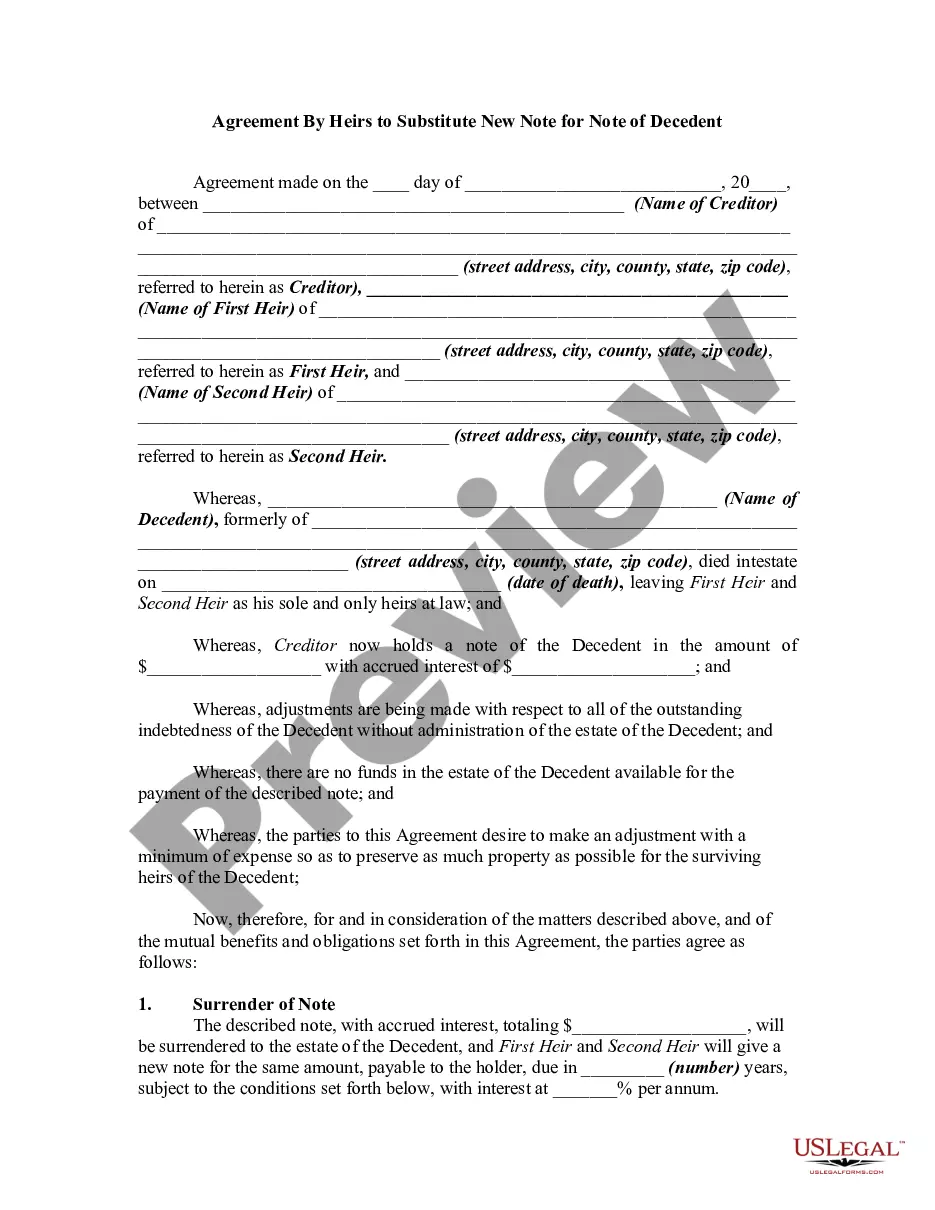

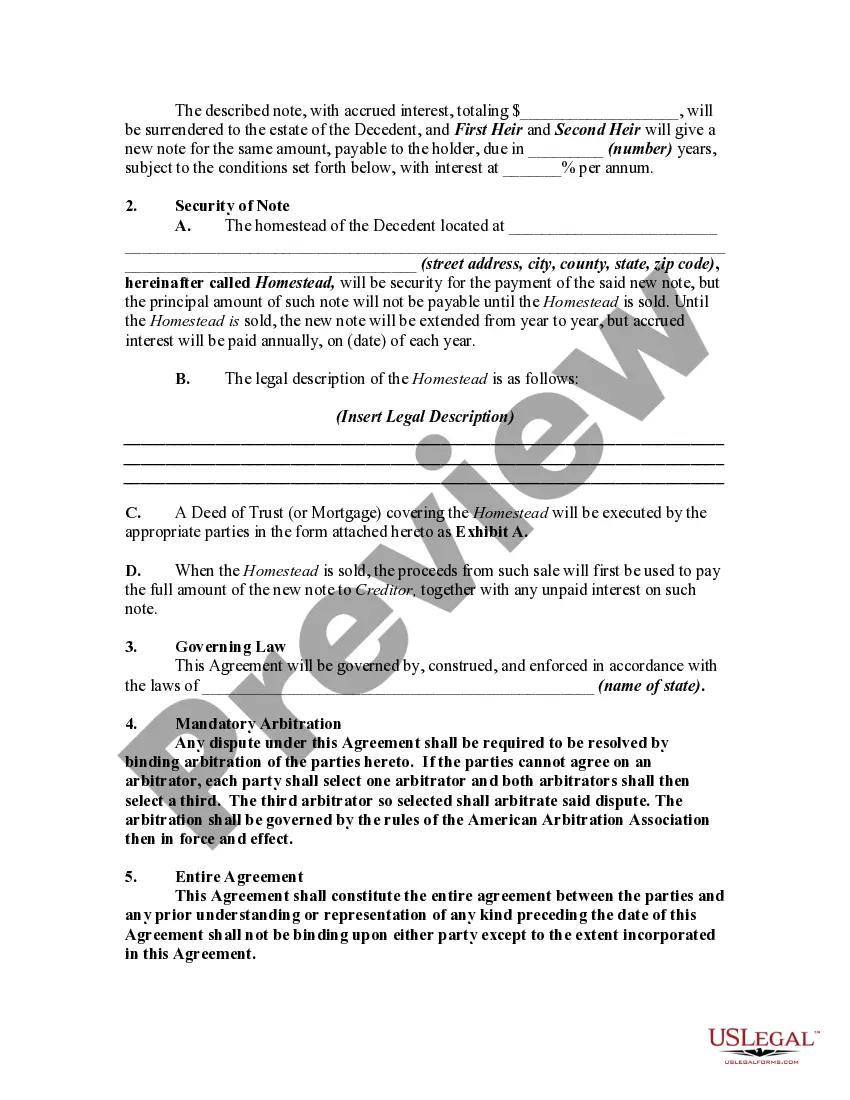

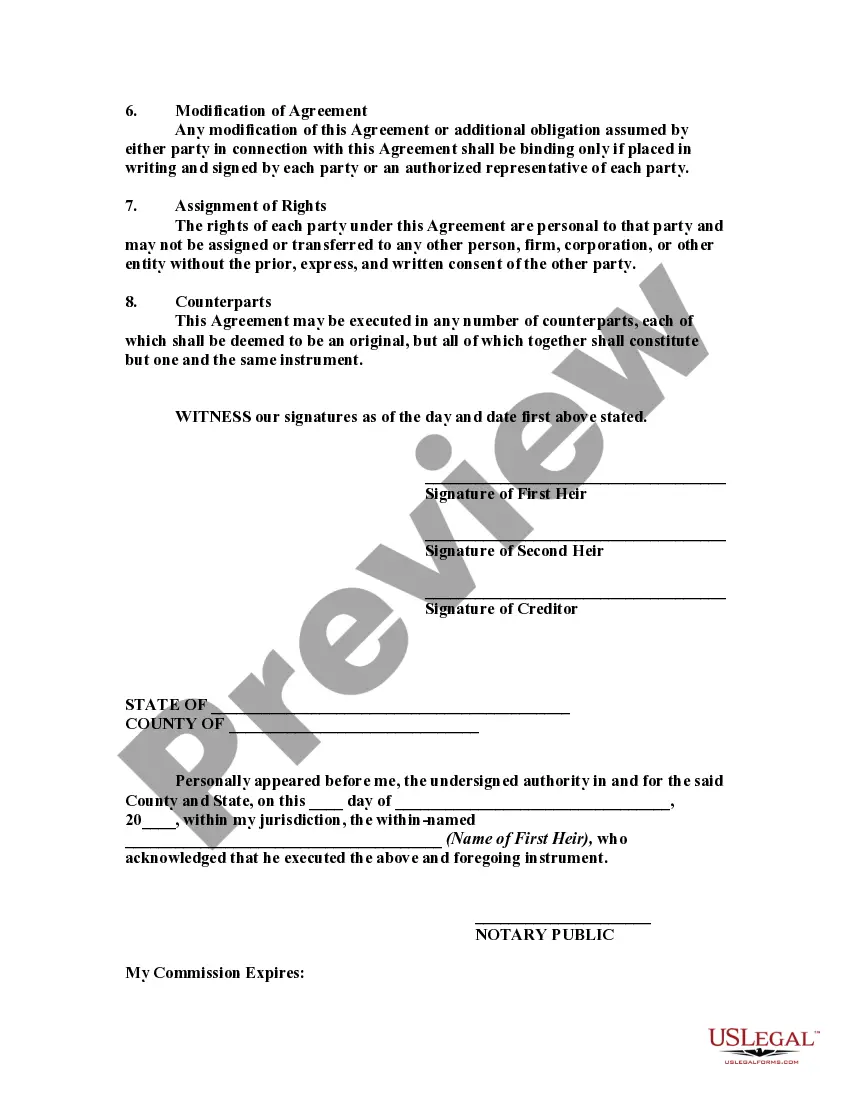

In this form, the heirs at law of an intestate estate are substituting their note for a note of the decedent. Intestate means that the decedent died without a valid will. The term heirs-at-law is used to refer to those who would inherit under the state statute of descent and distribution if the decedent dies intestate.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Fulton Georgia Agreement By Heirs to Substitute New Note for Note of Decedent is a legal document that allows the heirs of a deceased person to replace the existing note (loan) held by the decedent with a new note. This agreement is entered into when the decedent was a party to a loan transaction, and after their passing, the heirs wish to assume the rights and responsibilities of the original note. The purpose of the Fulton Georgia Agreement By Heirs to Substitute New Note for Note of Decedent is to provide a legal framework for the heirs to substitute the old note with a new one, ensuring the continuity of the loan without causing disruptions or default. This agreement acts as a guarantee that the new note will be treated and repaid in the same manner as the original note. The Fulton Georgia Agreement By Heirs to Substitute New Note for Note of Decedent protects the interests of all involved parties. It outlines the terms and conditions of the new note, such as the principal amount, interest rate, repayment schedule, and any other relevant provisions. The heirs assume the same obligations the decedent had, and the lender agrees to transfer the existing loan and accept the new note. Different types of Fulton Georgia Agreement By Heirs to Substitute New Note for Note of Decedent may include variations in the terms and conditions depending on the specific circumstances. Some key types may include: 1. Residential Property Agreement By Heirs to Substitute New Note for Note of Decedent: This type of agreement applies when the decedent was the borrower in a residential property loan. The heirs agree to substitute the existing note with a new note to ensure the continuation of the loan while abiding by the applicable residential property regulations. 2. Commercial Property Agreement By Heirs to Substitute New Note for Note of Decedent: If the decedent was a party to a loan related to a commercial property, this type of agreement is utilized. The heirs replace the previous note with a new one, maintaining the terms and conditions of the original loan while adapting to the specific requirements of commercial property transactions. 3. Vehicle Loan Agreement By Heirs to Substitute New Note for Note of Decedent: In cases where the decedent's loan pertains to a vehicle purchase, this type of agreement is employed. The heirs undertake the obligations of the original note and agree to a substitution to ensure the smooth continuation of the vehicle loan. By utilizing the Fulton Georgia Agreement By Heirs to Substitute New Note for Note of Decedent, heirs can properly assume the responsibilities of the deceased borrower. This legal document serves as a crucial protection for both the heirs and the lender, ensuring that the loan arrangement remains intact while accommodating the changing circumstances resulting from the decedent's passing.Fulton Georgia Agreement By Heirs to Substitute New Note for Note of Decedent is a legal document that allows the heirs of a deceased person to replace the existing note (loan) held by the decedent with a new note. This agreement is entered into when the decedent was a party to a loan transaction, and after their passing, the heirs wish to assume the rights and responsibilities of the original note. The purpose of the Fulton Georgia Agreement By Heirs to Substitute New Note for Note of Decedent is to provide a legal framework for the heirs to substitute the old note with a new one, ensuring the continuity of the loan without causing disruptions or default. This agreement acts as a guarantee that the new note will be treated and repaid in the same manner as the original note. The Fulton Georgia Agreement By Heirs to Substitute New Note for Note of Decedent protects the interests of all involved parties. It outlines the terms and conditions of the new note, such as the principal amount, interest rate, repayment schedule, and any other relevant provisions. The heirs assume the same obligations the decedent had, and the lender agrees to transfer the existing loan and accept the new note. Different types of Fulton Georgia Agreement By Heirs to Substitute New Note for Note of Decedent may include variations in the terms and conditions depending on the specific circumstances. Some key types may include: 1. Residential Property Agreement By Heirs to Substitute New Note for Note of Decedent: This type of agreement applies when the decedent was the borrower in a residential property loan. The heirs agree to substitute the existing note with a new note to ensure the continuation of the loan while abiding by the applicable residential property regulations. 2. Commercial Property Agreement By Heirs to Substitute New Note for Note of Decedent: If the decedent was a party to a loan related to a commercial property, this type of agreement is utilized. The heirs replace the previous note with a new one, maintaining the terms and conditions of the original loan while adapting to the specific requirements of commercial property transactions. 3. Vehicle Loan Agreement By Heirs to Substitute New Note for Note of Decedent: In cases where the decedent's loan pertains to a vehicle purchase, this type of agreement is employed. The heirs undertake the obligations of the original note and agree to a substitution to ensure the smooth continuation of the vehicle loan. By utilizing the Fulton Georgia Agreement By Heirs to Substitute New Note for Note of Decedent, heirs can properly assume the responsibilities of the deceased borrower. This legal document serves as a crucial protection for both the heirs and the lender, ensuring that the loan arrangement remains intact while accommodating the changing circumstances resulting from the decedent's passing.