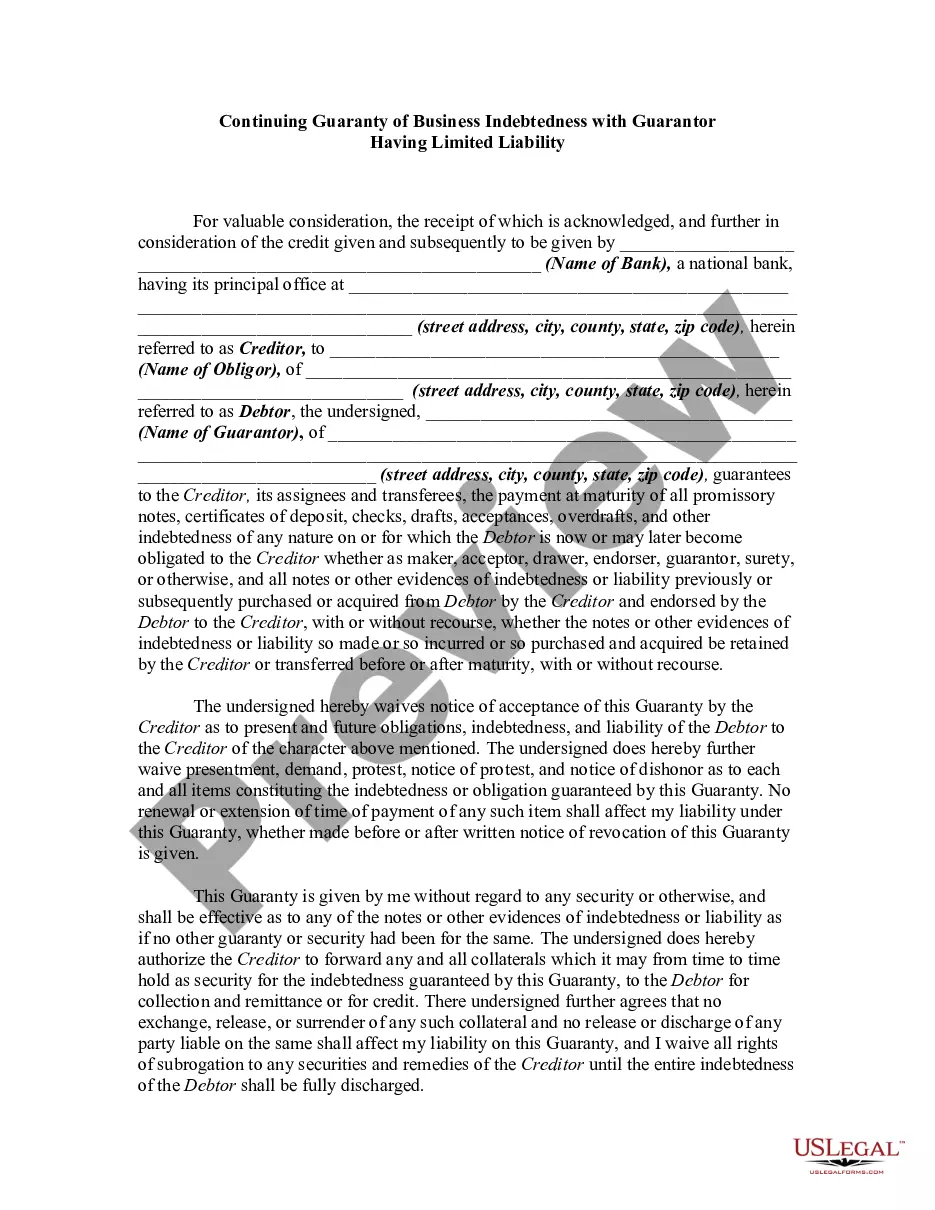

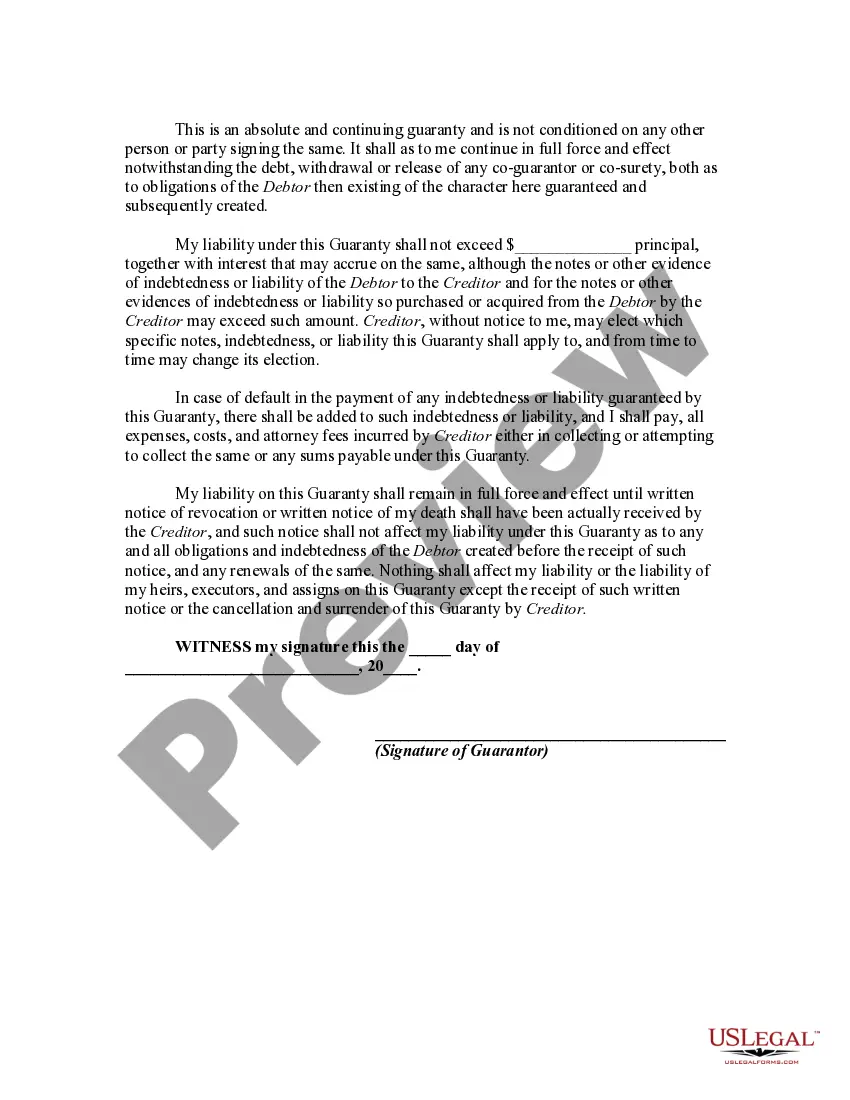

A guaranty is an undertaking on the part of one person (the guarantor) that is collateral to an obligation of another person (the debtor or obligor), and which binds the guarantor to performance of the obligation in the event of default by the debtor or obligor. A guaranty agreement is a type of contract. Thus, questions relating to such matters as validity, interpretation, and enforceability of guaranty agreements are decided in accordance with basic principles of contract law.

The King Washington Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability is a legal document designed to establish an agreement between a creditor and a guarantor with limited liability. This agreement ensures that the guarantor is responsible for any debts or liabilities incurred by the business. This type of guaranty is commonly used in business transactions where a borrowing entity, such as a corporation or limited liability company (LLC), seeks financial assistance from a lender. The lender may require additional security to mitigate the risk of default, and hence, they request a guarantor with limited liability to guarantee the repayment of the loan. The King Washington Continuing Guaranty of Business Indebtedness provides the lender with an added layer of protection by holding the guarantor accountable for the business's debts and obligations. It signifies that, in case of non-payment, the lender has the right to pursue the guarantor for repayment. There can be several variations or types of King Washington Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability documents, depending on the specific conditions and requirements of the lending agreement. Some key variations and scenarios that may arise include: 1. Limited Liability Company (LLC) Guaranty: This type of guaranty is designed specifically for businesses operating as LCS. It outlines the responsibilities and limitations of the guarantor in relation to the LLC's indebtedness. 2. Corporate Guaranty: For businesses structured as corporations, a corporate guaranty may be used. This document establishes the obligations and liabilities of the guarantor, who could be an individual or another corporate entity, towards the lender. 3. Continuing Guaranty: This type of guaranty extends beyond a single transaction and covers future indebtedness as well. It ensures that the guarantor's obligations remain in effect until explicitly released or discharged. 4. Specific Indebtedness Guaranty: In certain cases, a guarantor may provide a guaranty for a specific debt or obligation rather than the entire indebtedness of the business. This type of guaranty is limited to a particular loan or transaction. 5. Cross-Collateralization Guaranty: In complex financial arrangements, a guarantor may offer collateral, such as real estate or other assets, to secure the overall indebtedness of the business. This type of guaranty ensures the lender has multiple sources of repayment. Overall, the King Washington Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability helps protect the interests of lenders by establishing a legal agreement that holds a guarantor accountable for a business's debts. It is critical for both parties involved to fully understand the terms, conditions, and limitations outlined in the specific guaranty agreement.The King Washington Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability is a legal document designed to establish an agreement between a creditor and a guarantor with limited liability. This agreement ensures that the guarantor is responsible for any debts or liabilities incurred by the business. This type of guaranty is commonly used in business transactions where a borrowing entity, such as a corporation or limited liability company (LLC), seeks financial assistance from a lender. The lender may require additional security to mitigate the risk of default, and hence, they request a guarantor with limited liability to guarantee the repayment of the loan. The King Washington Continuing Guaranty of Business Indebtedness provides the lender with an added layer of protection by holding the guarantor accountable for the business's debts and obligations. It signifies that, in case of non-payment, the lender has the right to pursue the guarantor for repayment. There can be several variations or types of King Washington Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability documents, depending on the specific conditions and requirements of the lending agreement. Some key variations and scenarios that may arise include: 1. Limited Liability Company (LLC) Guaranty: This type of guaranty is designed specifically for businesses operating as LCS. It outlines the responsibilities and limitations of the guarantor in relation to the LLC's indebtedness. 2. Corporate Guaranty: For businesses structured as corporations, a corporate guaranty may be used. This document establishes the obligations and liabilities of the guarantor, who could be an individual or another corporate entity, towards the lender. 3. Continuing Guaranty: This type of guaranty extends beyond a single transaction and covers future indebtedness as well. It ensures that the guarantor's obligations remain in effect until explicitly released or discharged. 4. Specific Indebtedness Guaranty: In certain cases, a guarantor may provide a guaranty for a specific debt or obligation rather than the entire indebtedness of the business. This type of guaranty is limited to a particular loan or transaction. 5. Cross-Collateralization Guaranty: In complex financial arrangements, a guarantor may offer collateral, such as real estate or other assets, to secure the overall indebtedness of the business. This type of guaranty ensures the lender has multiple sources of repayment. Overall, the King Washington Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability helps protect the interests of lenders by establishing a legal agreement that holds a guarantor accountable for a business's debts. It is critical for both parties involved to fully understand the terms, conditions, and limitations outlined in the specific guaranty agreement.