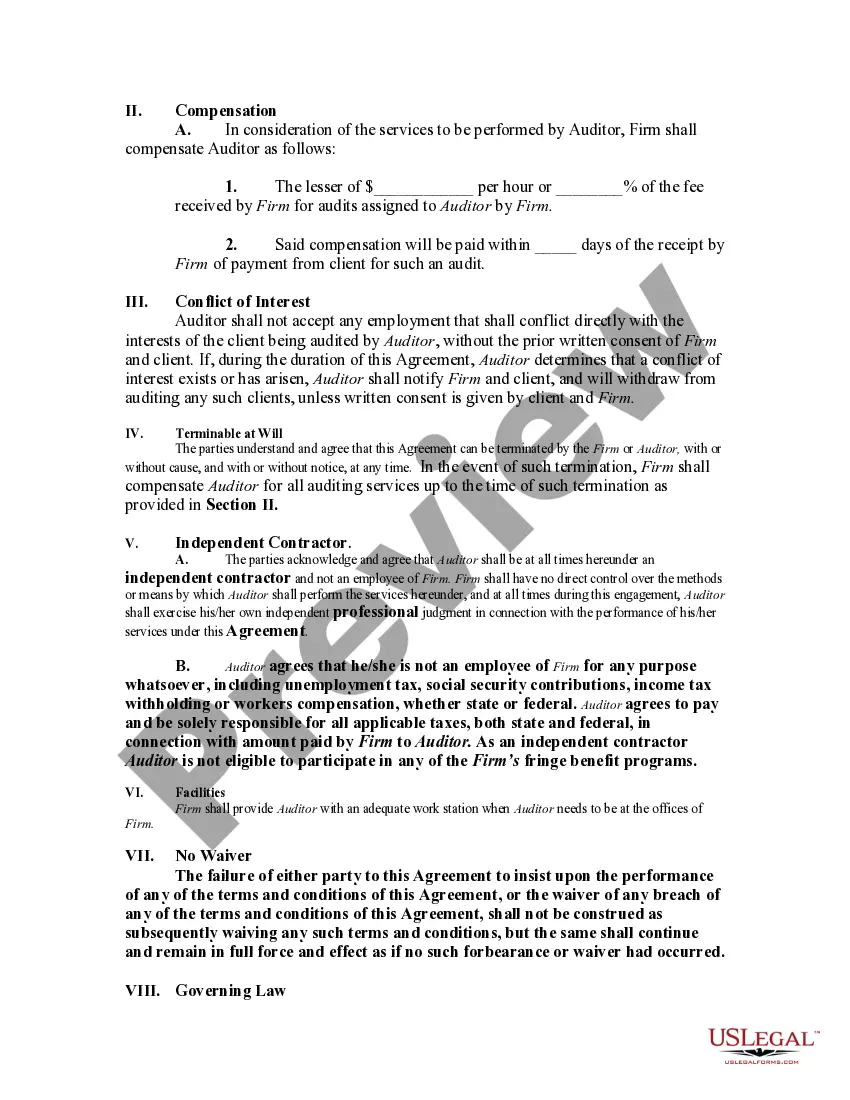

Although no definite rule exists for determining whether one is an independent contractor or an employee, certain indicia of the status of an independent contractor are recognized, and the insertion of provisions embodying these indicia in the contract will help to insure that the relationship reflects the intention of the parties. These indicia generally relate to the basic issue of control. The general test of what constitutes an independent contractor relationship involves which party has the right to direct what is to be done, and how and when. Another important test involves the method of payment of the contractor.

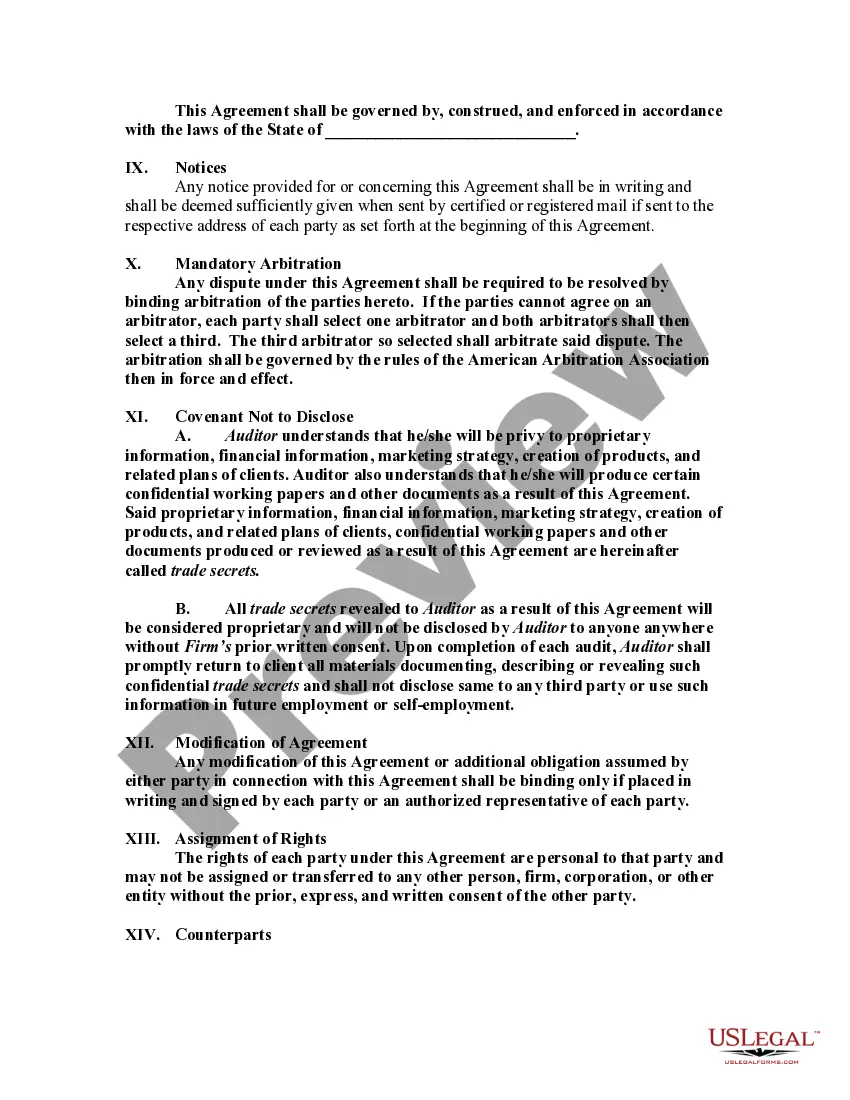

The Bronx New York Agreement by an Accounting Firm to Employ an Auditor as a Self-Employed Independent Contractor is a legally binding document that outlines the terms and conditions of engagement between an accounting firm in the Bronx, New York, and an auditor who will be hired as a self-employed independent contractor. This agreement is designed to establish a professional relationship between the accounting firm and the auditor, while clearly defining the rights, responsibilities, and obligations of both parties involved. The document covers various aspects, including but not limited to the scope of work, compensation, confidentiality, and termination procedures. The primary purpose of this agreement is to outline the specific tasks and duties the auditor will undertake on behalf of the accounting firm. It clarifies that the auditor will operate as a self-employed independent contractor, meaning that they are not an employee but rather a separate business entity. This distinction is crucial as it dictates the obligations and rights of each party under the law. Additionally, the agreement will specify the compensation structure for the auditor's services, whether it be a fixed fee, hourly rate, or commission-based arrangement. It will also address any expenses that the accounting firm will reimburse as part of the contract. Confidentiality is another important aspect covered in this agreement. Both the accounting firm and the auditor will agree to maintain strict confidentiality regarding any sensitive information obtained during the course of their professional engagement. This provision helps safeguard the firm's proprietary data and client information, ensuring that it remains secure and protected against unauthorized disclosure. Lastly, the agreement will outline the circumstances under which the engagement may be terminated by either party, as well as the notice period required for termination. This provision ensures that both parties have a fair and equitable means to end the agreement if necessary, enabling a smooth transition for both the accounting firm and the auditor. It is worth noting that while the Bronx New York Agreement by an Accounting Firm to Employ an Auditor as a Self-Employed Independent Contractor generally follows a standard structure, there may be variations or additional clauses based on the specific needs and requirements of the accounting firm and the auditor. These variations could include provisions related to intellectual property rights, dispute resolution mechanisms, non-compete agreements, and non-solicitation clauses. By utilizing the Bronx New York Agreement by an Accounting Firm to Employ an Auditor as a Self-Employed Independent Contractor, both the accounting firm and the auditor can establish a clear understanding of their professional relationship, thereby minimizing potential misunderstandings and conflicts.The Bronx New York Agreement by an Accounting Firm to Employ an Auditor as a Self-Employed Independent Contractor is a legally binding document that outlines the terms and conditions of engagement between an accounting firm in the Bronx, New York, and an auditor who will be hired as a self-employed independent contractor. This agreement is designed to establish a professional relationship between the accounting firm and the auditor, while clearly defining the rights, responsibilities, and obligations of both parties involved. The document covers various aspects, including but not limited to the scope of work, compensation, confidentiality, and termination procedures. The primary purpose of this agreement is to outline the specific tasks and duties the auditor will undertake on behalf of the accounting firm. It clarifies that the auditor will operate as a self-employed independent contractor, meaning that they are not an employee but rather a separate business entity. This distinction is crucial as it dictates the obligations and rights of each party under the law. Additionally, the agreement will specify the compensation structure for the auditor's services, whether it be a fixed fee, hourly rate, or commission-based arrangement. It will also address any expenses that the accounting firm will reimburse as part of the contract. Confidentiality is another important aspect covered in this agreement. Both the accounting firm and the auditor will agree to maintain strict confidentiality regarding any sensitive information obtained during the course of their professional engagement. This provision helps safeguard the firm's proprietary data and client information, ensuring that it remains secure and protected against unauthorized disclosure. Lastly, the agreement will outline the circumstances under which the engagement may be terminated by either party, as well as the notice period required for termination. This provision ensures that both parties have a fair and equitable means to end the agreement if necessary, enabling a smooth transition for both the accounting firm and the auditor. It is worth noting that while the Bronx New York Agreement by an Accounting Firm to Employ an Auditor as a Self-Employed Independent Contractor generally follows a standard structure, there may be variations or additional clauses based on the specific needs and requirements of the accounting firm and the auditor. These variations could include provisions related to intellectual property rights, dispute resolution mechanisms, non-compete agreements, and non-solicitation clauses. By utilizing the Bronx New York Agreement by an Accounting Firm to Employ an Auditor as a Self-Employed Independent Contractor, both the accounting firm and the auditor can establish a clear understanding of their professional relationship, thereby minimizing potential misunderstandings and conflicts.