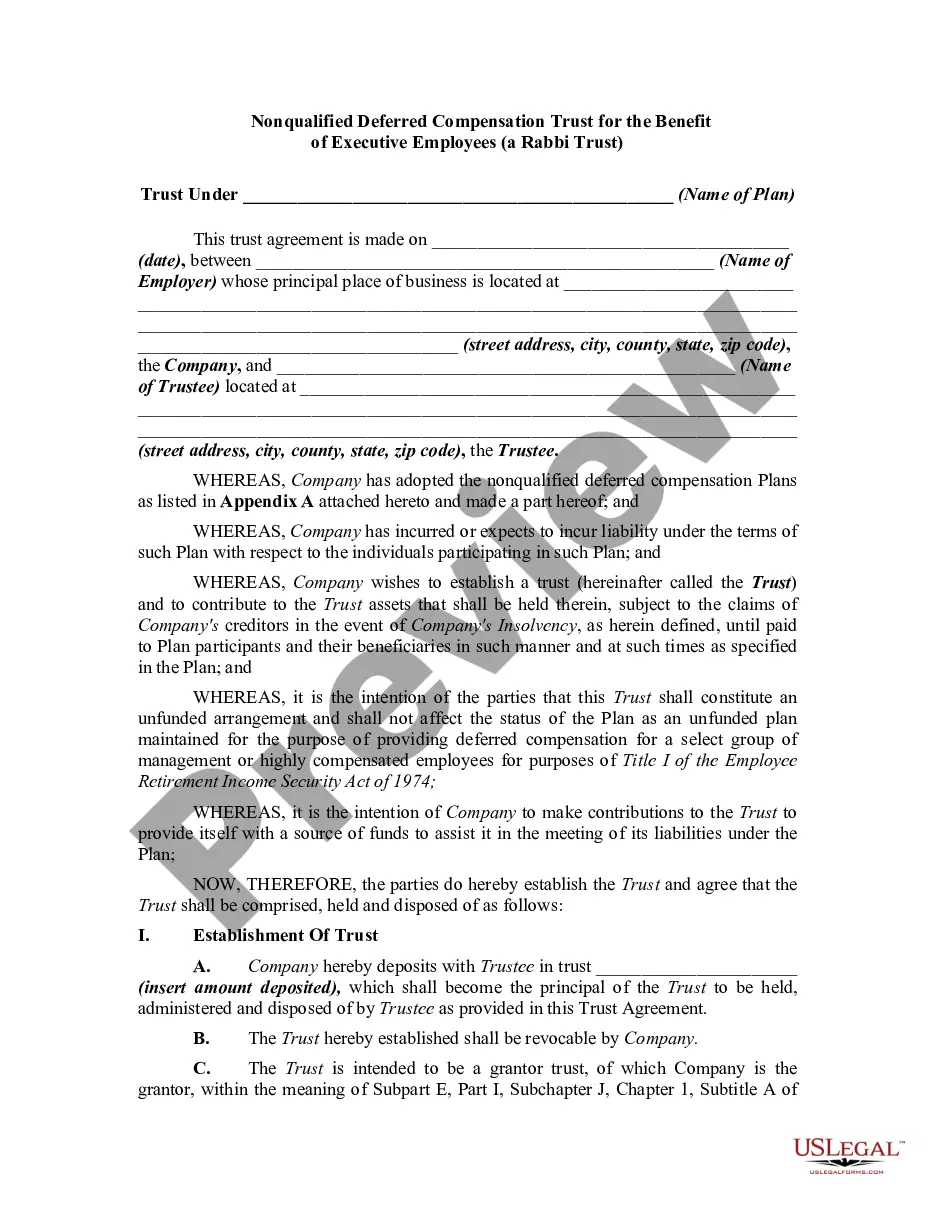

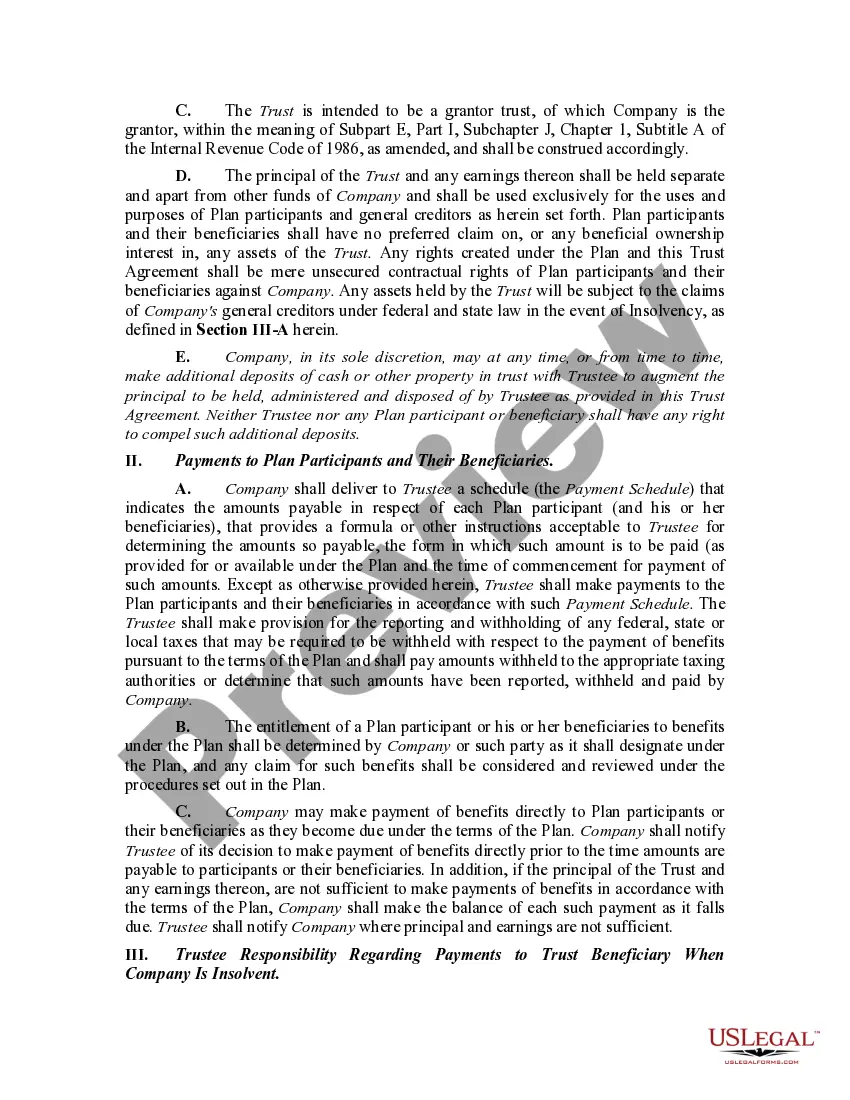

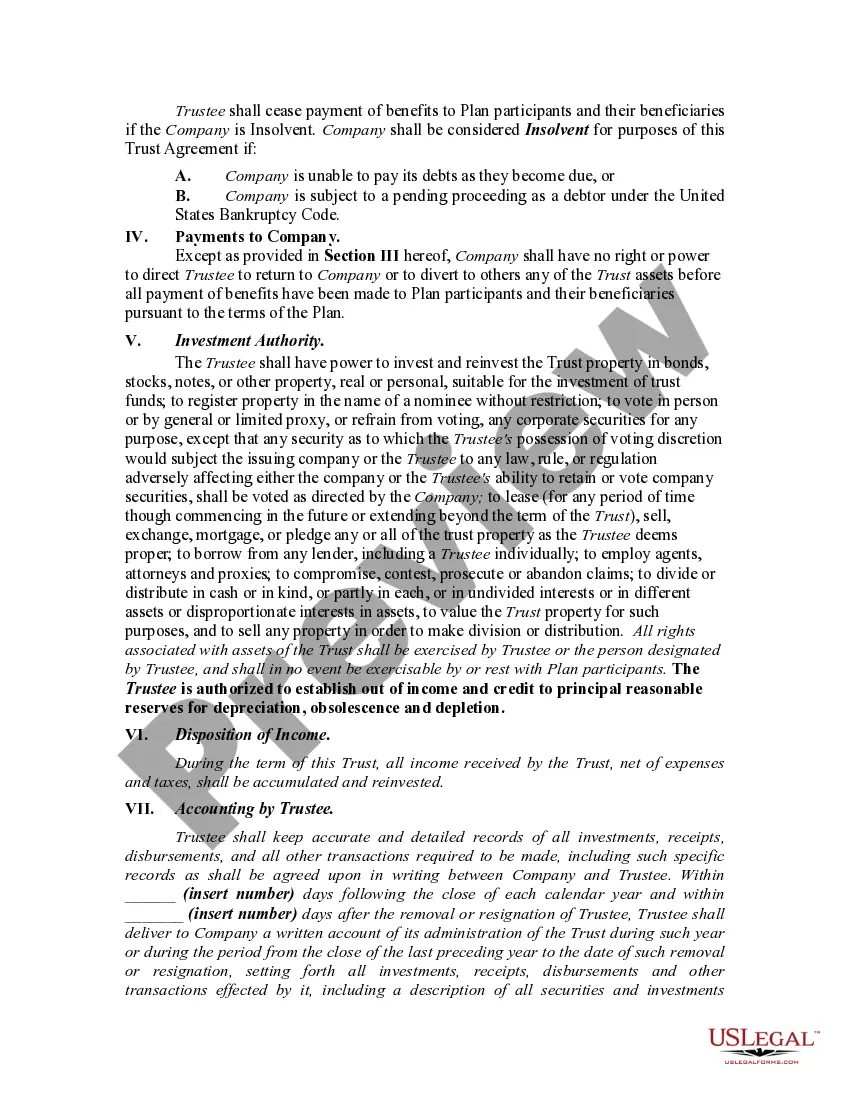

A method of deferring compensation for executives is the use of a rabbi trust. The instrument was named - rabbit trust - because it was first used to provide deferred compensation for a rabbi. Generally, the Internal Revenue Service (IRS) requires that the funds in a rabbi trust must be subject to the claims of the employer's creditors.

This information is current as of December, 2007, but is subject to change if tax laws or IRS regulations change. Current tax laws should be consulted at the time of the preparation of such a trust.

The Oakland Michigan Nonqualified Deferred Compensation Trust for the Benefit of Executive Employees, commonly known as a Rabbi Trust, is a specialized financial arrangement designed to provide supplemental retirement benefits for highly compensated executives. This trust is established by employers based in Oakland, Michigan, as a means to attract and retain top-level talent by offering additional retirement benefits that are not subject to certain tax restrictions imposed on qualified retirement plans such as 401(k)s or pension plans. As a nonqualified deferred compensation trust, the Rabbi Trust allows executives to defer a portion of their current compensation until a later date, typically retirement, when they can receive the deferred amount along with accumulated earnings. By deferring compensation, executives can effectively lower their current taxable income while potentially benefiting from tax savings in the future. The Oakland Michigan Nonqualified Deferred Compensation Trust for the Benefit of Executive Employees can take various forms, depending on the specifics of the employer's plan. Some common types of structures associated with a Rabbi Trust include: 1. Salary Deferral Trust: Executives contribute a portion of their salary to the trust, which is then invested on their behalf. The contributions and any earnings on these amounts are not taxed until they are distributed to the executive at a later date. 2. Bonus Deferral Trust: Similar to the salary deferral trust, executives can choose to defer a portion of their annual bonuses into the trust. By doing so, they can potentially reduce their tax liability in the year of receipt and enjoy the benefits of tax deferral. 3. Stock Appreciation Rights (SAR) Trust: In some cases, employers may grant executives the opportunity to defer the receipt of stock appreciation rights. These rights grant the executive the potential to benefit from the appreciation in the company's stock value over a specified period. By deferring the receipt of the stock appreciation rights, executives can delay the tax consequences associated with them. 4. Supplemental Executive Retirement Plan (SERP) Trust: This type of trust is specifically designed to provide additional retirement benefits to executives above and beyond what is offered through traditional retirement plans. Contributions made by the employer into the SERP trust are typically invested and held on behalf of the executive until retirement. It is important to note that while the Oakland Michigan Nonqualified Deferred Compensation Trust for the Benefit of Executive Employees — a Rabbi Trust presents potential tax advantages and flexibility for highly compensated executives, it also carries certain risks and complexities. Executives should consult with qualified financial and legal advisors to fully understand the implications and requirements associated with participating in such a trust.The Oakland Michigan Nonqualified Deferred Compensation Trust for the Benefit of Executive Employees, commonly known as a Rabbi Trust, is a specialized financial arrangement designed to provide supplemental retirement benefits for highly compensated executives. This trust is established by employers based in Oakland, Michigan, as a means to attract and retain top-level talent by offering additional retirement benefits that are not subject to certain tax restrictions imposed on qualified retirement plans such as 401(k)s or pension plans. As a nonqualified deferred compensation trust, the Rabbi Trust allows executives to defer a portion of their current compensation until a later date, typically retirement, when they can receive the deferred amount along with accumulated earnings. By deferring compensation, executives can effectively lower their current taxable income while potentially benefiting from tax savings in the future. The Oakland Michigan Nonqualified Deferred Compensation Trust for the Benefit of Executive Employees can take various forms, depending on the specifics of the employer's plan. Some common types of structures associated with a Rabbi Trust include: 1. Salary Deferral Trust: Executives contribute a portion of their salary to the trust, which is then invested on their behalf. The contributions and any earnings on these amounts are not taxed until they are distributed to the executive at a later date. 2. Bonus Deferral Trust: Similar to the salary deferral trust, executives can choose to defer a portion of their annual bonuses into the trust. By doing so, they can potentially reduce their tax liability in the year of receipt and enjoy the benefits of tax deferral. 3. Stock Appreciation Rights (SAR) Trust: In some cases, employers may grant executives the opportunity to defer the receipt of stock appreciation rights. These rights grant the executive the potential to benefit from the appreciation in the company's stock value over a specified period. By deferring the receipt of the stock appreciation rights, executives can delay the tax consequences associated with them. 4. Supplemental Executive Retirement Plan (SERP) Trust: This type of trust is specifically designed to provide additional retirement benefits to executives above and beyond what is offered through traditional retirement plans. Contributions made by the employer into the SERP trust are typically invested and held on behalf of the executive until retirement. It is important to note that while the Oakland Michigan Nonqualified Deferred Compensation Trust for the Benefit of Executive Employees — a Rabbi Trust presents potential tax advantages and flexibility for highly compensated executives, it also carries certain risks and complexities. Executives should consult with qualified financial and legal advisors to fully understand the implications and requirements associated with participating in such a trust.