- passing of title;

- made with the intent to pass title;

- without receiving money or value in consideration for the passing of title.

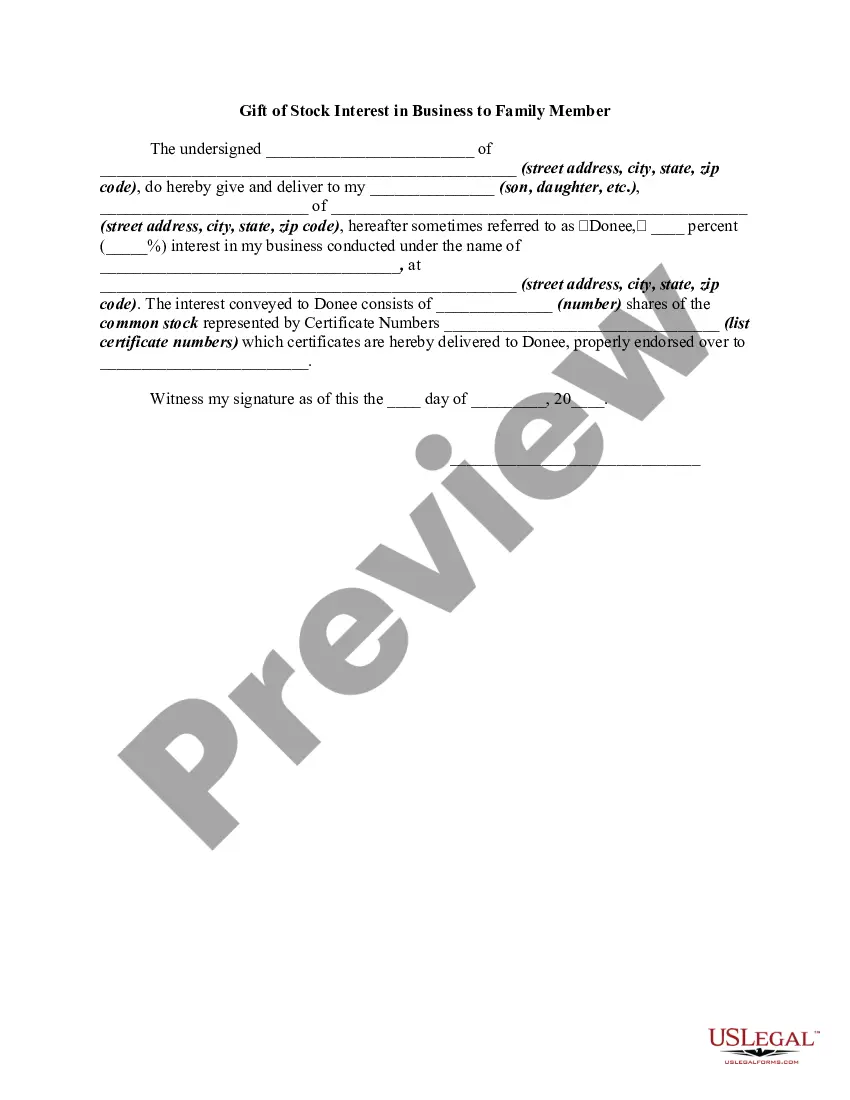

Kings New York Gift of Stock Interest in Business to Family Member refers to the transfer of ownership of shares or stocks in a business from one family member to another as a gift. This type of transaction is commonly undertaken for various reasons, such as succession planning, estate planning, or simply to support a family member's financial or entrepreneurial goals. There are different types of Kings New York Gift of Stock Interest in Business to Family Member, depending on the structure and nature of the transfer. Some commonly known types include: 1. Outright Stock Transfer: This involves the direct transfer of stock ownership from the donor to the recipient, without any conditions or limitations. The recipient becomes the new legal and beneficial owner of the shares immediately. 2. Restricted Stock Transfer: In this type of transfer, the shares are given to the family member but subject to certain restrictions. These restrictions can include a holding period, limitations on selling or transferring the stocks, or other conditions imposed by the donor to protect the business's interests. 3. Minority Interest Transfer: If the family member is being gifted a minority interest in the business, it means they will receive less than 50% ownership. The donor retains the controlling interest, allowing them to continue making critical business decisions. 4. Majority Interest Transfer: In contrast to a minority interest transfer, this type involves gifting a majority stake in the business to the family member. It grants them the power to make significant decisions and potentially control the direction of the company. 5. Voting vs. Non-voting Stock Transfer: If the business has different classes of stock, the donor may choose to gift either voting or non-voting shares. Voting shares give the recipient the right to participate in company decisions and vote on matters brought to shareholder meetings, while non-voting shares limit their influence in governance. 6. Cross-Purchase Agreement: This occurs when multiple family members co-own the business and want to transfer their stock interest to other family members. In this scenario, each co-owner agrees to purchase the shares of others, ensuring an equitable transfer of ownership. When engaging in a Kings New York Gift of Stock Interest in Business to Family Member, it is crucial to seek legal and financial advice to navigate the complexities and ensure compliance with applicable laws and regulations. Additionally, documenting the transfer through a formal agreement can help clarify the terms and conditions, protecting the interests of all parties involved.