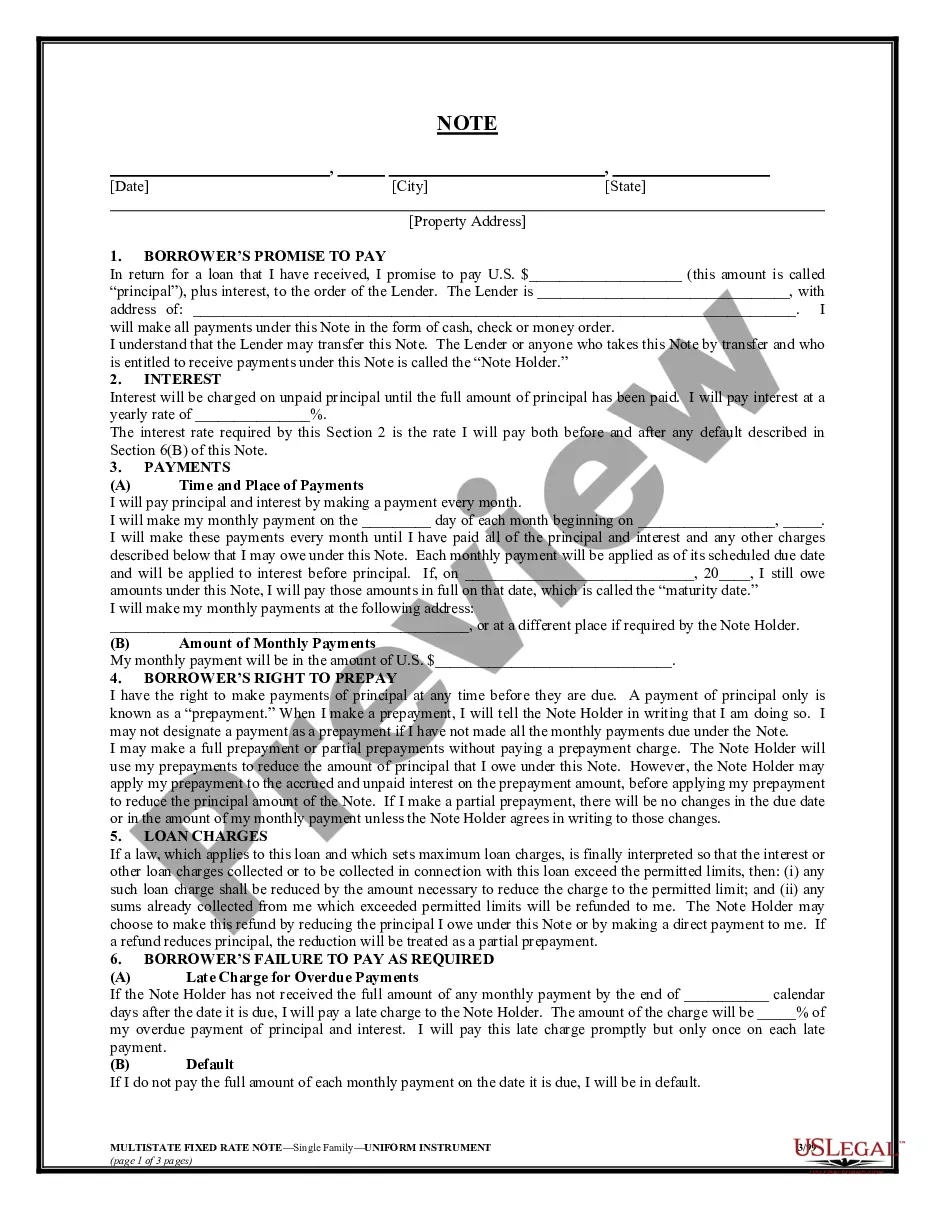

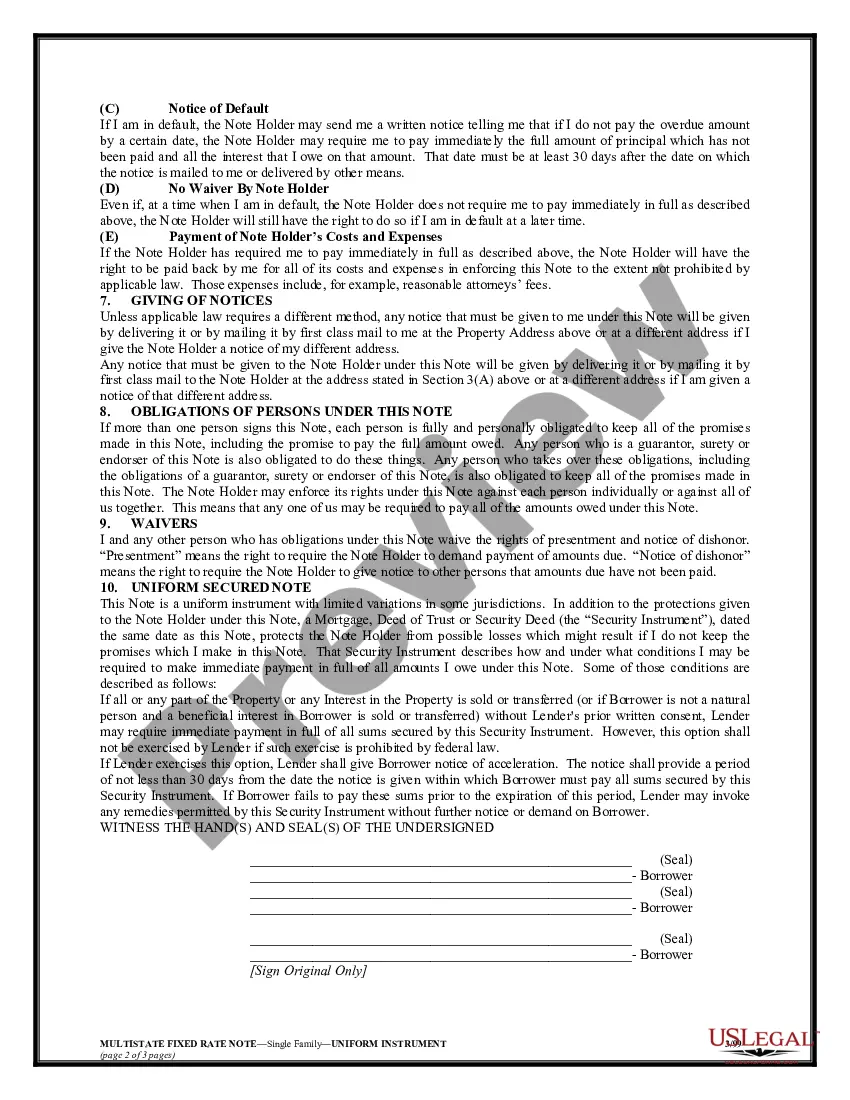

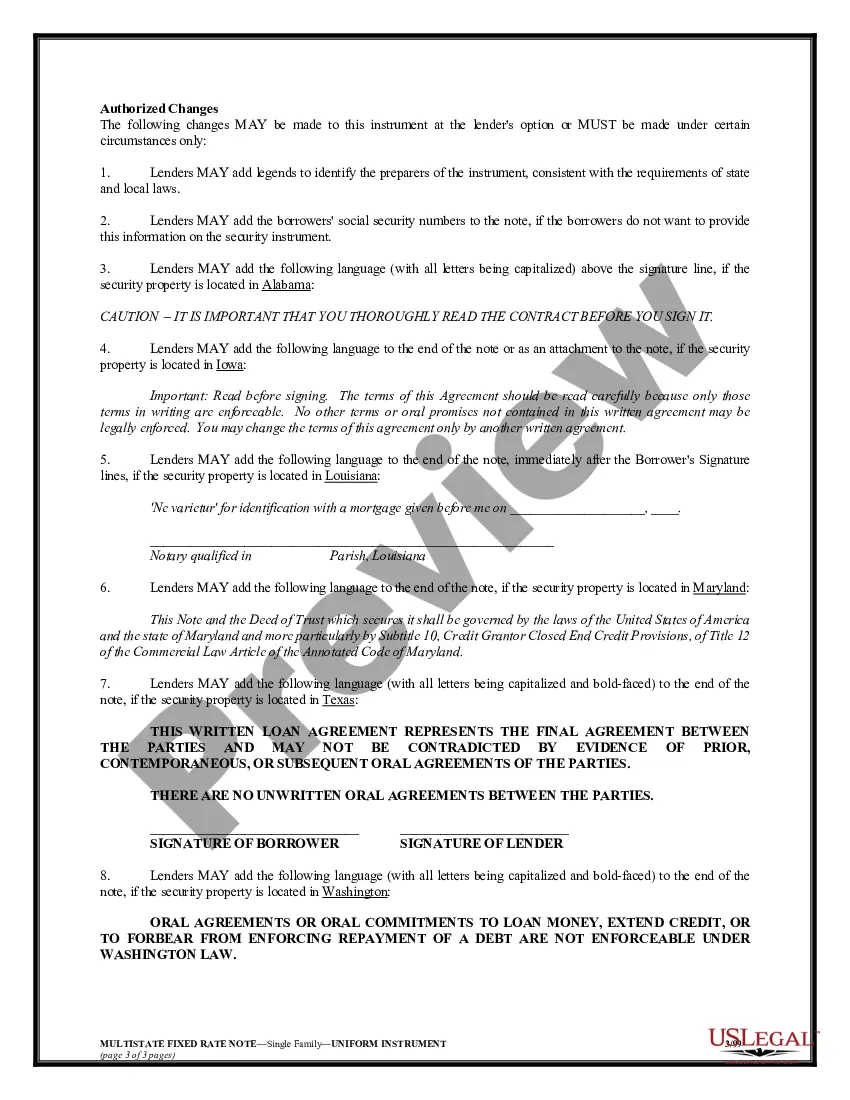

The Hillsborough Florida Multistate Promissory Note — Secured is a legally binding financial document that individuals or entities can use when lending money in the state of Florida. This note provides a detailed agreement between the lender (known as the "Payee") and the borrower (known as the "Maker"). A secured promissory note means that the borrower pledges collateral to secure the loan, which gives the lender a legal right to claim and sell the collateral in the event of non-payment. This provides added protection for lenders and can potentially result in lower interest rates for borrowers. There are different types of Hillsborough Florida Multistate Promissory Note — Secured, including: 1. Real Estate Secured Promissory Note: This specific type of secured promissory note is commonly used for real estate transactions. It outlines the terms and conditions of a loan related to the purchase, refinancing, or renovation of a property. The note is secured by the property itself, meaning that if the borrower defaults, the lender has a right to foreclose on the property. 2. Vehicle Secured Promissory Note: This type of secured promissory note is used for financing the purchase of a vehicle. The note outlines the loan amount, interest rate, repayment terms, and the vehicle being used as collateral. If the borrower fails to repay the loan, the lender has the right to repossess and sell the vehicle to recover their funds. 3. Business Secured Promissory Note: This variant of the Hillsborough Florida Multistate Promissory Note — Secured is designed for business-related loans. It includes provisions for securing the loan with business assets, such as inventory, equipment, or accounts receivable. If the borrower defaults, the lender can seize and sell these assets to recover the outstanding debt. It is important for both parties involved in a Hillsborough Florida Multistate Promissory Note — Secured to thoroughly review and understand the document before signing. Consider engaging legal counsel to ensure compliance with state laws and to protect both the lender and the borrower's rights and interests.

Hillsborough Florida Multistate Promissory Note - Secured

Description

How to fill out Hillsborough Florida Multistate Promissory Note - Secured?

Whether you plan to start your business, enter into a deal, apply for your ID renewal, or resolve family-related legal issues, you must prepare certain paperwork corresponding to your local laws and regulations. Finding the correct papers may take a lot of time and effort unless you use the US Legal Forms library.

The platform provides users with more than 85,000 professionally drafted and verified legal templates for any personal or business occurrence. All files are grouped by state and area of use, so opting for a copy like Hillsborough Multistate Promissory Note - Secured is quick and simple.

The US Legal Forms library users only need to log in to their account and click the Download key next to the required template. If you are new to the service, it will take you a few more steps to obtain the Hillsborough Multistate Promissory Note - Secured. Follow the guidelines below:

- Make sure the sample fulfills your individual needs and state law regulations.

- Look through the form description and check the Preview if available on the page.

- Make use of the search tab specifying your state above to locate another template.

- Click Buy Now to obtain the sample when you find the proper one.

- Choose the subscription plan that suits you most to proceed.

- Log in to your account and pay the service with a credit card or PayPal.

- Download the Hillsborough Multistate Promissory Note - Secured in the file format you need.

- Print the copy or fill it out and sign it electronically via an online editor to save time.

Documents provided by our library are reusable. Having an active subscription, you are able to access all of your previously acquired paperwork whenever you need in the My Forms tab of your profile. Stop wasting time on a endless search for up-to-date formal documents. Sign up for the US Legal Forms platform and keep your paperwork in order with the most comprehensive online form library!