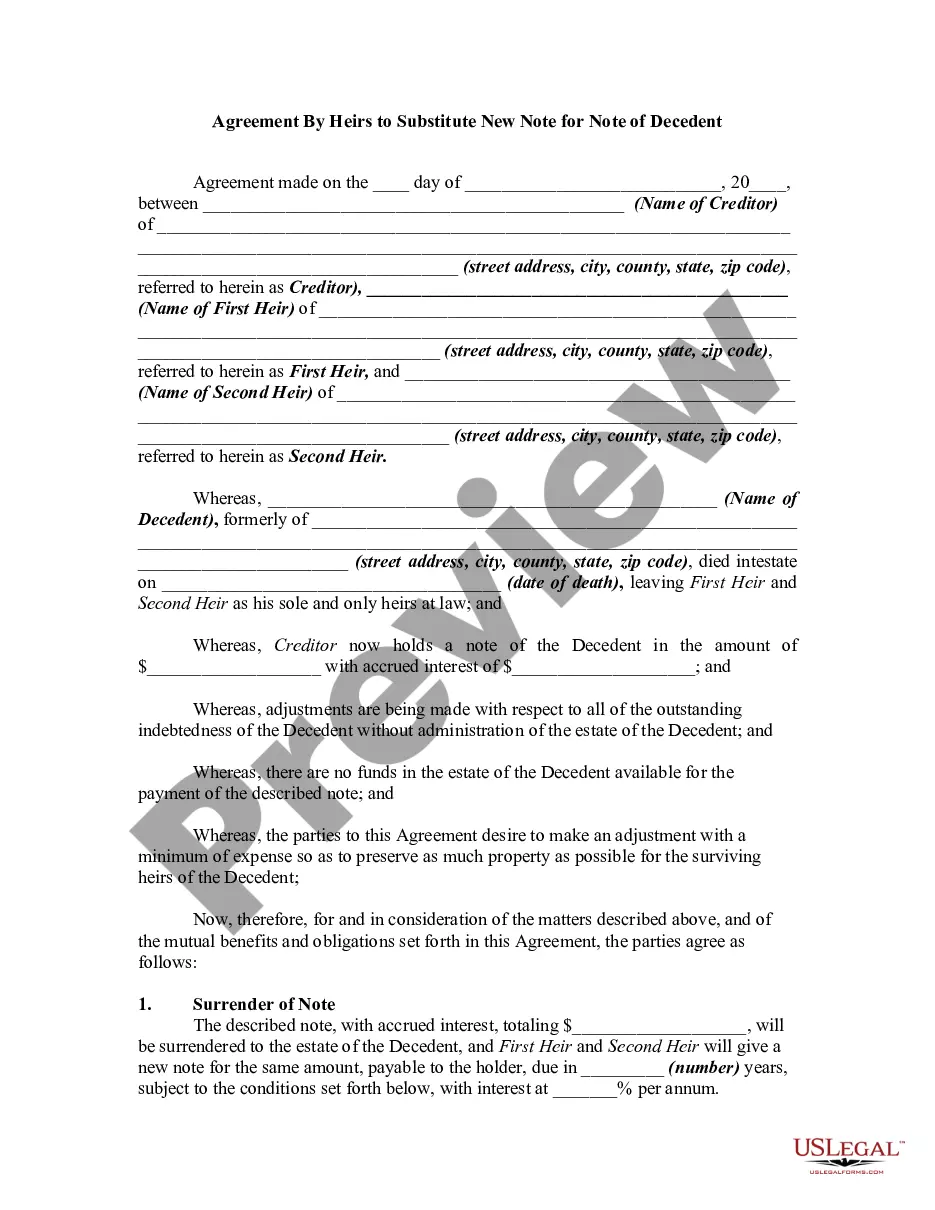

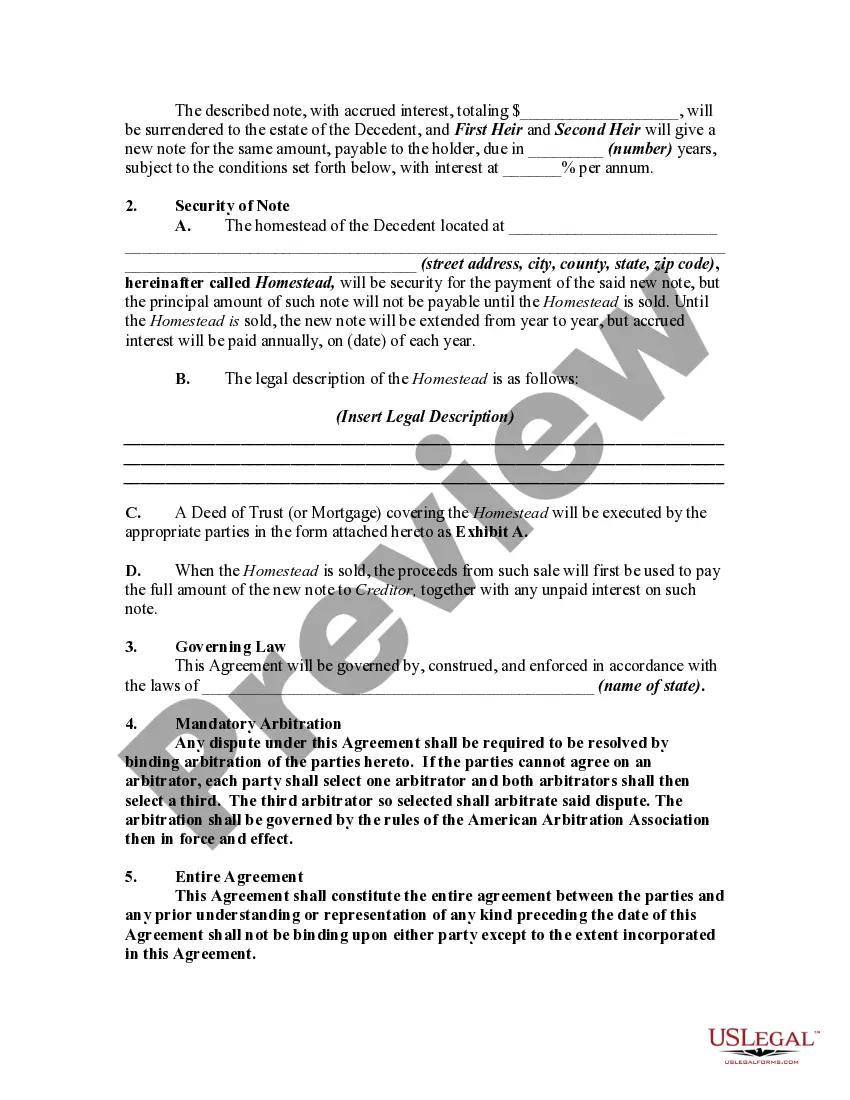

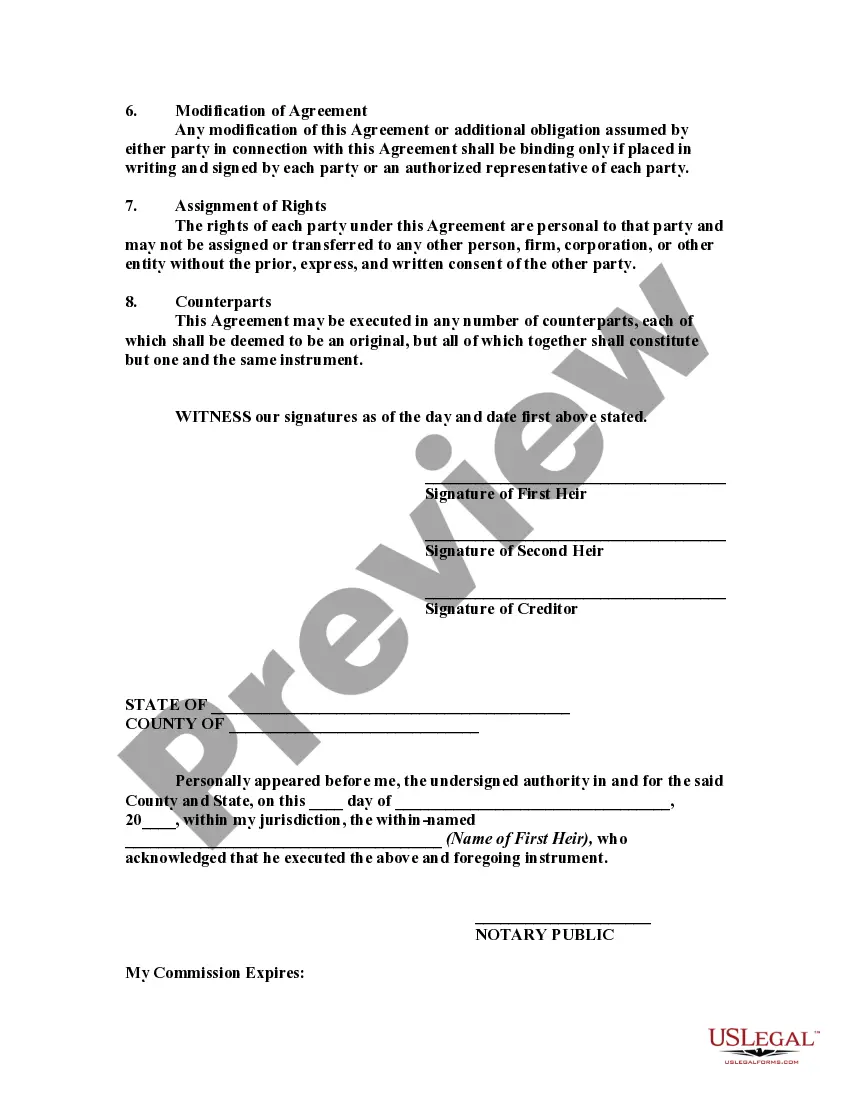

In this form, the heirs at law of an intestate estate are substituting their note for a note of the decedent. Intestate means that the decedent died without a valid will. The term heirs-at-law is used to refer to those who would inherit under the state statute of descent and distribution if the decedent dies intestate.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Title: Understanding the Harris Texas Agreement By Heirs to Substitute New Note for Note of Decedent Introduction: The Harris Texas Agreement By Heirs to Substitute New Note for Note of Decedent is an important legal agreement that allows the heirs of a deceased individual to replace a promissory note held by the decedent with a new note. This legal process often occurs after the passing of a loved one who had existing financial obligations or loans. Keywords: Harris Texas Agreement, heirs, substitute, new note, decedent, promissory note, legal agreement 1. What is the Harris Texas Agreement By Heirs to Substitute New Note for Note of Decedent? The Harris Texas Agreement By Heirs to Substitute New Note for Note of Decedent is a legal contract that provides a mechanism for the heirs of a deceased individual to replace a promissory note held by the decedent with a new note. 2. Purpose and Benefits of the Agreement: The primary purpose of the Harris Texas Agreement is to transfer the existing financial obligations of a decedent to the heirs. By substituting the original note with a new one, the agreement enables the heirs to fulfill the deceased individual's obligations while ensuring legal clarity and transparency. This agreement offers benefits such as flexibility in loan terms, uniformity in loan servicing, and consolidation of multiple notes into a single new note. 3. Key Elements of the Harris Texas Agreement: a) Identification of Parties: The agreement should identify the participating heirs and any other relevant individuals involved, such as creditors or financial institutions. b) Description of the Original Note: Detailed information about the existing promissory note, including the principal amount, interest rate, and repayment terms, should be included. c) Terms of the New Note: The agreement should outline the terms and conditions of the new promissory note, such as interest rate, repayment schedule, and any additional provisions or amendments. d) Consent and Approval: It is crucial that all parties involved, including the heirs, creditors, and any relevant authorities, provide their consent and approval for the substitution of the notes. e) Legal Acknowledgment: The agreement must be notarized or duly executed following all legal formalities to ensure its validity and enforceability. 4. Types of Harris Texas Agreement By Heirs to Substitute New Note for Note of Decedent: There are different types of Harris Texas Agreement based on the specific circumstances and parties involved. These may include: a) Agreement for Mortgage Note Substitution: Specifically related to mortgage loans. b) Agreement for Personal Loan Note Substitution: Applicable when the decedent had personal debts or loans. c) Agreement for Business Loan Note Substitution: Relevant for situations where the decedent had business-related obligations or loans. Conclusion: The Harris Texas Agreement By Heirs to Substitute New Note for Note of Decedent provides a legal framework for the heirs to take over the financial responsibilities of a deceased individual. This agreement facilitates the seamless transfer of notes and ensures transparency in honoring the decedent's financial commitments. Heirs, creditors, and financial institutions should understand the key elements of this agreement to effectively navigate the process of substituting notes and managing the estate's obligations.Title: Understanding the Harris Texas Agreement By Heirs to Substitute New Note for Note of Decedent Introduction: The Harris Texas Agreement By Heirs to Substitute New Note for Note of Decedent is an important legal agreement that allows the heirs of a deceased individual to replace a promissory note held by the decedent with a new note. This legal process often occurs after the passing of a loved one who had existing financial obligations or loans. Keywords: Harris Texas Agreement, heirs, substitute, new note, decedent, promissory note, legal agreement 1. What is the Harris Texas Agreement By Heirs to Substitute New Note for Note of Decedent? The Harris Texas Agreement By Heirs to Substitute New Note for Note of Decedent is a legal contract that provides a mechanism for the heirs of a deceased individual to replace a promissory note held by the decedent with a new note. 2. Purpose and Benefits of the Agreement: The primary purpose of the Harris Texas Agreement is to transfer the existing financial obligations of a decedent to the heirs. By substituting the original note with a new one, the agreement enables the heirs to fulfill the deceased individual's obligations while ensuring legal clarity and transparency. This agreement offers benefits such as flexibility in loan terms, uniformity in loan servicing, and consolidation of multiple notes into a single new note. 3. Key Elements of the Harris Texas Agreement: a) Identification of Parties: The agreement should identify the participating heirs and any other relevant individuals involved, such as creditors or financial institutions. b) Description of the Original Note: Detailed information about the existing promissory note, including the principal amount, interest rate, and repayment terms, should be included. c) Terms of the New Note: The agreement should outline the terms and conditions of the new promissory note, such as interest rate, repayment schedule, and any additional provisions or amendments. d) Consent and Approval: It is crucial that all parties involved, including the heirs, creditors, and any relevant authorities, provide their consent and approval for the substitution of the notes. e) Legal Acknowledgment: The agreement must be notarized or duly executed following all legal formalities to ensure its validity and enforceability. 4. Types of Harris Texas Agreement By Heirs to Substitute New Note for Note of Decedent: There are different types of Harris Texas Agreement based on the specific circumstances and parties involved. These may include: a) Agreement for Mortgage Note Substitution: Specifically related to mortgage loans. b) Agreement for Personal Loan Note Substitution: Applicable when the decedent had personal debts or loans. c) Agreement for Business Loan Note Substitution: Relevant for situations where the decedent had business-related obligations or loans. Conclusion: The Harris Texas Agreement By Heirs to Substitute New Note for Note of Decedent provides a legal framework for the heirs to take over the financial responsibilities of a deceased individual. This agreement facilitates the seamless transfer of notes and ensures transparency in honoring the decedent's financial commitments. Heirs, creditors, and financial institutions should understand the key elements of this agreement to effectively navigate the process of substituting notes and managing the estate's obligations.