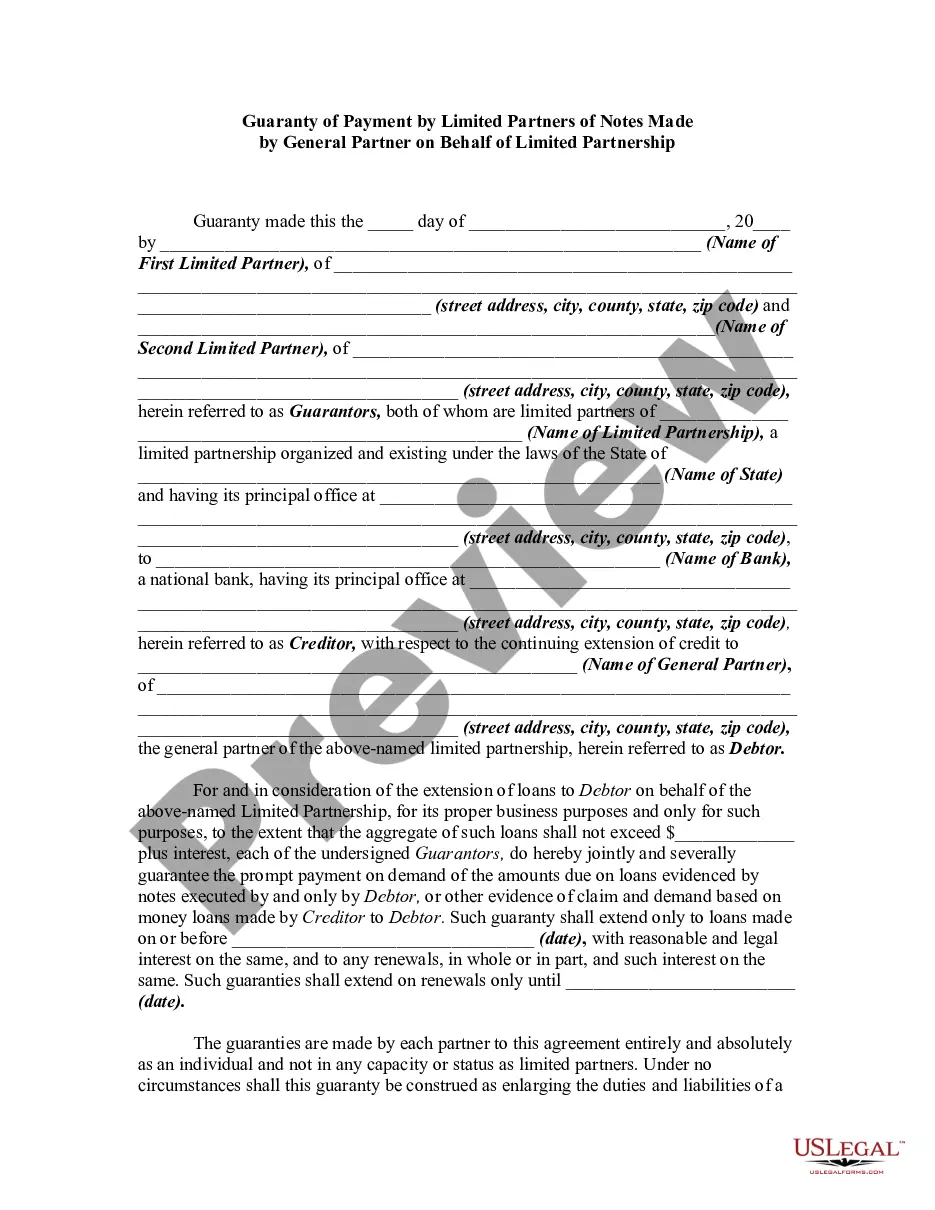

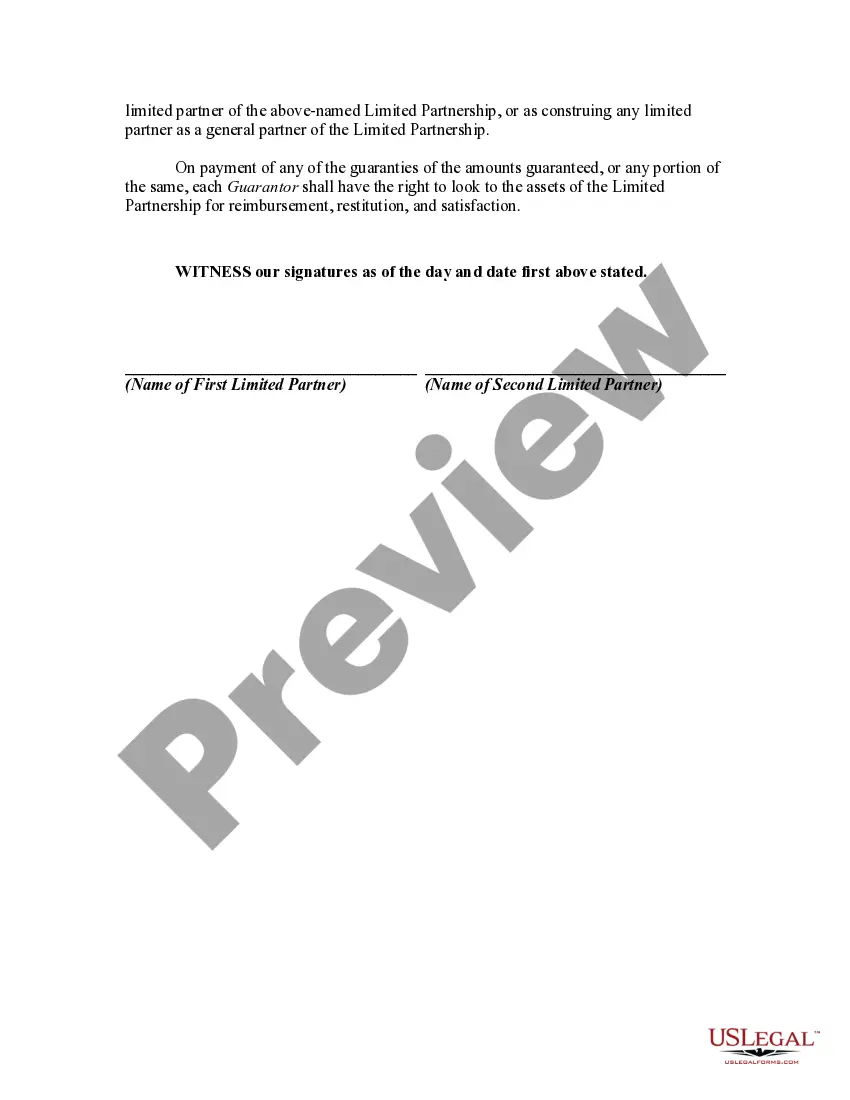

A limited partnership is a modified partnership. It has characteristics of both a corporation and a general partnership. In a limited partnership, certain members contribute capital, but do not have liability for the debts of the partnership beyond the amount of their investment. These members are known as limited partners. The partners who manage the business and who are personally liable for the debts of the business are the general partners. Limited partners have the right to share in the profits of the business and, if the partnership is dissolved, will be entitled to a percentage of the assets of the partnership. A limited partner may lose his limited liability status if he participates in the control of the business.

Collin Texas Guaranty of Payment by Limited Partners of Notes Made by General Partner on Behalf of Limited Partnership

Category:

State:

Multi-State

County:

Collin

Control #:

US-01115BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Collin Texas Guaranty Of Payment By Limited Partners Of Notes Made By General Partner On Behalf Of Limited Partnership?

Do you need to quickly draft a legally-binding Collin Guaranty of Payment by Limited Partners of Notes Made by General Partner on Behalf of Limited Partnership or maybe any other form to handle your own or corporate affairs? You can select one of the two options: contact a legal advisor to write a valid paper for you or draft it entirely on your own. Luckily, there's an alternative option - US Legal Forms. It will help you get neatly written legal paperwork without having to pay sky-high fees for legal services.

US Legal Forms provides a huge catalog of more than 85,000 state-specific form templates, including Collin Guaranty of Payment by Limited Partners of Notes Made by General Partner on Behalf of Limited Partnership and form packages. We provide documents for a myriad of use cases: from divorce papers to real estate documents. We've been out there for over 25 years and gained a spotless reputation among our clients. Here's how you can become one of them and obtain the needed template without extra troubles.

- First and foremost, double-check if the Collin Guaranty of Payment by Limited Partners of Notes Made by General Partner on Behalf of Limited Partnership is tailored to your state's or county's laws.

- If the document includes a desciption, make sure to check what it's intended for.

- Start the searching process again if the form isn’t what you were looking for by utilizing the search bar in the header.

- Select the plan that is best suited for your needs and proceed to the payment.

- Select the file format you would like to get your document in and download it.

- Print it out, fill it out, and sign on the dotted line.

If you've already set up an account, you can easily log in to it, find the Collin Guaranty of Payment by Limited Partners of Notes Made by General Partner on Behalf of Limited Partnership template, and download it. To re-download the form, simply go to the My Forms tab.

It's stressless to find and download legal forms if you use our catalog. Moreover, the documents we provide are updated by industry experts, which gives you greater peace of mind when dealing with legal matters. Try US Legal Forms now and see for yourself!