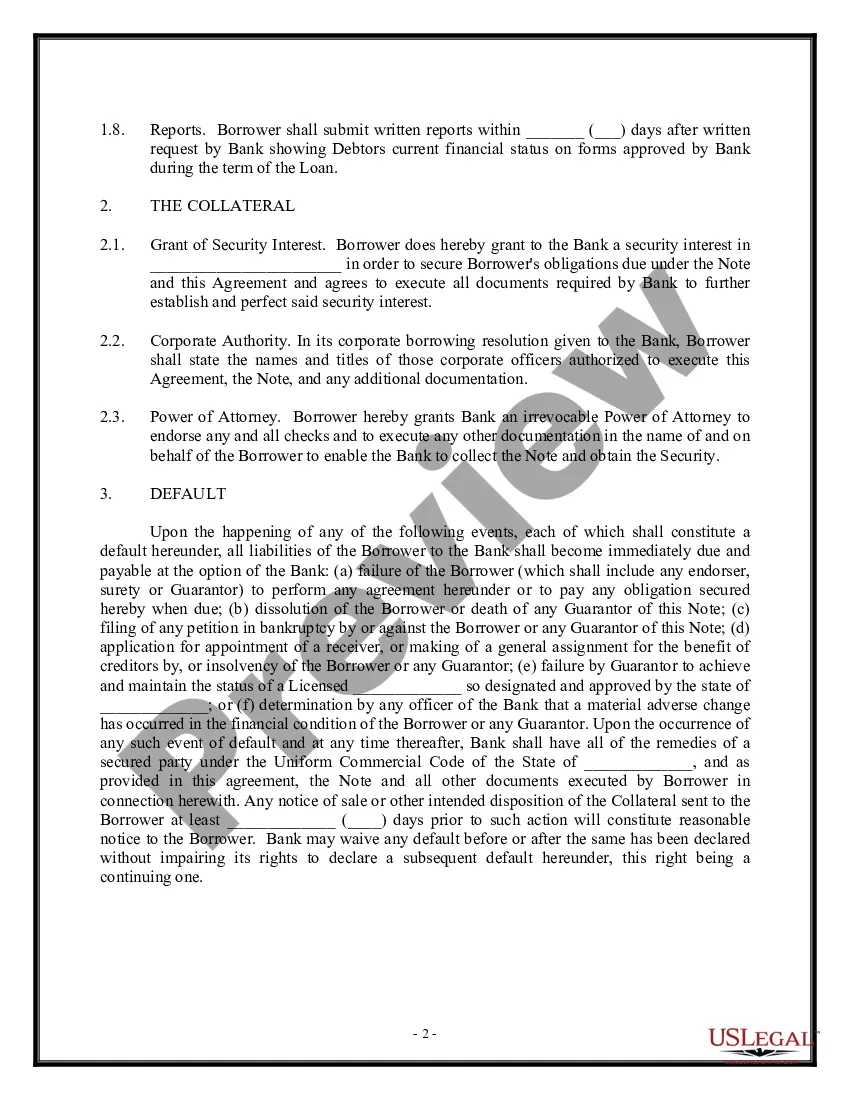

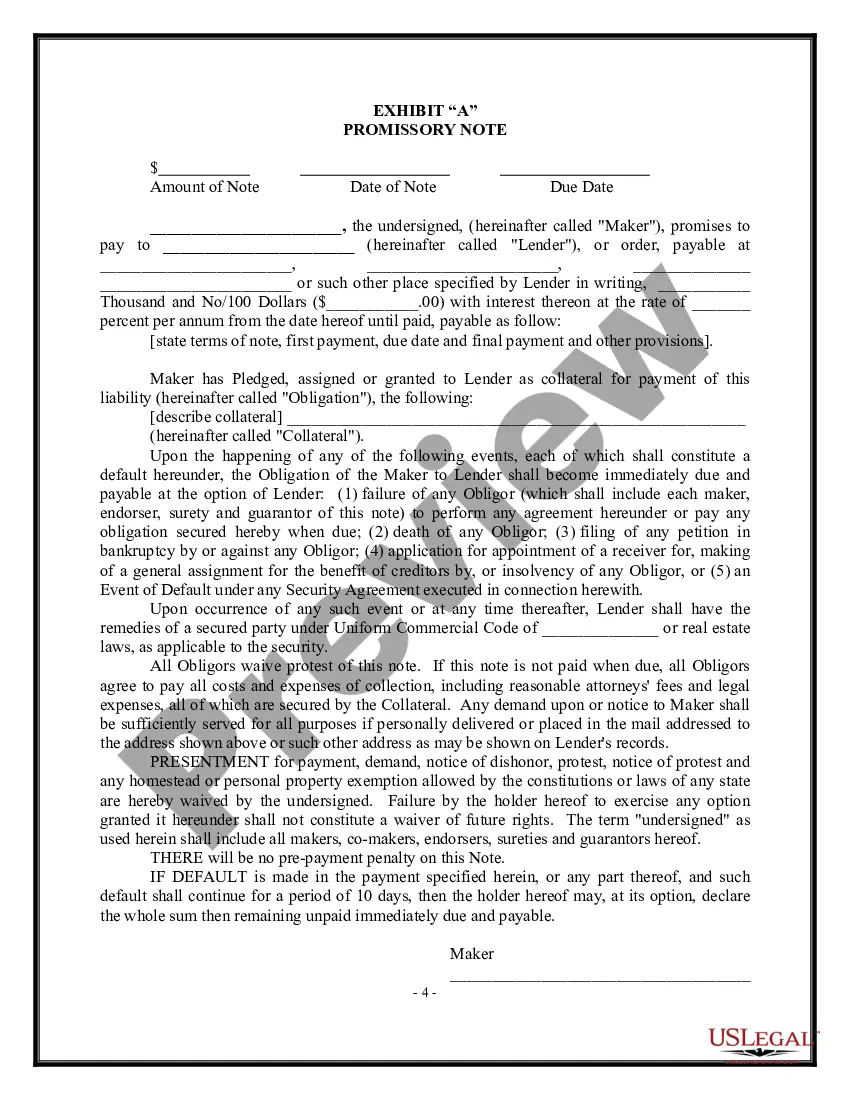

A Loan Agreement — Short Form in Santa Clara, California is a legally binding contract that outlines the terms and conditions under which a lender agrees to loan a certain amount of money to a borrower. This type of agreement is commonly used in various situations such as personal loans, business loans, or financing for real estate transactions. The Santa Clara California Loan Agreement — Short Form must include specific details to protect both parties involved. It typically contains key elements such as the loan amount, interest rate, repayment terms, late payment penalties, and the duration of the loan. Moreover, it should clearly state the purpose of the loan and any collateral that may be used to secure the loan. Different types of Loan Agreement — Short Forms that may exist in Santa Clara, California can include: 1. Personal Loan Agreement: This type of loan agreement is used between individuals, such as friends or family members, where one is borrowing money from the other for personal reasons. It may be used for financing education expenses, medical bills, or home renovations. 2. Business Loan Agreement: This form of loan agreement is designed for businesses that require financial assistance to expand operations, invest in equipment, or meet working capital needs. It can involve a bank, financial institution, or private lender providing funds to a business entity. 3. Real Estate Loan Agreement: This type of agreement is specifically tailored for real estate transactions, such as purchasing a house, commercial property, or land. The loan agreement would outline the terms of the loan, including the loan amount, interest rate, repayment schedule, and any collateral required. Regardless of the specific type, a Loan Agreement — Short Form serves as a legal document to protect the rights and obligations of both the lender and the borrower. It ensures that both parties are aware of their responsibilities and creates a framework for resolving any disputes that may arise during the loan's duration.

Santa Clara California Loan Agreement - Short Form

Description

How to fill out Santa Clara California Loan Agreement - Short Form?

If you need to find a reliable legal form provider to find the Santa Clara Loan Agreement - Short Form, consider US Legal Forms. No matter if you need to launch your LLC business or take care of your belongings distribution, we got you covered. You don't need to be knowledgeable about in law to locate and download the needed form.

- You can browse from over 85,000 forms categorized by state/county and situation.

- The intuitive interface, variety of supporting resources, and dedicated support team make it easy to locate and complete different paperwork.

- US Legal Forms is a reliable service offering legal forms to millions of users since 1997.

You can simply select to search or browse Santa Clara Loan Agreement - Short Form, either by a keyword or by the state/county the document is intended for. After locating necessary form, you can log in and download it or retain it in the My Forms tab.

Don't have an account? It's simple to start! Simply locate the Santa Clara Loan Agreement - Short Form template and take a look at the form's preview and short introductory information (if available). If you're confident about the template’s legalese, go ahead and click Buy now. Create an account and select a subscription plan. The template will be instantly available for download as soon as the payment is completed. Now you can complete the form.

Handling your legal affairs doesn’t have to be pricey or time-consuming. US Legal Forms is here to demonstrate it. Our comprehensive collection of legal forms makes this experience less pricey and more reasonably priced. Create your first business, arrange your advance care planning, create a real estate agreement, or complete the Santa Clara Loan Agreement - Short Form - all from the convenience of your sofa.

Join US Legal Forms now!