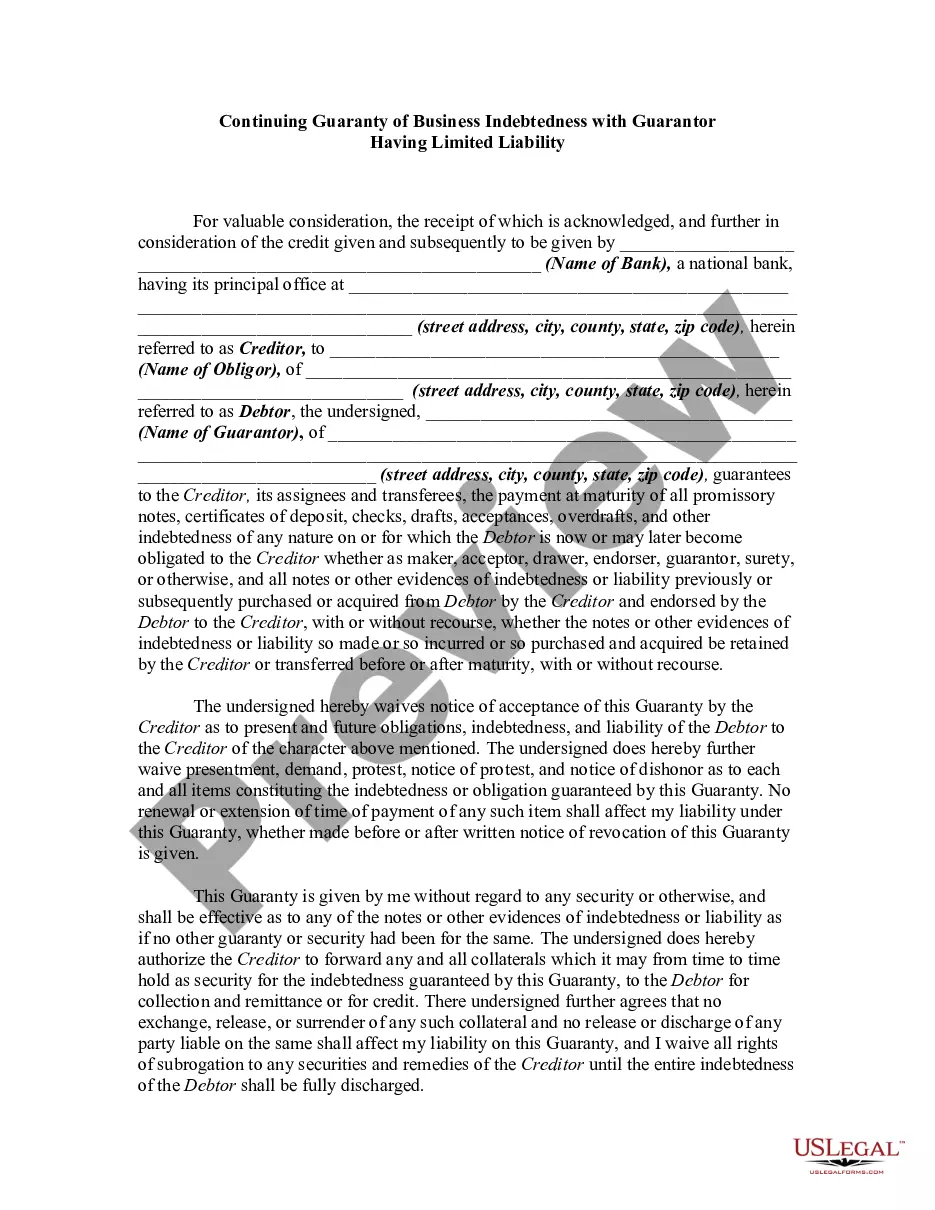

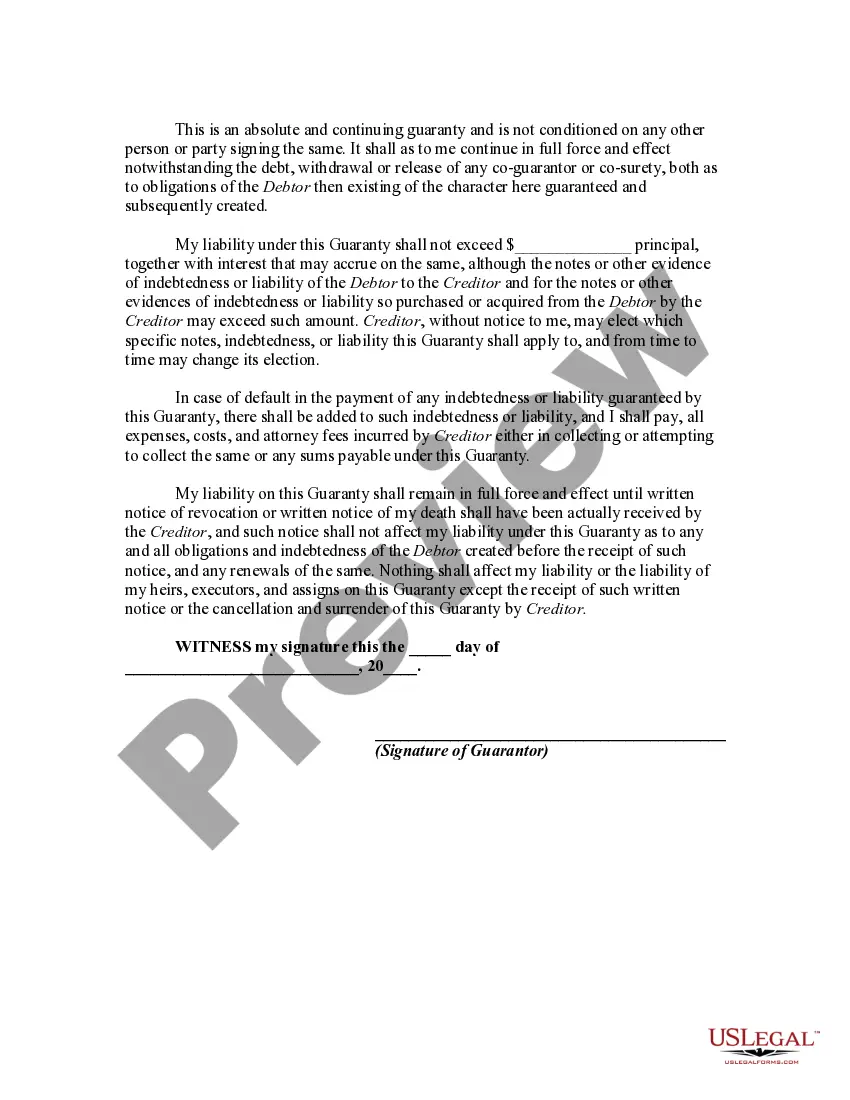

A guaranty is an undertaking on the part of one person (the guarantor) that is collateral to an obligation of another person (the debtor or obligor), and which binds the guarantor to performance of the obligation in the event of default by the debtor or obligor. A guaranty agreement is a type of contract. Thus, questions relating to such matters as validity, interpretation, and enforceability of guaranty agreements are decided in accordance with basic principles of contract law.

Mecklenburg North Carolina Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability A Mecklenburg North Carolina Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability is a legally binding agreement that provides a mechanism for ensuring the repayment of a business's debts. This type of guarantee is commonly used in commercial transactions where the lender requires additional assurance for the borrowed funds. Keywords: Mecklenburg North Carolina, Continuing Guaranty, Business Indebtedness, Guarantor, Limited Liability, Commercial transactions, Repayment, Lender, Borrowed funds. This type of guaranty serves as a risk management tool, minimizing potential financial losses for lenders. By having a guarantor with limited liability, they can be held responsible only up to a certain extent, thereby reducing their exposure to the business's obligations. There are different types or variations of the Mecklenburg North Carolina Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability, namely: 1. Limited Liability Guaranty: This type of guaranty limits the guarantor's liability to a specific amount or a predefined percentage of the total business indebtedness. The guarantor will be liable only for this predetermined limit, protecting them from unforeseen or excessive liabilities. 2. Time-Limited Guaranty: In this variation, the guarantor's liability is limited to a particular timeframe. Once the agreed-upon duration expires, the guarantor is released from any further obligations, even if the business remains indebted. 3. Asset-Based Guaranty: This form of guaranty provides limited liability for the guarantor based on the valuation of specific assets. The amount of liability is linked to the value of the pledged assets, ensuring that the guarantor's exposure is proportionate to the asset's worth. 4. Partial Guaranty: This version of the guaranty agreement applies only to a portion of the business's overall indebtedness. The guarantor assumes limited liability for a specific part of the debt, leaving the remainder unaffected. It's crucial for all parties involved to thoroughly review and understand the terms and conditions of the Mecklenburg North Carolina Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability before entering into such an agreement. Seeking legal advice is highly recommended ensuring compliance with applicable laws and to protect each party's rights and interests. In conclusion, a Mecklenburg North Carolina Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability provides a means for lenders to secure repayment of business debts while affording the guarantor certain limitations on their liability. Understanding the different types of this guaranty allows businesses and guarantors to select the most appropriate approach that suits their needs and circumstances.Mecklenburg North Carolina Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability A Mecklenburg North Carolina Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability is a legally binding agreement that provides a mechanism for ensuring the repayment of a business's debts. This type of guarantee is commonly used in commercial transactions where the lender requires additional assurance for the borrowed funds. Keywords: Mecklenburg North Carolina, Continuing Guaranty, Business Indebtedness, Guarantor, Limited Liability, Commercial transactions, Repayment, Lender, Borrowed funds. This type of guaranty serves as a risk management tool, minimizing potential financial losses for lenders. By having a guarantor with limited liability, they can be held responsible only up to a certain extent, thereby reducing their exposure to the business's obligations. There are different types or variations of the Mecklenburg North Carolina Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability, namely: 1. Limited Liability Guaranty: This type of guaranty limits the guarantor's liability to a specific amount or a predefined percentage of the total business indebtedness. The guarantor will be liable only for this predetermined limit, protecting them from unforeseen or excessive liabilities. 2. Time-Limited Guaranty: In this variation, the guarantor's liability is limited to a particular timeframe. Once the agreed-upon duration expires, the guarantor is released from any further obligations, even if the business remains indebted. 3. Asset-Based Guaranty: This form of guaranty provides limited liability for the guarantor based on the valuation of specific assets. The amount of liability is linked to the value of the pledged assets, ensuring that the guarantor's exposure is proportionate to the asset's worth. 4. Partial Guaranty: This version of the guaranty agreement applies only to a portion of the business's overall indebtedness. The guarantor assumes limited liability for a specific part of the debt, leaving the remainder unaffected. It's crucial for all parties involved to thoroughly review and understand the terms and conditions of the Mecklenburg North Carolina Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability before entering into such an agreement. Seeking legal advice is highly recommended ensuring compliance with applicable laws and to protect each party's rights and interests. In conclusion, a Mecklenburg North Carolina Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability provides a means for lenders to secure repayment of business debts while affording the guarantor certain limitations on their liability. Understanding the different types of this guaranty allows businesses and guarantors to select the most appropriate approach that suits their needs and circumstances.