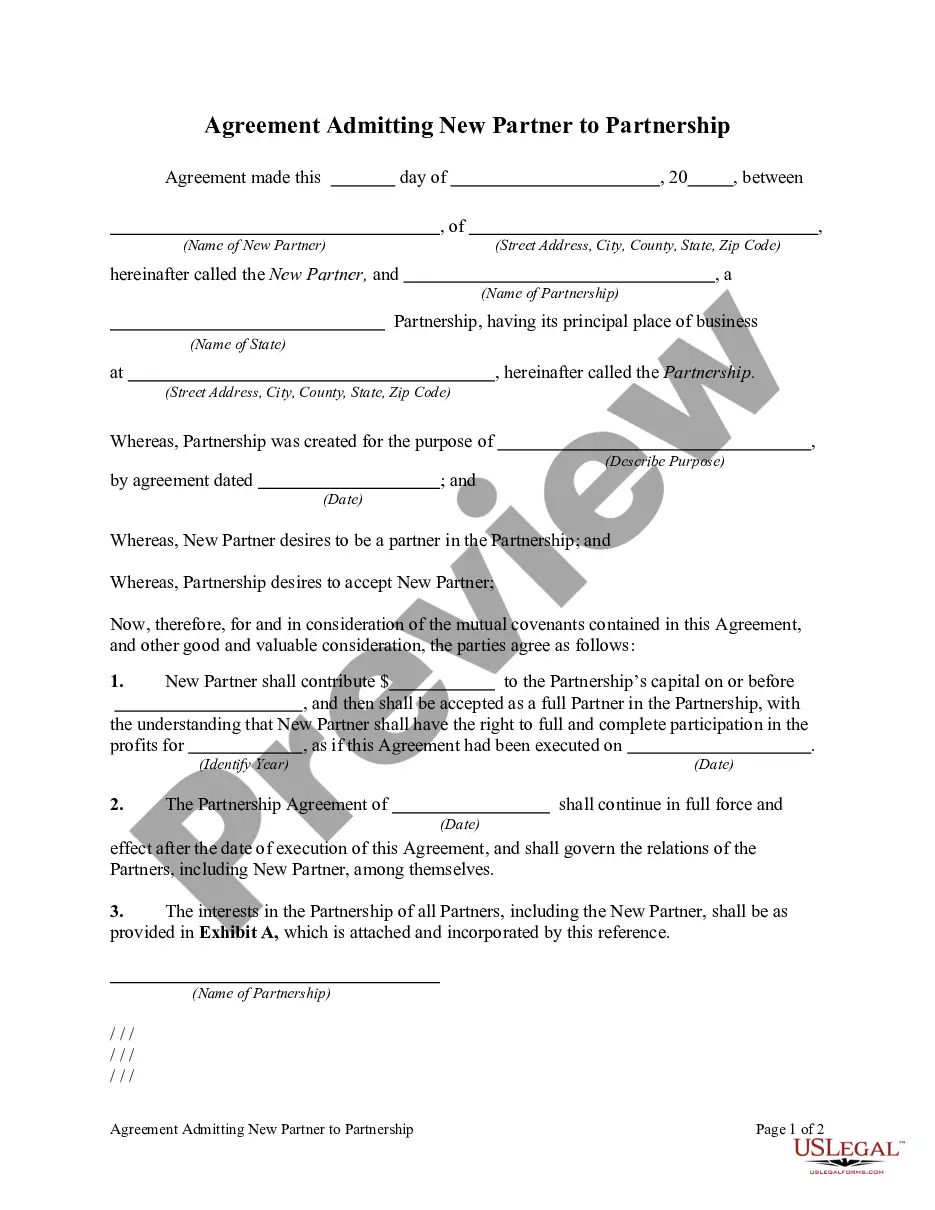

The admission of a new partner results in the legal dissolution of the existing partnership and the beginning of a new one. From an economic standpoint, however, the admission of a new partner (or partners) may be of minor significance in the continuity of the business. For example, in large public accounting or law firms, partners are admitted annually without any change in operating policies. To recognize the economic effects, it is necessary only to open a capital account for each new partner. In the entries illustrated in this appendix, we assume that the accounting records of the predecessor firm will continue to be used by the new partnership. A new partner may be admitted either by (1) purchasing the interest of one or more existing partners or (2) investing assets in the partnership, as shown in Illustration 12A-1. The former affects only the capital accounts of the partners who are parties to the transaction. The latter increases both net assets and total capital of the partnership.

Dallas Texas Agreement Admitting New Partner to Partnership

Description

How to fill out Dallas Texas Agreement Admitting New Partner To Partnership?

Laws and regulations in every sphere differ around the country. If you're not an attorney, it's easy to get lost in countless norms when it comes to drafting legal paperwork. To avoid high priced legal assistance when preparing the Dallas Agreement Admitting New Partner to Partnership, you need a verified template legitimate for your county. That's when using the US Legal Forms platform is so beneficial.

US Legal Forms is a trusted by millions web catalog of more than 85,000 state-specific legal templates. It's a great solution for professionals and individuals looking for do-it-yourself templates for various life and business scenarios. All the forms can be used many times: once you pick a sample, it remains available in your profile for subsequent use. Thus, when you have an account with a valid subscription, you can just log in and re-download the Dallas Agreement Admitting New Partner to Partnership from the My Forms tab.

For new users, it's necessary to make some more steps to get the Dallas Agreement Admitting New Partner to Partnership:

- Take a look at the page content to make sure you found the right sample.

- Use the Preview option or read the form description if available.

- Look for another doc if there are inconsistencies with any of your criteria.

- Use the Buy Now button to obtain the document once you find the right one.

- Opt for one of the subscription plans and log in or sign up for an account.

- Select how you prefer to pay for your subscription (with a credit card or PayPal).

- Pick the format you want to save the document in and click Download.

- Complete and sign the document on paper after printing it or do it all electronically.

That's the easiest and most affordable way to get up-to-date templates for any legal reasons. Locate them all in clicks and keep your documentation in order with the US Legal Forms!