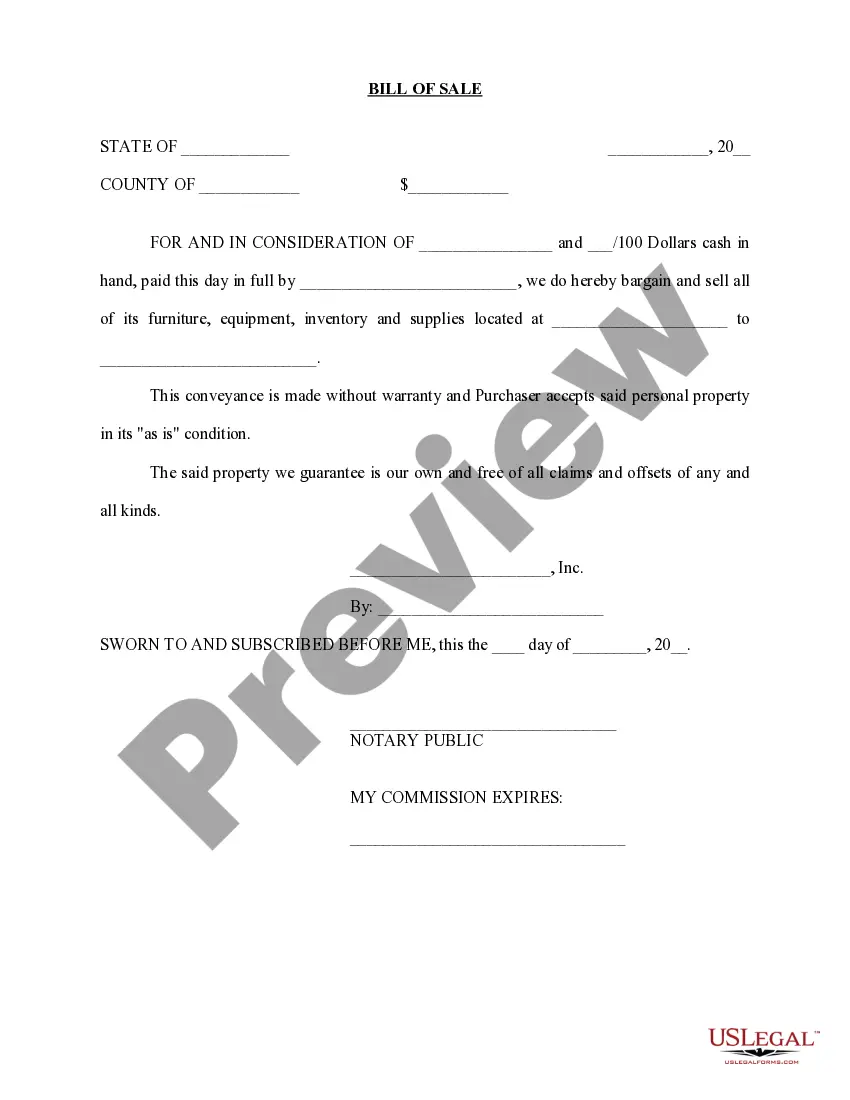

Contra Costa California Sale of Business: Bill of Sale for Personal Assets — Asset Purchase Transaction In Contra Costa County, California, the process of selling a business and transferring personal assets requires a comprehensive legal document known as the "Bill of Sale for Personal Assets — Asset Purchase Transaction." This document serves as a binding agreement between the buyer and seller, outlining the specifics of the transaction and ensuring a smooth transfer of assets. The Contra Costa California Sale of Business — Bill of Sale for Personal Asset— - Asset Purchase Transaction covers a wide range of personal assets, including but not limited to: 1. Tangible Assets: This category includes physical items such as equipment, machinery, furniture, vehicles, inventory, and other tangible property that are part of the business's operations. The bill of sale ensures the transfer of ownership for these assets from the seller to the buyer. 2. Intangible Assets: Intangible assets refer to non-physical assets with value, such as trademarks, copyrights, patents, trade secrets, client lists, goodwill, and proprietary software. The bill of sale reflects the transfer of these assets and establishes their ownership under the new business owner. 3. Contracts and Agreements: Contracts and agreements associated with the business, such as lease agreements, supplier contracts, customer contracts, and licensing agreements, need to be addressed in the bill of sale. It ensures that these contracts are assigned to the buyer and that both parties understand their responsibilities. 4. Intellectual Property: The bill of sale should outline the transfer of any intellectual property assets, including trademarks, copyrights, and patents. This protects the buyer from any legal issues or claims related to these assets in the future. 5. Liabilities and Debts: The bill of sale should clearly define the liabilities and debts associated with the business. It ensures that the buyer is aware of any outstanding debts or obligations and understands their responsibility for them after the purchase. Different types of Contra Costa California Sale of Business — Bill of Sale for Personal Asset— - Asset Purchase Transaction may include variations tailored to specific industries or unique circumstances such as: 1. Real Estate Assets: If the business includes real estate property, a separate section or addendum may be added to the bill of sale to address the transfer of ownership and associated documents. 2. Financial Assets: In cases where the business holds financial assets like stocks, bonds, or investment portfolios, additional provisions may be included to outline their transfer and any necessary legal processes. 3. Licensing of Technology: If the business deals with proprietary technology, software, or patents, the bill of sale may include specific clauses regarding licensing agreements, restrictions, and legal requirements. It is crucial to consult with experienced legal professionals or business advisors familiar with Contra Costa California's sale of business laws to ensure the bill of sale accurately reflects all necessary components and protects the interests of both the buyer and seller.

Contra Costa California Sale of Business - Bill of Sale for Personal Assets - Asset Purchase Transaction

Description

How to fill out Contra Costa California Sale Of Business - Bill Of Sale For Personal Assets - Asset Purchase Transaction?

If you need to find a reliable legal form supplier to get the Contra Costa Sale of Business - Bill of Sale for Personal Assets - Asset Purchase Transaction, look no further than US Legal Forms. Whether you need to start your LLC business or take care of your belongings distribution, we got you covered. You don't need to be knowledgeable about in law to find and download the appropriate form.

- You can select from over 85,000 forms categorized by state/county and situation.

- The self-explanatory interface, number of learning resources, and dedicated support make it easy to get and complete various paperwork.

- US Legal Forms is a reliable service offering legal forms to millions of users since 1997.

You can simply type to search or browse Contra Costa Sale of Business - Bill of Sale for Personal Assets - Asset Purchase Transaction, either by a keyword or by the state/county the document is intended for. After finding the required form, you can log in and download it or retain it in the My Forms tab.

Don't have an account? It's simple to get started! Simply find the Contra Costa Sale of Business - Bill of Sale for Personal Assets - Asset Purchase Transaction template and check the form's preview and short introductory information (if available). If you're confident about the template’s language, go ahead and hit Buy now. Register an account and choose a subscription option. The template will be immediately ready for download once the payment is completed. Now you can complete the form.

Handling your legal matters doesn’t have to be expensive or time-consuming. US Legal Forms is here to demonstrate it. Our comprehensive collection of legal forms makes this experience less expensive and more affordable. Create your first business, arrange your advance care planning, draft a real estate contract, or execute the Contra Costa Sale of Business - Bill of Sale for Personal Assets - Asset Purchase Transaction - all from the convenience of your home.

Join US Legal Forms now!