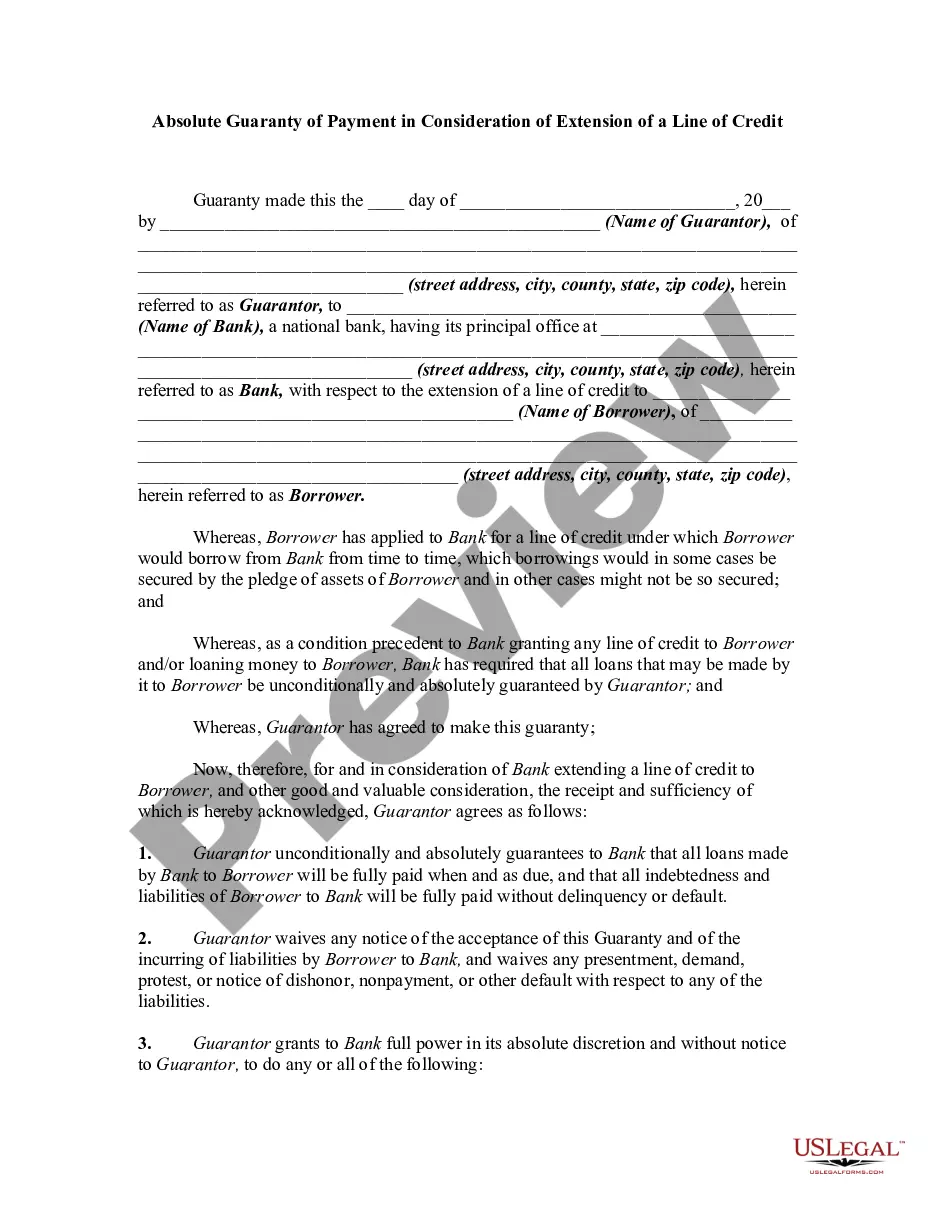

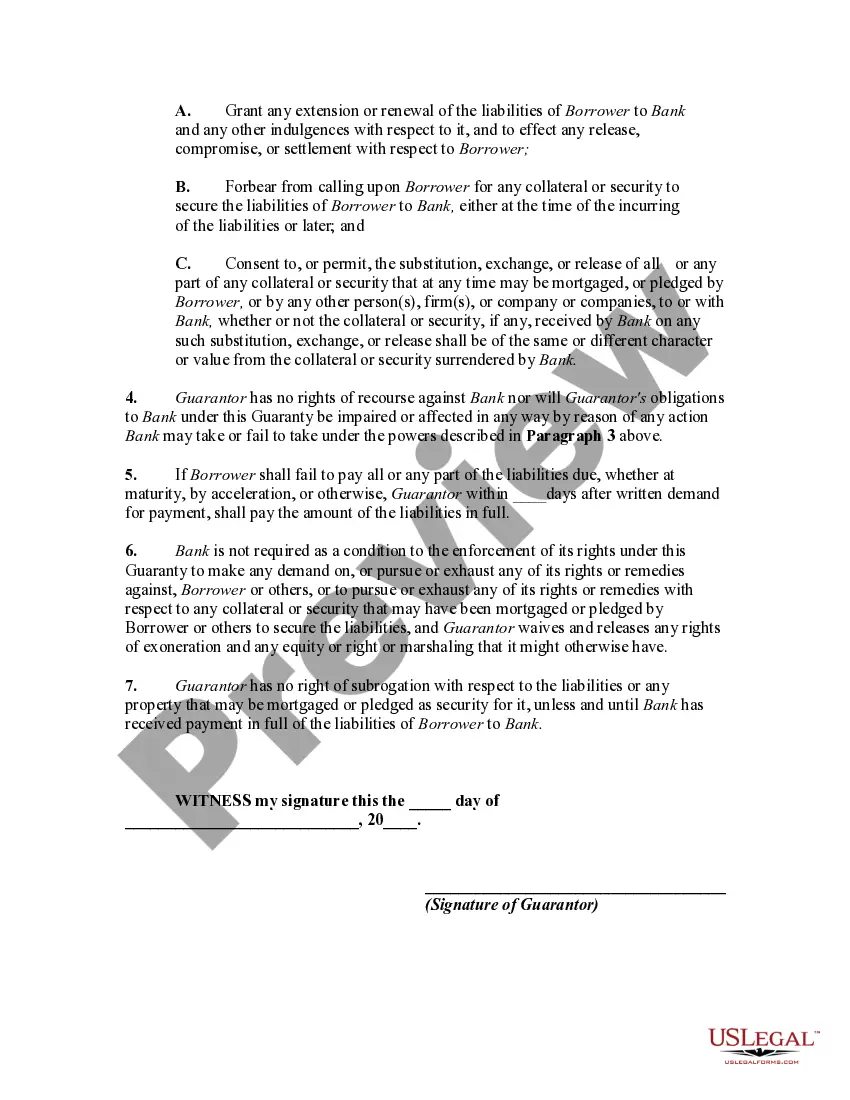

A guaranty is an undertaking on the part of one person (the guarantor) that is collateral to an obligation of another person (the debtor or obligor), and which binds the guarantor to performance of the obligation in the event of default by the debtor or obligor.

The contract of guaranty may be absolute or it may be conditional. An absolute guaranty is a contract by which the guarantor has promised that if the debtor does not perform the obligation or obligations, the guarantor will perform some act (such as the payment of money) to or for the benefit of the creditor.

A line of credit is an arrangement in which a lender extends a specified amount of credit to borrower for a specified time period.

Mecklenburg North Carolina Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit is a legal document that provides a comprehensive guarantee of payment to a lender for the extension of a line of credit in Mecklenburg, North Carolina. This type of guaranty is typically used in commercial transactions where a borrower requires access to additional funds beyond their existing credit limit. Keywords: Mecklenburg North Carolina, Absolute Guaranty of Payment, Extension of a Line of Credit, legal document, comprehensive guarantee, lender, borrower, commercial transactions, funds, credit limit. Types of Mecklenburg North Carolina Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit: 1. Personal Guaranty: This type of guaranty involves an individual, typically the owner or principal of a business, providing a personal guarantee of payment for the extension of a line of credit. It holds the guarantor personally liable for the debt in case of default by the borrower. 2. Corporate Guaranty: In this case, a corporation guarantees payment for the extension of a line of credit. The guaranty is provided by the corporation itself, making the company liable for the debt if the borrower fails to repay. 3. Limited Guaranty: A limited guaranty places specific limitations on the extent of the guarantor's liability. This means that the guarantor is only responsible for a portion of the debt, up to a predetermined amount or under specific conditions outlined in the agreement. 4. Unconditional Guaranty: An unconditional guaranty is a type of guaranty where the guarantor's liability is not subject to any conditions or limitations. They are fully responsible for payment in case of default, regardless of the circumstances. 5. Continuing Guaranty: A continuing guaranty is a guaranty that remains in effect for an extended period, usually until the borrower's line of credit is completely paid off or terminated. It covers all future extensions of credit made within the specified timeframe. 6. Limited Liability Guaranty: In some cases, a guarantor may seek to limit their liability by including specific clauses in the guaranty agreement. This type of guaranty protects the guarantor from excessive liability and clearly defines their payment obligations. It is important to consult legal professionals when drafting or entering into a Mecklenburg North Carolina Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit. Each type of guaranty may vary in terms of its scope, obligations, and legal implications, and it is crucial to fully understand these aspects before agreeing to or providing a guaranty.Mecklenburg North Carolina Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit is a legal document that provides a comprehensive guarantee of payment to a lender for the extension of a line of credit in Mecklenburg, North Carolina. This type of guaranty is typically used in commercial transactions where a borrower requires access to additional funds beyond their existing credit limit. Keywords: Mecklenburg North Carolina, Absolute Guaranty of Payment, Extension of a Line of Credit, legal document, comprehensive guarantee, lender, borrower, commercial transactions, funds, credit limit. Types of Mecklenburg North Carolina Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit: 1. Personal Guaranty: This type of guaranty involves an individual, typically the owner or principal of a business, providing a personal guarantee of payment for the extension of a line of credit. It holds the guarantor personally liable for the debt in case of default by the borrower. 2. Corporate Guaranty: In this case, a corporation guarantees payment for the extension of a line of credit. The guaranty is provided by the corporation itself, making the company liable for the debt if the borrower fails to repay. 3. Limited Guaranty: A limited guaranty places specific limitations on the extent of the guarantor's liability. This means that the guarantor is only responsible for a portion of the debt, up to a predetermined amount or under specific conditions outlined in the agreement. 4. Unconditional Guaranty: An unconditional guaranty is a type of guaranty where the guarantor's liability is not subject to any conditions or limitations. They are fully responsible for payment in case of default, regardless of the circumstances. 5. Continuing Guaranty: A continuing guaranty is a guaranty that remains in effect for an extended period, usually until the borrower's line of credit is completely paid off or terminated. It covers all future extensions of credit made within the specified timeframe. 6. Limited Liability Guaranty: In some cases, a guarantor may seek to limit their liability by including specific clauses in the guaranty agreement. This type of guaranty protects the guarantor from excessive liability and clearly defines their payment obligations. It is important to consult legal professionals when drafting or entering into a Mecklenburg North Carolina Absolute Guaranty of Payment in Consideration of Extension of a Line of Credit. Each type of guaranty may vary in terms of its scope, obligations, and legal implications, and it is crucial to fully understand these aspects before agreeing to or providing a guaranty.