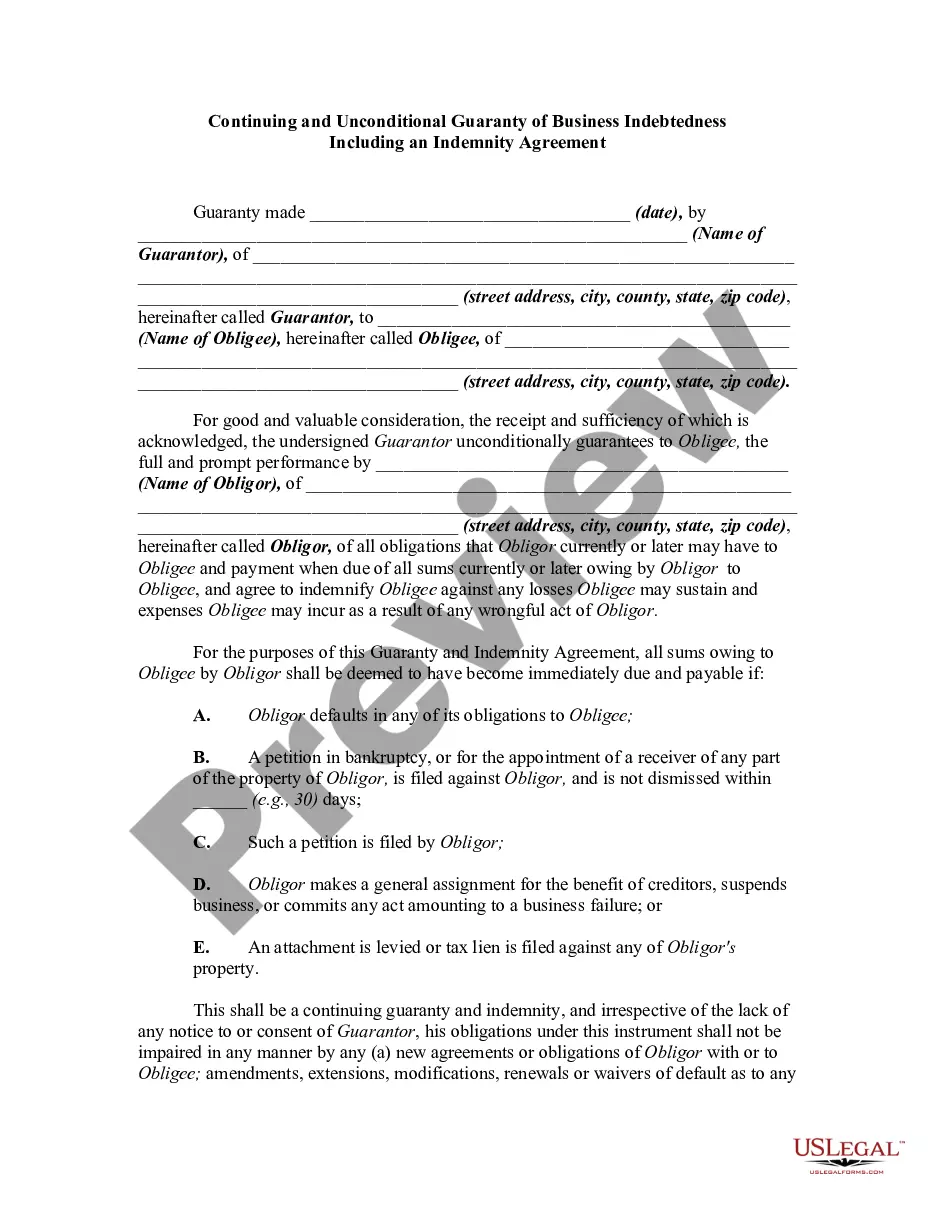

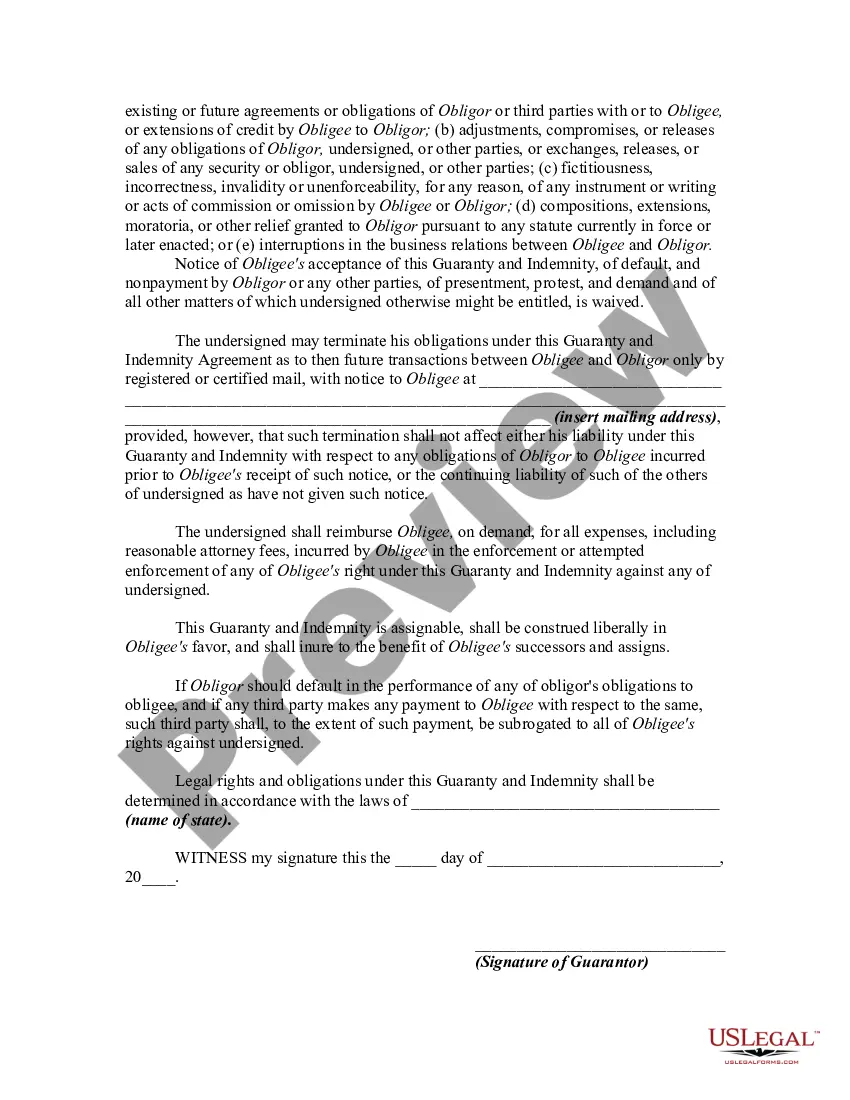

A guaranty is an undertaking on the part of one person (the guarantor) which binds the guarantor to performing the obligation of the debtor or obligor in the event of default by the debtor or obligor. The contract of guaranty may be absolute or it may be conditional. An absolute or unconditional guaranty is a contract by which the guarantor has promised that if the debtor does not perform the obligation or obligations, the guarantor will perform some act (such as the payment of money) to or for the benefit of the creditor.

A guaranty may be either continuing or restricted. The contract is restricted if it is limited to the guaranty of a single transaction or to a limited number of specific transactions and is not effective as to transactions other than those guaranteed. The contract is continuing if it contemplates a future course of dealing during an indefinite period, or if it is intended to cover a series of transactions or a succession of credits, or if its purpose is to give to the principal debtor a standing credit to be used by him or her from time to time.

A Fulton Georgia Continuing and Unconditional Guaranty of Business Indebtedness, including an Indemnity Agreement, is a legal document that outlines the specific terms and conditions under which an individual or entity agrees to assume full responsibility for the repayment of a business's debts. This type of guaranty provides a lender with an added layer of assurance that if the borrower defaults on the loan or fails to meet their obligations, the guarantor will step in and fulfill the repayment obligations. It serves as a form of financial security for the lender, minimizing the risk involved in extending credit to a business. Different variations of Fulton Georgia Continuing and Unconditional Guaranty of Business Indebtedness including an Indemnity Agreement may include: 1. Limited Guaranty: In this type of guaranty, the guarantor's liability is limited to a specific dollar amount or to a certain portion of the total indebtedness. This provides some protection to the guarantor, as their liability is not unlimited. 2. Unlimited Guaranty: Unlike the limited guaranty, an unlimited guaranty holds the guarantor fully responsible for the entire indebtedness. In case of default, the lender can pursue the guarantor for the full repayment amount, regardless of the original borrower's assets or ability to repay. 3. Continuing Guaranty: A continuing guaranty is one that remains in effect until expressly revoked or the indebtedness is fully satisfied. Even if the principal debt is paid down, this type of guaranty may continue to apply to any future borrowings or extensions of credit by the borrower. 4. Unconditional Guaranty: An unconditional guaranty is one that is not subject to any specific conditions or contingencies. It represents an absolute and irrevocable promise by the guarantor to satisfy the indebtedness, regardless of any dispute, change in circumstances, or the financial condition of the borrower. The Indemnity Agreement component within this guarantee further reinforces the guarantor's commitment by providing additional protection to the lender. It assures the lender that if any losses, damages, or costs are incurred as a result of the borrower's default, the guarantor will indemnify the lender and cover these expenses. Overall, a Fulton Georgia Continuing and Unconditional Guaranty of Business Indebtedness Including an Indemnity Agreement is a critical legal instrument that outlines the responsibilities and obligations of a guarantor in relation to a business's debts. It allows lenders to mitigate risk and ensure they have a reliable source for repayment, safeguarding their financial interests.