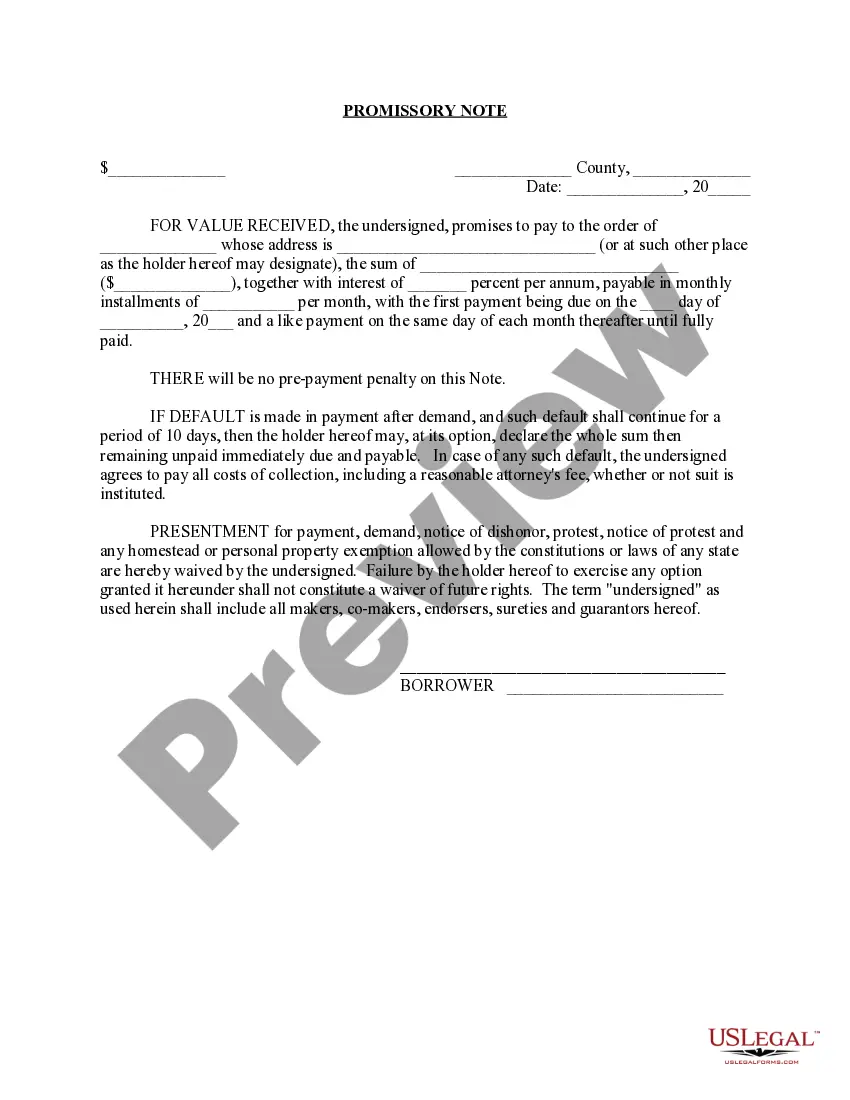

A Harris Texas Promissory Note with Installment Payments is a legally binding document that outlines the terms and conditions of a loan agreement between a lender and a borrower in Harris County, Texas. This note serves as evidence of a debt owed by the borrower to the lender and provides details on how the repayment will take place through scheduled installment payments. The primary purpose of a Harris Texas Promissory Note with Installment Payments is to establish a clear and transparent agreement between the involved parties. It specifies the loan amount, interest rate, repayment schedule, late fees, and any other relevant terms and conditions. The note includes the names and contact information of both the lender and the borrower, ensuring the document's authenticity and enforceability. Different types of Harris Texas Promissory Notes with Installment Payments may exist depending on the specific circumstances and requirements of the parties involved. Some examples include: 1. Personal Loan Promissory Note with Installment Payments: This type of promissory note is commonly used for loans between individuals, such as friends or family members. It facilitates lending arrangements outside traditional financial institutions, allowing for greater flexibility in repayment terms. 2. Business Loan Promissory Note with Installment Payments: Businesses may utilize this type of promissory note when borrowing funds from a lender. It helps establish a formal agreement, specifying the loan amount, interest, and repayment schedule, which is essential for both parties' clarity and protection. 3. Real Estate Promissory Note with Installment Payments: When purchasing a property or engaging in real estate transactions, buyers often use this type of promissory note to outline the terms of a loan granted by the seller. It ensures a structured repayment plan for the buyer, typically including interest and other relevant details. Regardless of the specific type, a Harris Texas Promissory Note with Installment Payments is crucial to safeguarding the rights and obligations of both parties involved in a loan agreement. It acts as a legal contract, protecting the lender's investment and ensuring the borrower's commitment to repayment. Having such a document in place promotes transparency and minimizes the potential for disputes or misunderstandings.

Harris Texas Promissory Note with Installment Payments

Description

How to fill out Harris Texas Promissory Note With Installment Payments?

Laws and regulations in every sphere vary around the country. If you're not an attorney, it's easy to get lost in a variety of norms when it comes to drafting legal documentation. To avoid expensive legal assistance when preparing the Harris Promissory Note with Installment Payments, you need a verified template valid for your county. That's when using the US Legal Forms platform is so advantageous.

US Legal Forms is a trusted by millions web catalog of more than 85,000 state-specific legal templates. It's a great solution for professionals and individuals looking for do-it-yourself templates for various life and business occasions. All the forms can be used multiple times: once you purchase a sample, it remains accessible in your profile for further use. Therefore, when you have an account with a valid subscription, you can simply log in and re-download the Harris Promissory Note with Installment Payments from the My Forms tab.

For new users, it's necessary to make some more steps to get the Harris Promissory Note with Installment Payments:

- Take a look at the page content to make sure you found the correct sample.

- Utilize the Preview option or read the form description if available.

- Search for another doc if there are inconsistencies with any of your requirements.

- Utilize the Buy Now button to obtain the document once you find the proper one.

- Opt for one of the subscription plans and log in or create an account.

- Choose how you prefer to pay for your subscription (with a credit card or PayPal).

- Pick the format you want to save the document in and click Download.

- Complete and sign the document on paper after printing it or do it all electronically.

That's the easiest and most economical way to get up-to-date templates for any legal scenarios. Find them all in clicks and keep your documentation in order with the US Legal Forms!