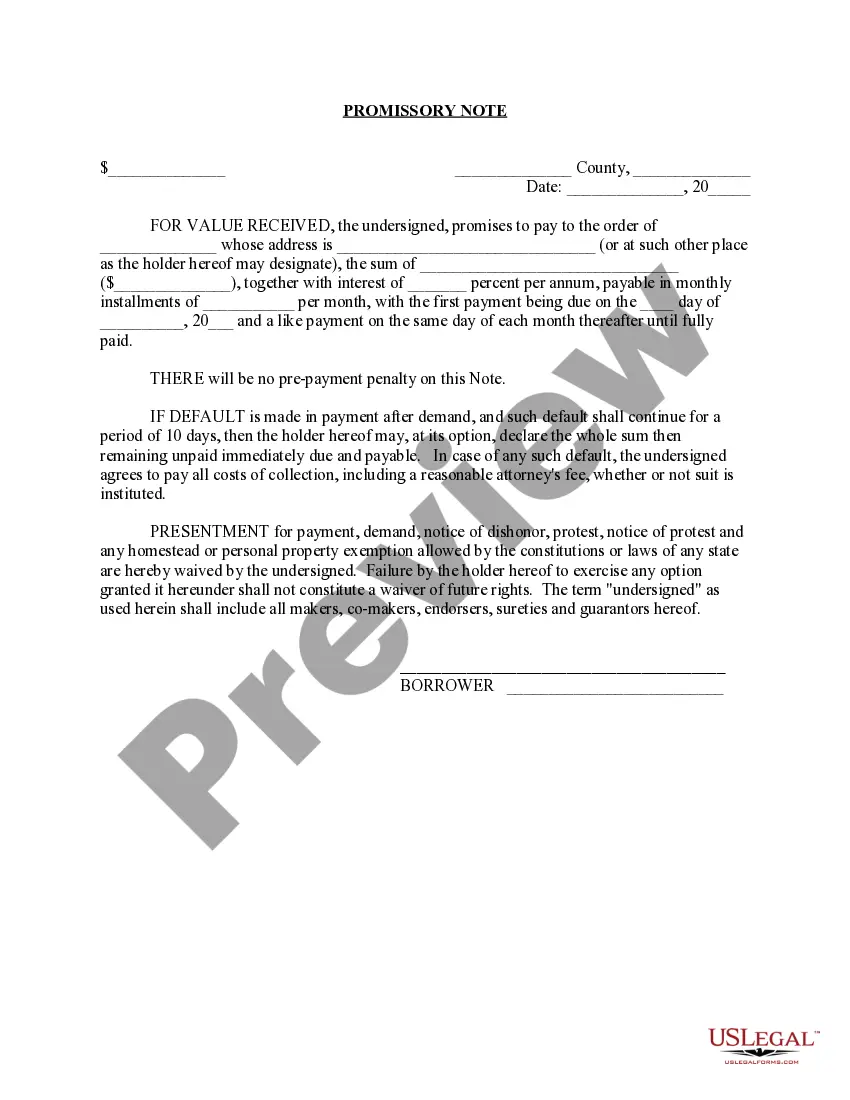

A Cook Illinois Promissory Note with Installment Payments is a legal document outlining the terms and conditions of a loan agreement between a lender and a borrower. This type of promissory note specifically pertains to individuals or entities residing in the state of Illinois, United States. Installment payments refer to the repayment method, where the borrower agrees to make regular payments over a specific period of time until the loan amount, including interest and any additional fees, is fully repaid. The Cook Illinois Promissory Note with Installment Payments provides a detailed description of the loan agreement, including the amount borrowed, the interest rate charged, the repayment schedule, and any consequences for defaulting on payments. This legally binding contract protects both the lender and the borrower, ensuring that the loan amount is repaid in a structured and mutually agreed upon manner. There are various types of Cook Illinois Promissory Notes with Installment Payments that cater to different loan purposes. Some common types include: 1. Personal Loan Promissory Note: This type of promissory note is used when individuals borrow money for personal expenses, such as education, medical bills, or household expenses. 2. Mortgage Promissory Note: When borrowing money for a real estate purchase, the lender may require a mortgage promissory note specifying the terms of the loan, including the property's details and the agreed-upon repayment plan. 3. Business Loan Promissory Note: Entrepreneurs or business owners seeking financial assistance for their ventures may utilize this promissory note type to outline the loan terms, interest rate, repayment schedule, and any collateral involved. 4. Auto Loan Promissory Note: When purchasing a vehicle through financing, this type of promissory note covers the terms and conditions of the auto loan, including repayment options and consequences for late or missed payments. Regardless of the specific type, Cook Illinois Promissory Notes with Installment Payments are crucial documents for both lenders and borrowers. They establish a clear understanding of the loan agreement, protect the rights and interests of all parties involved, and ensure that the loan amount is repaid according to the agreed terms.

Cook Illinois Promissory Note with Installment Payments

Description

How to fill out Cook Illinois Promissory Note With Installment Payments?

Preparing legal paperwork can be burdensome. Besides, if you decide to ask a lawyer to write a commercial agreement, documents for proprietorship transfer, pre-marital agreement, divorce paperwork, or the Cook Promissory Note with Installment Payments, it may cost you a lot of money. So what is the best way to save time and money and draw up legitimate forms in total compliance with your state and local laws? US Legal Forms is a great solution, whether you're looking for templates for your individual or business needs.

US Legal Forms is the most extensive online library of state-specific legal documents, providing users with the up-to-date and professionally checked templates for any use case gathered all in one place. Consequently, if you need the latest version of the Cook Promissory Note with Installment Payments, you can easily find it on our platform. Obtaining the papers takes a minimum of time. Those who already have an account should check their subscription to be valid, log in, and select the sample by clicking on the Download button. If you haven't subscribed yet, here's how you can get the Cook Promissory Note with Installment Payments:

- Look through the page and verify there is a sample for your area.

- Check the form description and use the Preview option, if available, to make sure it's the sample you need.

- Don't worry if the form doesn't suit your requirements - search for the correct one in the header.

- Click Buy Now when you find the needed sample and pick the best suitable subscription.

- Log in or register for an account to pay for your subscription.

- Make a payment with a credit card or via PayPal.

- Opt for the file format for your Cook Promissory Note with Installment Payments and download it.

Once finished, you can print it out and complete it on paper or import the template to an online editor for a faster and more convenient fill-out. US Legal Forms allows you to use all the paperwork ever acquired multiple times - you can find your templates in the My Forms tab in your profile. Try it out now!