The Fairfax Virginia Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale is a legal process that occurs when one partner in a business passes away, and their ownership or equity in the company needs to be transferred to the surviving partner. This type of transaction requires the creation of a Purchase Agreement and a Bill of Sale to document the transfer of ownership. The Purchase Agreement is a legally binding contract that outlines the terms and conditions of the sale. It includes important details such as the names and addresses of the parties involved, the purchase price, the percentage of ownership being transferred, and any additional terms or contingencies. The Bill of Sale, on the other hand, is a legal document that provides evidence of the transfer of ownership from the deceased partner to the surviving partner. It includes the names and addresses of the parties, a description of the property being transferred (i.e., the deceased partner's interest in the business), the purchase price, and any warranties or representations made by the seller. In Fairfax Virginia, there may be different types or variations of the Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale. Listed below are a few possible scenarios: 1. Sole Proprietorship: If the business was organized as a sole proprietorship, the deceased partner's interest would transfer to the surviving partner without the need for a Purchase Agreement and Bill of Sale. Instead, the surviving partner would assume full ownership of the business automatically, subject to any legal requirements or obligations. 2. Partnership Agreement: If the business was organized as a partnership and had a partnership agreement in place that addressed the sale of a deceased partner's interest, the terms of the agreement would typically govern the transaction. The Purchase Agreement and Bill of Sale would be structured accordingly, following the guidelines set forth in the partnership agreement. 3. Limited Liability Company (LLC): If the business was organized as an LLC, the sale of a deceased partner's interest would be subject to the operating agreement. The terms outlined in the operating agreement would guide the creation of the Purchase Agreement and Bill of Sale, ensuring compliance with the legal requirements of Fairfax Virginia. In any case, it is crucial for all parties involved to seek legal counsel to ensure that all legal obligations are met and the transaction is conducted in accordance with Fairfax Virginia's laws and regulations. The Purchase Agreement and Bill of Sale should be drafted by knowledgeable attorneys and signed by both parties to establish a clear and enforceable transfer of ownership. (Note: It is important to consult with a legal professional or attorney when dealing with specific legal matters, as the information provided here is for general guidance only.)

Fairfax Virginia Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale

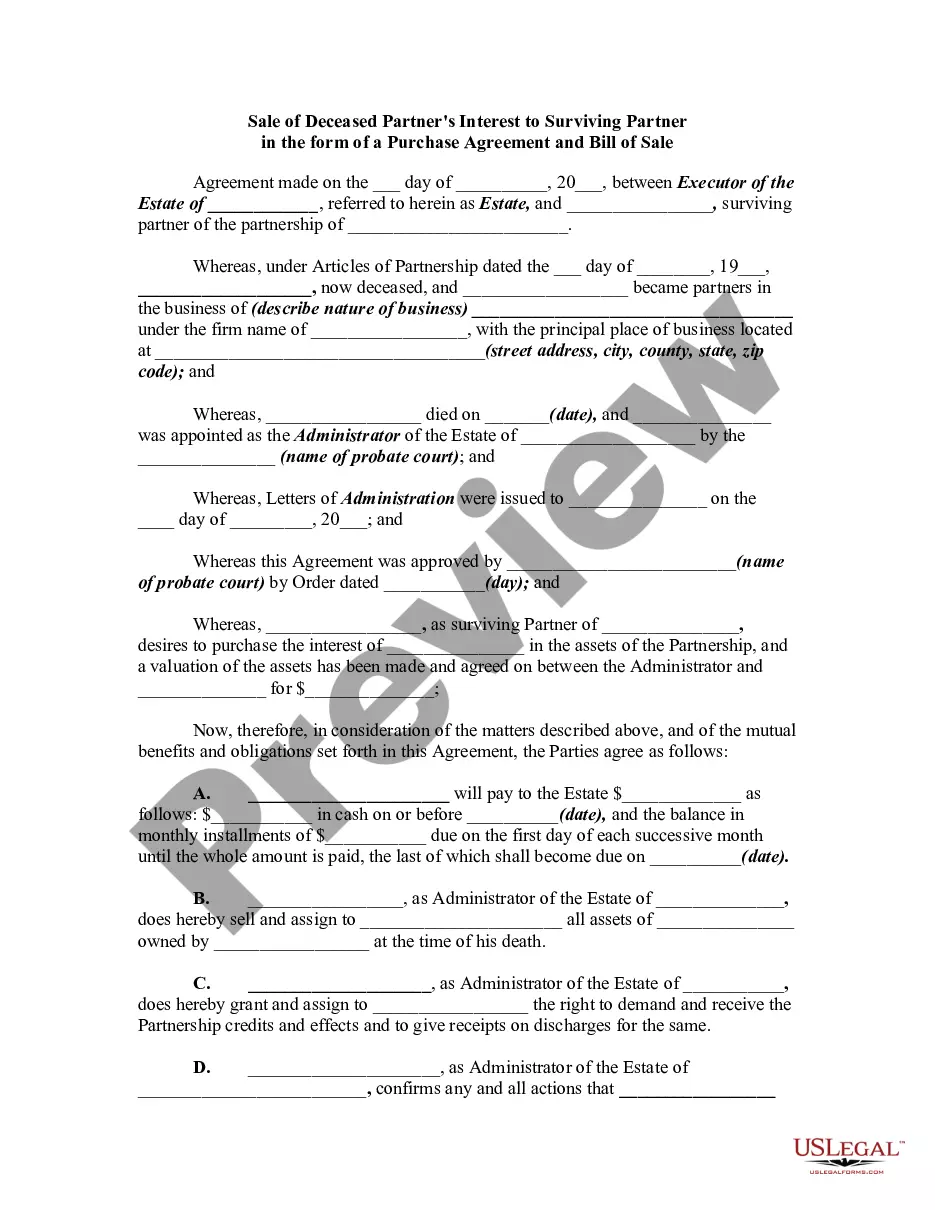

Description

How to fill out Fairfax Virginia Sale Of Deceased Partner's Interest To Surviving Partner In The Form Of A Purchase Agreement And Bill Of Sale?

Drafting papers for the business or individual demands is always a big responsibility. When creating an agreement, a public service request, or a power of attorney, it's crucial to consider all federal and state laws of the specific area. However, small counties and even cities also have legislative provisions that you need to consider. All these aspects make it burdensome and time-consuming to draft Fairfax Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale without professional help.

It's easy to avoid spending money on attorneys drafting your paperwork and create a legally valid Fairfax Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale by yourself, using the US Legal Forms web library. It is the greatest online collection of state-specific legal templates that are professionally verified, so you can be certain of their validity when picking a sample for your county. Previously subscribed users only need to log in to their accounts to save the needed form.

In case you still don't have a subscription, follow the step-by-step instruction below to obtain the Fairfax Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale:

- Examine the page you've opened and verify if it has the sample you require.

- To accomplish this, use the form description and preview if these options are presented.

- To locate the one that suits your requirements, utilize the search tab in the page header.

- Recheck that the template complies with juridical criteria and click Buy Now.

- Opt for the subscription plan, then sign in or register for an account with the US Legal Forms.

- Utilize your credit card or PayPal account to pay for your subscription.

- Download the selected file in the preferred format, print it, or complete it electronically.

The great thing about the US Legal Forms library is that all the paperwork you've ever purchased never gets lost - you can access it in your profile within the My Forms tab at any time. Join the platform and quickly obtain verified legal forms for any scenario with just a few clicks!