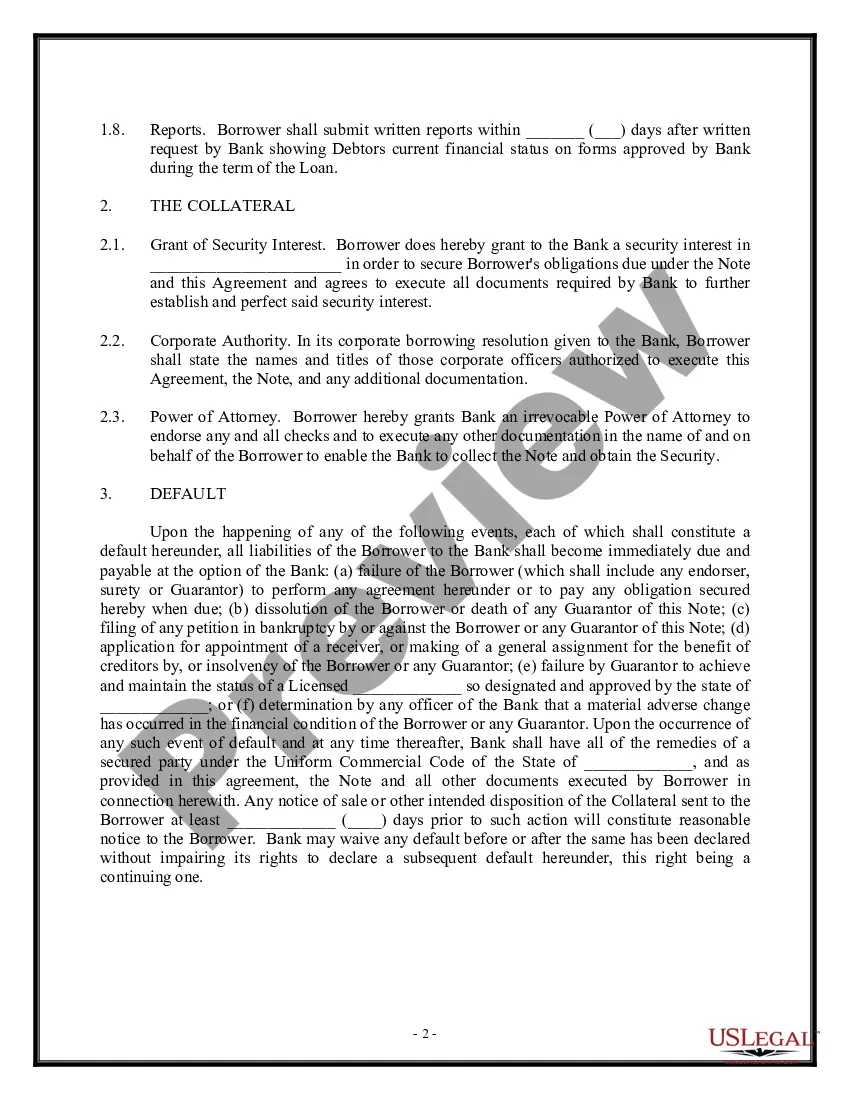

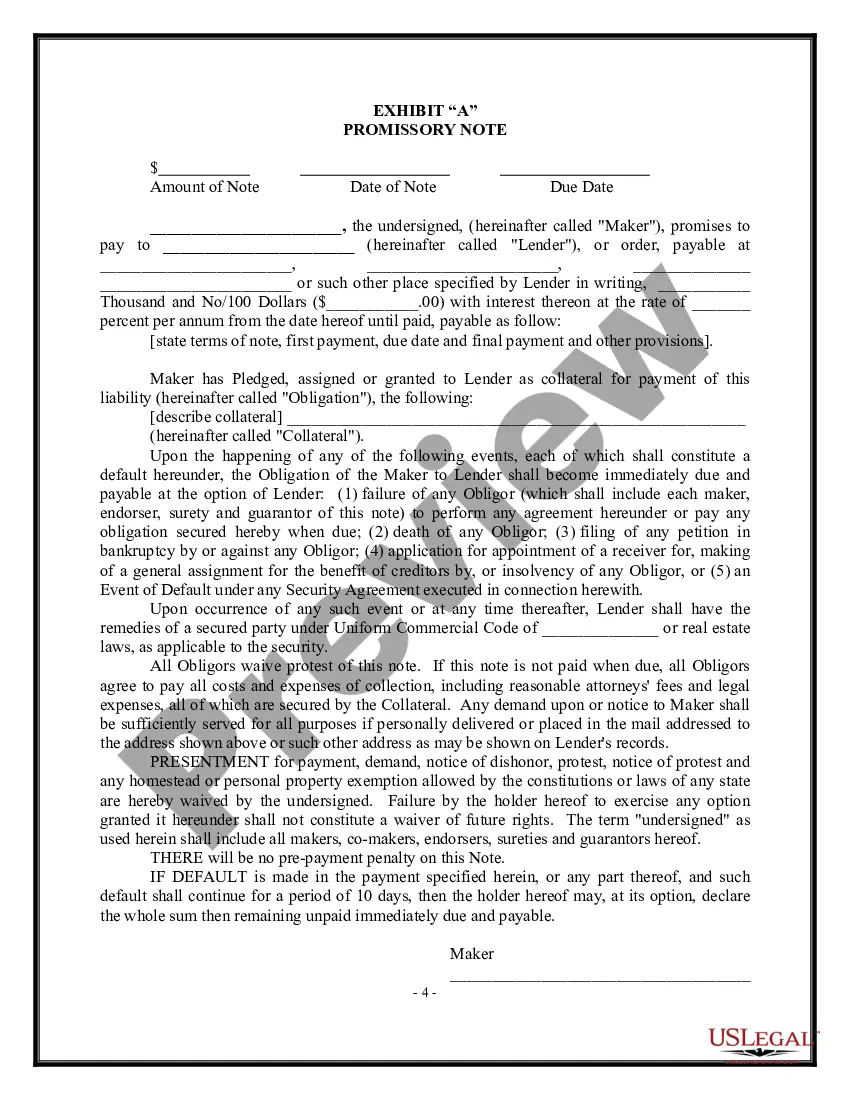

The Wake North Carolina Loan Agreement — Short Form is a legally binding contract between a lender and a borrower in Wake County, North Carolina. This agreement outlines the terms and conditions of a loan, ensuring that both parties fully understand their rights and obligations. Keywords: Loan Agreement, Short Form, Wake North Carolina, lender, borrower, terms and conditions, rights, obligations. This agreement typically includes important details such as: 1. Parties involved: It identifies the lender, who is providing the loan, and the borrower, who is receiving the loan. Both parties' full legal names and addresses are specified in the agreement. 2. Loan amount: The agreement clearly states the exact amount of money being lent to the borrower. It may also include provisions for any additional charges or fees associated with the loan. 3. Interest rate: The agreement specifies the interest rate that will be applied to the loan amount. It defines whether the interest will be fixed or variable and when it will be compounded (if applicable). 4. Repayment terms: This section outlines the repayment plan, including the frequency of payments, the installment amount, and the duration of the loan. It also describes the consequences of missed or late payments, such as additional interest or late fees. 5. Prepayment and default: The agreement may include provisions that allow the borrower to repay the loan in full before the agreed-upon term. It also clarifies the consequences of defaulting on the loan, such as accelerating the repayment or pursuing legal action. 6. Collateral: If the loan is secured by collateral, such as a property or vehicle, the agreement details the collateral's description and value. It specifies the consequences if the borrower fails to meet their obligations, such as the lender's right to seize or sell the collateral. 7. Governing law: It states that the agreement is subject to Wake County, North Carolina's laws, ensuring that any disputes or legal actions relating to the loan will be resolved within this jurisdiction. Different types of Wake North Carolina Loan Agreement — Short Form may include variations based on loan purposes or specific legal considerations, such as: 1. Personal loan agreement: This type of agreement is used when an individual borrows money from another person or a financial institution for personal purposes, such as education, medical expenses, or home renovation. 2. Business loan agreement: When a business seeks financial assistance from a lender, a specific business loan agreement is tailored to address the unique needs and risks associated with commercial transactions. 3. Real estate loan agreement: This agreement is used when a lender provides funds for the purchase or development of a real estate property. It may include additional provisions related to property title, insurance requirements, and construction milestones. Overall, the Wake North Carolina Loan Agreement — Short Form serves to protect both the lender and the borrower by clearly defining the terms and ensuring transparency in the lending process.

Wake North Carolina Loan Agreement - Short Form

Description

How to fill out Wake North Carolina Loan Agreement - Short Form?

How much time does it usually take you to create a legal document? Given that every state has its laws and regulations for every life sphere, locating a Wake Loan Agreement - Short Form suiting all local requirements can be tiring, and ordering it from a professional lawyer is often costly. Numerous web services offer the most popular state-specific templates for download, but using the US Legal Forms library is most beneficial.

US Legal Forms is the most comprehensive web catalog of templates, collected by states and areas of use. In addition to the Wake Loan Agreement - Short Form, here you can get any specific document to run your business or personal affairs, complying with your regional requirements. Experts check all samples for their actuality, so you can be certain to prepare your paperwork correctly.

Using the service is pretty simple. If you already have an account on the platform and your subscription is valid, you only need to log in, pick the required form, and download it. You can get the file in your profile anytime later on. Otherwise, if you are new to the platform, there will be a few more actions to complete before you get your Wake Loan Agreement - Short Form:

- Examine the content of the page you’re on.

- Read the description of the sample or Preview it (if available).

- Search for another document using the related option in the header.

- Click Buy Now once you’re certain in the chosen file.

- Select the subscription plan that suits you most.

- Create an account on the platform or log in to proceed to payment options.

- Pay via PalPal or with your credit card.

- Switch the file format if needed.

- Click Download to save the Wake Loan Agreement - Short Form.

- Print the doc or use any preferred online editor to complete it electronically.

No matter how many times you need to use the acquired document, you can find all the samples you’ve ever saved in your profile by opening the My Forms tab. Give it a try!