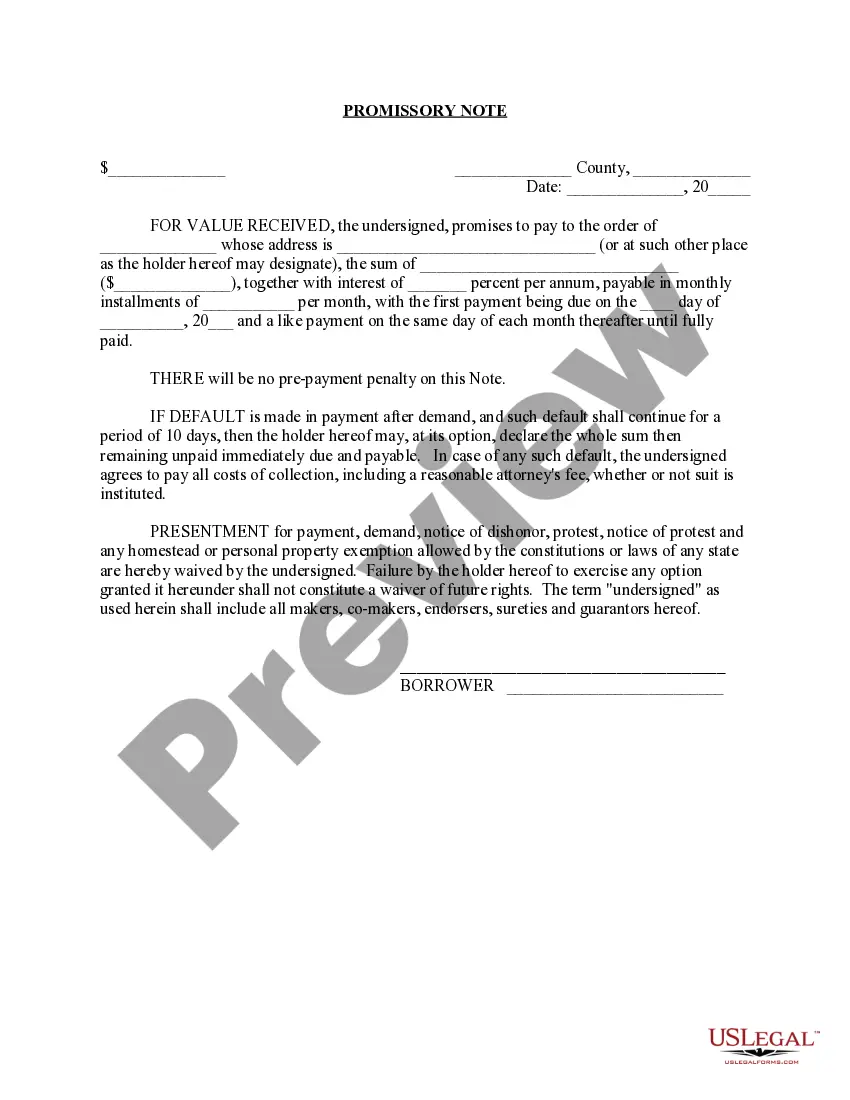

A Wake North Carolina Promissory Note with Installment Payments is a legal document that outlines the terms and conditions of a loan agreement between a lender and a borrower. This promissory note is specifically designed for individuals residing in Wake County, North Carolina, and provides a structured plan for repayment in regular installments. In Wake County, there are different types of promissory notes with installment payments tailored to various specific situations. Some of these include: 1. Wake County Promissory Note with Monthly Installments: This type of promissory note requires the borrower to make monthly payments towards the loan. The note will specify the amount of each installment and the due date. 2. Wake County Promissory Note with Bi-Weekly Installments: This promissory note requires the borrower to make payments every two weeks. This frequency allows for quicker repayment and is suitable for individuals with a bi-weekly income. 3. Wake County Promissory Note with Quarterly Installments: For borrowers who prefer a less frequent payment cycle, this type of note allows for payments to be made every three months. It provides flexibility for borrowers who receive income at a quarterly interval. 4. Wake County Promissory Note with Balloon Payment: This note structure involves regular installments for a specific duration, but with a large final payment known as a balloon payment. It is ideal for borrowers who anticipate a substantial sum of money coming in near the end of the loan term. 5. Wake County Promissory Note with Variable Installments: In this type of note, the installment amount may vary over time based on a predetermined formula or percentage. It allows flexibility for borrowers whose income fluctuates, such as those in seasonal employment. Regardless of the specific type, a Wake North Carolina Promissory Note with Installment Payments typically includes essential details such as the loan amount, interest rate, installment schedule, late payment penalties, and any collateral involved. Both the lender and the borrower must carefully review and agree to the terms outlined in the promissory note before signing to ensure both parties are protected throughout the loan repayment process.

Wake North Carolina Promissory Note with Installment Payments

Description

How to fill out Wake North Carolina Promissory Note With Installment Payments?

Preparing legal documentation can be burdensome. In addition, if you decide to ask an attorney to draft a commercial contract, documents for proprietorship transfer, pre-marital agreement, divorce papers, or the Wake Promissory Note with Installment Payments, it may cost you a fortune. So what is the best way to save time and money and draft legitimate forms in total compliance with your state and local laws and regulations? US Legal Forms is a great solution, whether you're looking for templates for your personal or business needs.

US Legal Forms is the most extensive online library of state-specific legal documents, providing users with the up-to-date and professionally verified templates for any use case collected all in one place. Therefore, if you need the current version of the Wake Promissory Note with Installment Payments, you can easily locate it on our platform. Obtaining the papers requires a minimum of time. Those who already have an account should check their subscription to be valid, log in, and select the sample using the Download button. If you haven't subscribed yet, here's how you can get the Wake Promissory Note with Installment Payments:

- Glance through the page and verify there is a sample for your region.

- Check the form description and use the Preview option, if available, to ensure it's the sample you need.

- Don't worry if the form doesn't suit your requirements - search for the right one in the header.

- Click Buy Now when you find the needed sample and select the best suitable subscription.

- Log in or register for an account to purchase your subscription.

- Make a payment with a credit card or through PayPal.

- Choose the document format for your Wake Promissory Note with Installment Payments and save it.

When done, you can print it out and complete it on paper or import the samples to an online editor for a faster and more practical fill-out. US Legal Forms allows you to use all the documents ever purchased multiple times - you can find your templates in the My Forms tab in your profile. Try it out now!