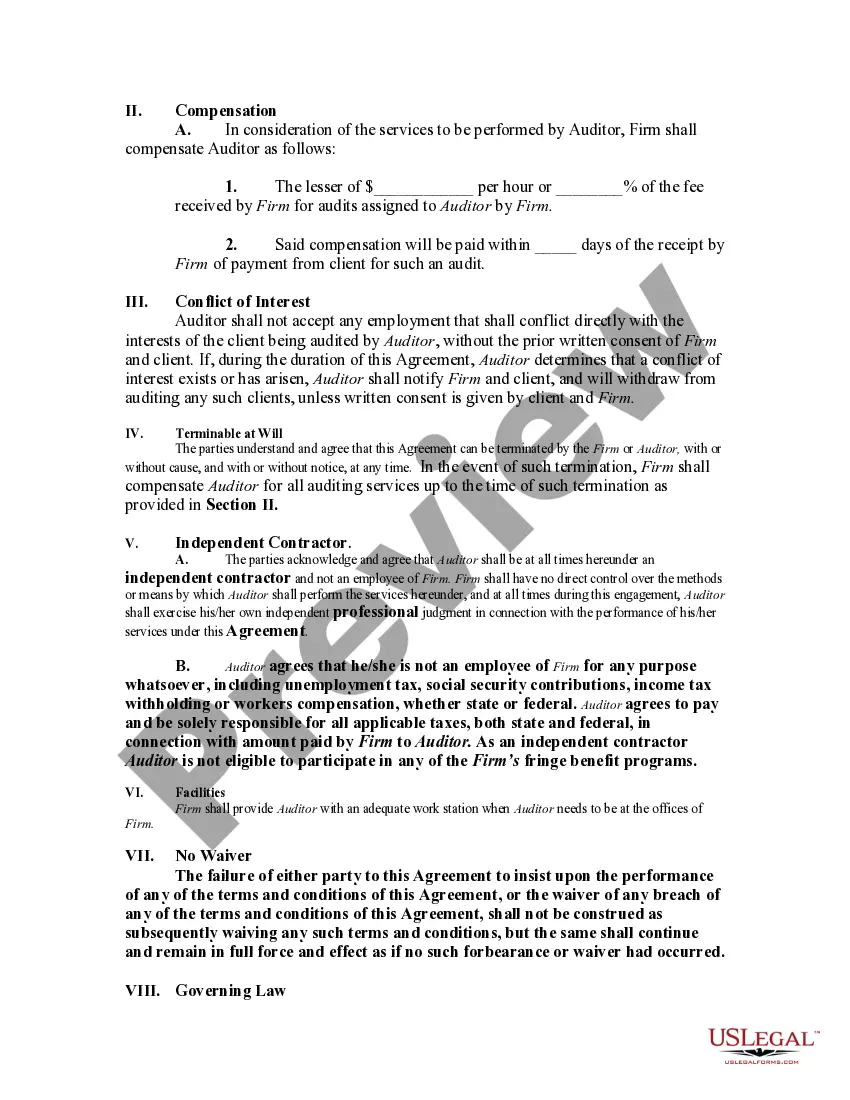

Although no definite rule exists for determining whether one is an independent contractor or an employee, certain indicia of the status of an independent contractor are recognized, and the insertion of provisions embodying these indicia in the contract will help to insure that the relationship reflects the intention of the parties. These indicia generally relate to the basic issue of control. The general test of what constitutes an independent contractor relationship involves which party has the right to direct what is to be done, and how and when. Another important test involves the method of payment of the contractor.

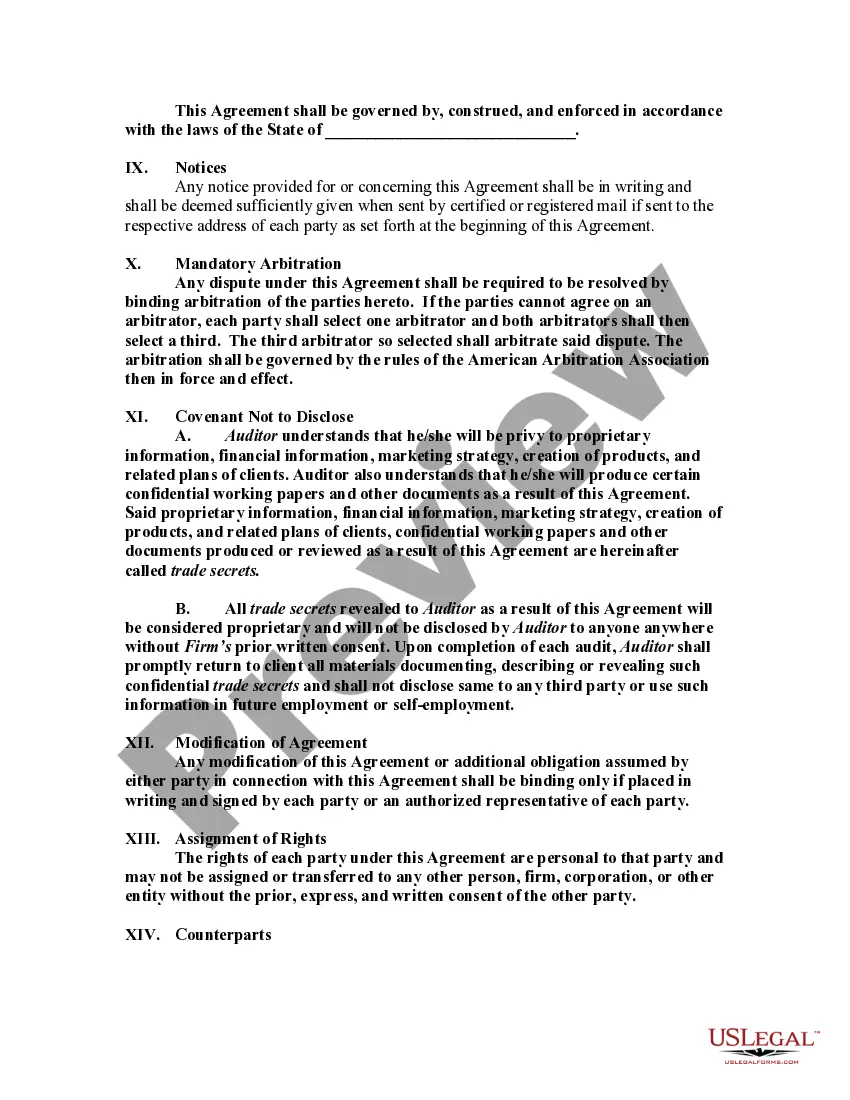

Clark Nevada Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a legally binding document that outlines the terms and conditions of the working relationship between an accounting firm and an auditor who will be engaged as a self-employed independent contractor. This agreement is beneficial for both parties as it clarifies the expectations, responsibilities, and compensation arrangements involved in the engagement. The Clark Nevada Agreement is named after the applicable jurisdiction, which could vary depending on the location of the accounting firm. This agreement is specifically tailored for auditors being employed as self-employed independent contractors, and it encompasses various types, such as: 1. Full-Time Engagement Agreement: This type of agreement outlines the terms for auditors who will be engaged by the accounting firm on a full-time basis. It includes details regarding working hours, reporting structure, client assignments, and remuneration criteria. 2. Part-Time Engagement Agreement: For auditors who are engaged on a part-time basis, this agreement defines the scope of work, specific days and hours of availability, and compensation for the services rendered. 3. Project-Based Engagement Agreement: This agreement is designed for auditors who are engaged for a specific project or assignment. It details the scope of work, project timeline, expected deliverables, and compensation terms. 4. Retainer Agreement: In some cases, an accounting firm may engage an auditor on a retainer basis to secure their availability for future projects or to offer ongoing consulting services. This agreement establishes the monthly or yearly retainer fee, the number of hours for which the auditor needs to be available, and the specific services covered. Keywords: — Clark NevadAgreementen— - Accounting Firm — Auditor - Self-Employed Independent Contractor — EmploymenAgreementen— - Engagement Agreement — Full-Time Audito— - Part-Time Auditor - Project-Based Auditor — RetaineAgreementen— - Scope of Work - Responsibilities Compensationatio— - Reporting StructureClark Nevada Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a legally binding document that outlines the terms and conditions of the working relationship between an accounting firm and an auditor who will be engaged as a self-employed independent contractor. This agreement is beneficial for both parties as it clarifies the expectations, responsibilities, and compensation arrangements involved in the engagement. The Clark Nevada Agreement is named after the applicable jurisdiction, which could vary depending on the location of the accounting firm. This agreement is specifically tailored for auditors being employed as self-employed independent contractors, and it encompasses various types, such as: 1. Full-Time Engagement Agreement: This type of agreement outlines the terms for auditors who will be engaged by the accounting firm on a full-time basis. It includes details regarding working hours, reporting structure, client assignments, and remuneration criteria. 2. Part-Time Engagement Agreement: For auditors who are engaged on a part-time basis, this agreement defines the scope of work, specific days and hours of availability, and compensation for the services rendered. 3. Project-Based Engagement Agreement: This agreement is designed for auditors who are engaged for a specific project or assignment. It details the scope of work, project timeline, expected deliverables, and compensation terms. 4. Retainer Agreement: In some cases, an accounting firm may engage an auditor on a retainer basis to secure their availability for future projects or to offer ongoing consulting services. This agreement establishes the monthly or yearly retainer fee, the number of hours for which the auditor needs to be available, and the specific services covered. Keywords: — Clark NevadAgreementen— - Accounting Firm — Auditor - Self-Employed Independent Contractor — EmploymenAgreementen— - Engagement Agreement — Full-Time Audito— - Part-Time Auditor - Project-Based Auditor — RetaineAgreementen— - Scope of Work - Responsibilities Compensationatio— - Reporting Structure