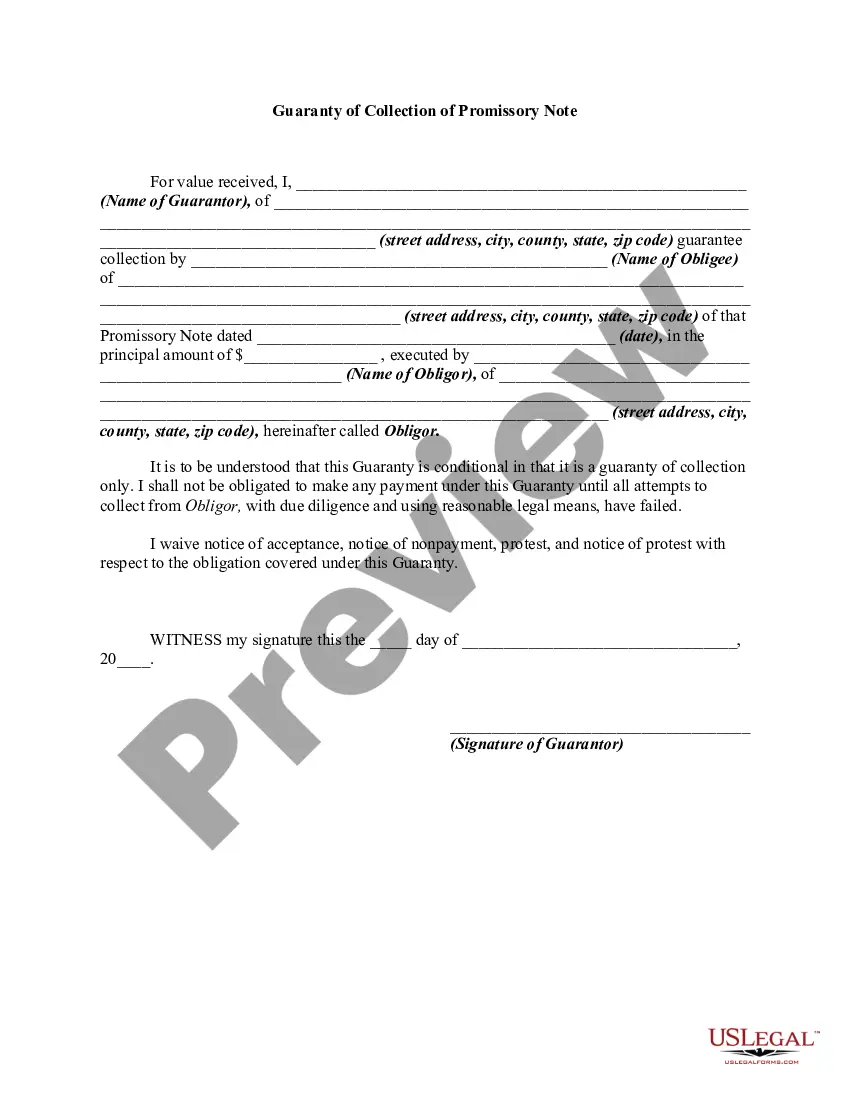

A guaranty is a contract under which one person agrees to pay a debt or perform a duty if the other person who is bound to pay the debt or perform the duty fails to do so. A guaranty of the payment of a debt is different from a guaranty of the collection of the debt. A guaranty of payment is absolute while a guaranty of collection is conditional.

The Nassau New York Guaranty of Collection of Promissory Note refers to a legal document that acts as a binding agreement between two parties in the county of Nassau, New York. It establishes the terms and conditions under which one party guarantees the collection of a promissory note on behalf of the other party. A promissory note is a written agreement in which one person (the promise) promises to pay a specific amount of money to another person (the promise) at a predetermined time. In some cases, the promise may require additional security to ensure repayment, which is where the Nassau New York Guaranty of Collection of Promissory Note comes into play. By signing the guaranty, the guarantor pledges to fulfill the promise's obligations in case the promise fails to fulfill their payment obligations outlined in the promissory note. The guarantor assumes responsibility for collecting the outstanding amount owed, making this document vital in safeguarding the promise's financial interests. The Nassau New York Guaranty of Collection of Promissory Note may vary in types depending on the specific circumstances. Here are some types that could exist: 1. Absolute Guaranty: The guarantor assumes full responsibility for the collection of the promissory note, regardless of any defenses or claims that may arise from the promise. 2. Limited Guaranty: The guarantor agrees to guarantee the collection of the promissory note up to a specified amount or for a defined period. Limits are set to protect the guarantor from excessive liability. 3. Conditional Guaranty: The guarantor's obligations are contingent on specific conditions being met. For example, the guarantor may require the promise to attempt collection from the promise before stepping in. 4. Continuing Guaranty: The guarantor's obligations extend beyond a single promissory note. It covers all present and future promissory notes or debts between the promise and promise, providing ongoing security. 5. Demand Guaranty: The guarantor's obligations come into effect upon demand from the promise. Unlike fixed-duration guaranties, this type is flexible and can be accessed if needed by the promise. The Nassau New York Guaranty of Collection of Promissory Note is crucial in protecting lenders or parties lending money by providing an additional layer of security. It offers peace of mind to the promise, knowing that a guarantor will step in if the promise cannot fulfill their obligations.The Nassau New York Guaranty of Collection of Promissory Note refers to a legal document that acts as a binding agreement between two parties in the county of Nassau, New York. It establishes the terms and conditions under which one party guarantees the collection of a promissory note on behalf of the other party. A promissory note is a written agreement in which one person (the promise) promises to pay a specific amount of money to another person (the promise) at a predetermined time. In some cases, the promise may require additional security to ensure repayment, which is where the Nassau New York Guaranty of Collection of Promissory Note comes into play. By signing the guaranty, the guarantor pledges to fulfill the promise's obligations in case the promise fails to fulfill their payment obligations outlined in the promissory note. The guarantor assumes responsibility for collecting the outstanding amount owed, making this document vital in safeguarding the promise's financial interests. The Nassau New York Guaranty of Collection of Promissory Note may vary in types depending on the specific circumstances. Here are some types that could exist: 1. Absolute Guaranty: The guarantor assumes full responsibility for the collection of the promissory note, regardless of any defenses or claims that may arise from the promise. 2. Limited Guaranty: The guarantor agrees to guarantee the collection of the promissory note up to a specified amount or for a defined period. Limits are set to protect the guarantor from excessive liability. 3. Conditional Guaranty: The guarantor's obligations are contingent on specific conditions being met. For example, the guarantor may require the promise to attempt collection from the promise before stepping in. 4. Continuing Guaranty: The guarantor's obligations extend beyond a single promissory note. It covers all present and future promissory notes or debts between the promise and promise, providing ongoing security. 5. Demand Guaranty: The guarantor's obligations come into effect upon demand from the promise. Unlike fixed-duration guaranties, this type is flexible and can be accessed if needed by the promise. The Nassau New York Guaranty of Collection of Promissory Note is crucial in protecting lenders or parties lending money by providing an additional layer of security. It offers peace of mind to the promise, knowing that a guarantor will step in if the promise cannot fulfill their obligations.