here’s what you need to do before downloading Mecklenburg Complaint regarding Group Insurance Contract:

- Ensure that your form is compliant with your state/county since the regulations for writing legal documents may differ from one state another.

- Find out more about the form by previewing it or reading a brief description. If the Mecklenburg Complaint regarding Group Insurance Contract isn’t something you were hoping to find, then use the header to find another one.

- Sign in or create an account to start utilizing our website and download the form.

- Everything looks good on your end? Click the Buy now button and choose the subscription plan.

- Pick the payment gateway and type in your payment information.

- Your form is all set. You can try and download it.

It’s easy to find and purchase the appropriate template with US Legal Forms. Thousands of organizations and individuals are already taking advantage of our extensive library. Sign up for it now if you want to check what other perks you can get with US Legal Forms!