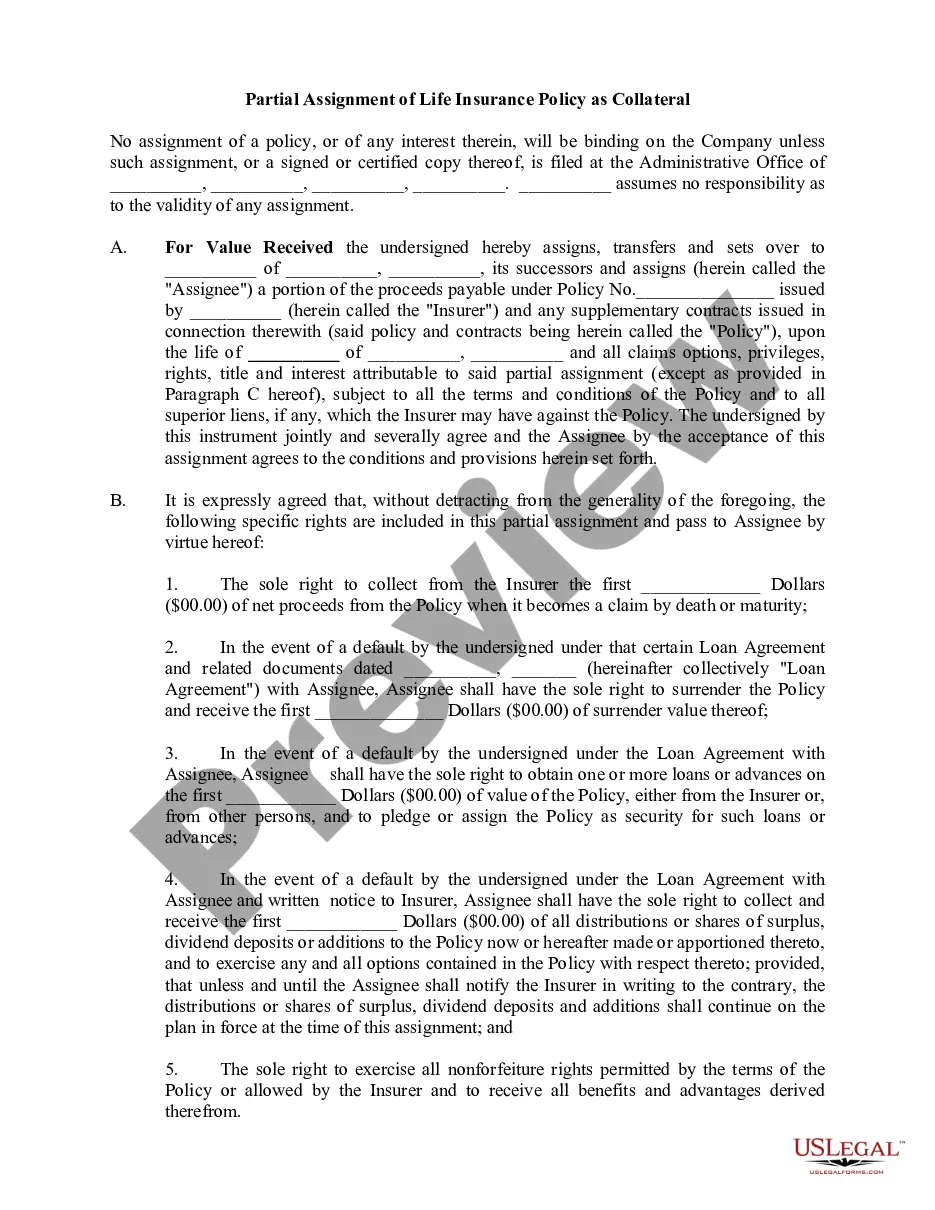

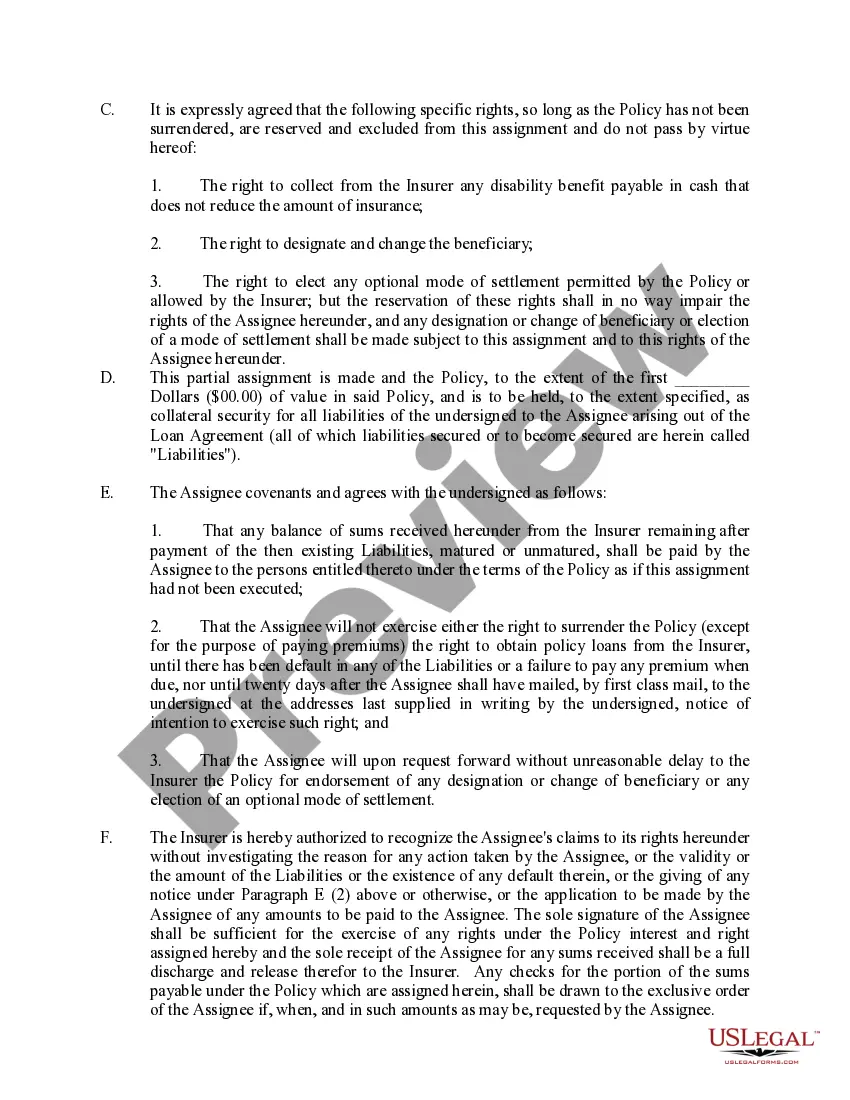

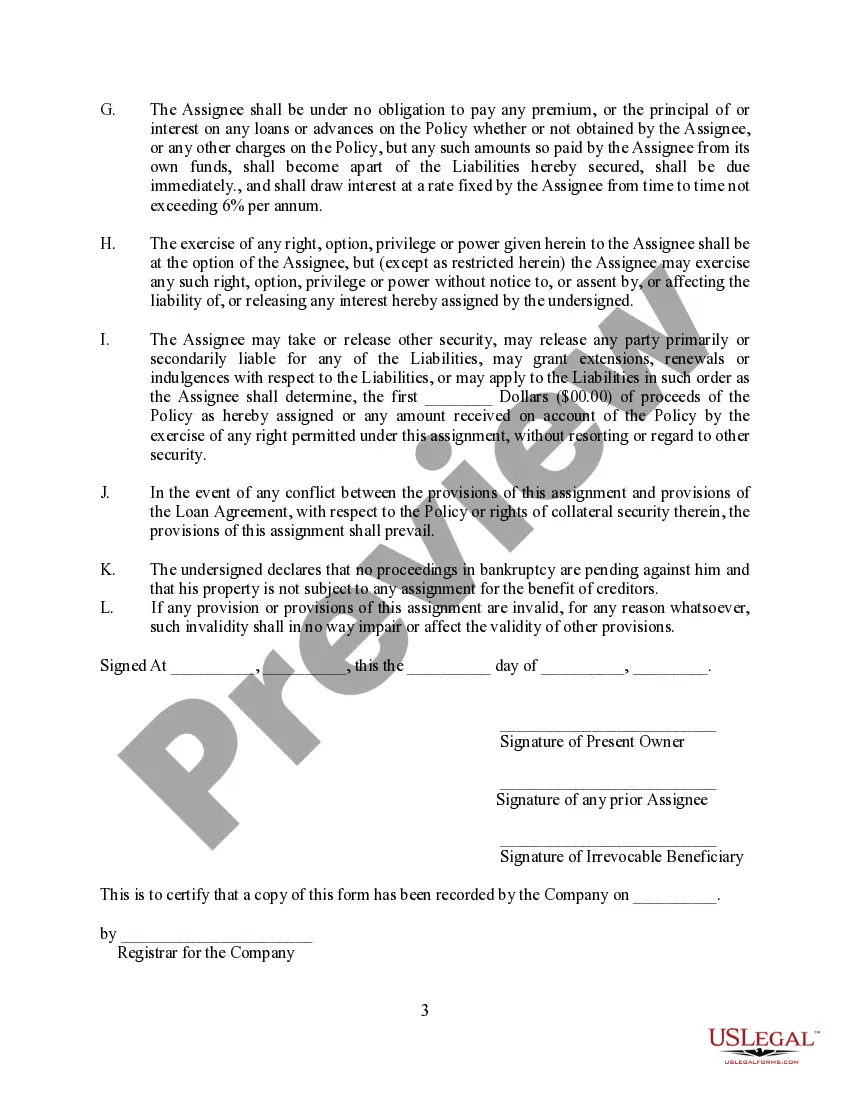

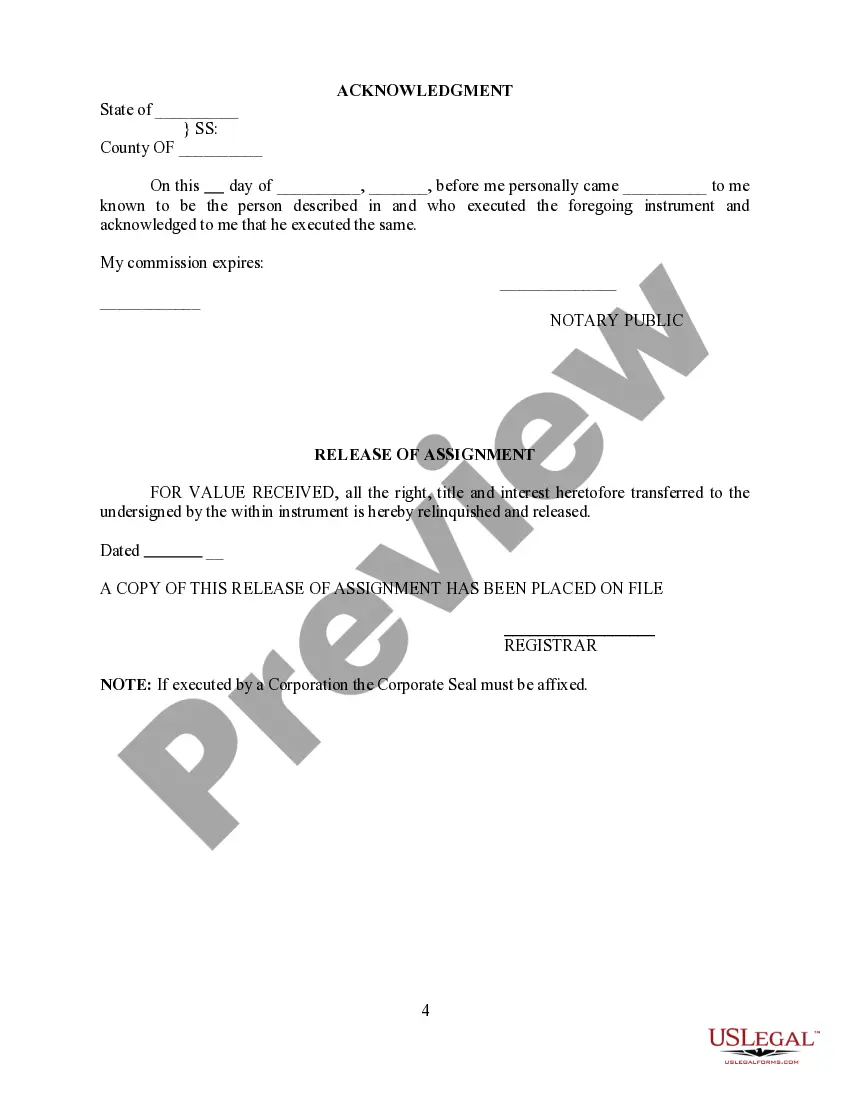

Broward Florida Partial Assignment of Life Insurance Policy as Collateral is a financial arrangement in which a portion of the value of a life insurance policy is used as collateral for a loan or debt. This type of agreement involves transferring a partial interest in the life insurance policy to a lender as security for repayment. It is an alternative to other forms of collateral, such as real estate or vehicles. There are various types of Broward Florida Partial Assignment of Life Insurance Policy as Collateral, each with its own specific features and purposes: 1. Term Life Insurance Collateral Assignment: This type of assignment involves using a term life insurance policy as collateral. The insurer guarantees a predetermined death benefit for a specific term, and the lender's interest is limited to that period. If the policyholder dies within the term, the lender is repaid from the policy proceeds. 2. Whole Life Insurance Collateral Assignment: With a whole life insurance policy, the policyholder can use the accumulated cash value as collateral. This type of assignment is commonly used in situations where a policyholder wishes to borrow against the policy while keeping it in force. 3. Universal Life Insurance Collateral Assignment: Similar to whole life insurance, universal life policies allow for the assignment of cash value as collateral. However, universal life offers more flexibility in premium payments and death benefits, making it an attractive option for those seeking collateralized loans. 4. Variable Life Insurance Collateral Assignment: Variable life insurance policies allow policyholders to allocate premiums into investment accounts, offering the potential for higher returns. With this type of assignment, the policy's cash value fluctuates based on the performance of the underlying investments. Broward Florida Partial Assignment of Life Insurance Policy as Collateral provides borrowers with a means to secure loans while leveraging the value of their life insurance policies. This arrangement benefits lenders by minimizing risk and ensuring repayments through the policy's death benefit or cash value. However, it is essential for policyholders to carefully consider the potential impact on their coverage and consult with financial professionals for comprehensive guidance.

Broward Florida Partial Assignment of Life Insurance Policy as Collateral

Description

How to fill out Broward Florida Partial Assignment Of Life Insurance Policy As Collateral?

Preparing legal documentation can be difficult. Besides, if you decide to ask a legal professional to write a commercial agreement, papers for proprietorship transfer, pre-marital agreement, divorce papers, or the Broward Partial Assignment of Life Insurance Policy as Collateral, it may cost you a fortune. So what is the most reasonable way to save time and money and draw up legitimate documents in total compliance with your state and local regulations? US Legal Forms is a perfect solution, whether you're looking for templates for your individual or business needs.

US Legal Forms is largest online collection of state-specific legal documents, providing users with the up-to-date and professionally checked forms for any use case collected all in one place. Consequently, if you need the latest version of the Broward Partial Assignment of Life Insurance Policy as Collateral, you can easily find it on our platform. Obtaining the papers takes a minimum of time. Those who already have an account should check their subscription to be valid, log in, and pick the sample using the Download button. If you haven't subscribed yet, here's how you can get the Broward Partial Assignment of Life Insurance Policy as Collateral:

- Look through the page and verify there is a sample for your region.

- Examine the form description and use the Preview option, if available, to make sure it's the sample you need.

- Don't worry if the form doesn't satisfy your requirements - search for the correct one in the header.

- Click Buy Now once you find the needed sample and select the best suitable subscription.

- Log in or sign up for an account to pay for your subscription.

- Make a payment with a credit card or through PayPal.

- Opt for the file format for your Broward Partial Assignment of Life Insurance Policy as Collateral and download it.

Once done, you can print it out and complete it on paper or import the template to an online editor for a faster and more practical fill-out. US Legal Forms enables you to use all the paperwork ever obtained many times - you can find your templates in the My Forms tab in your profile. Try it out now!