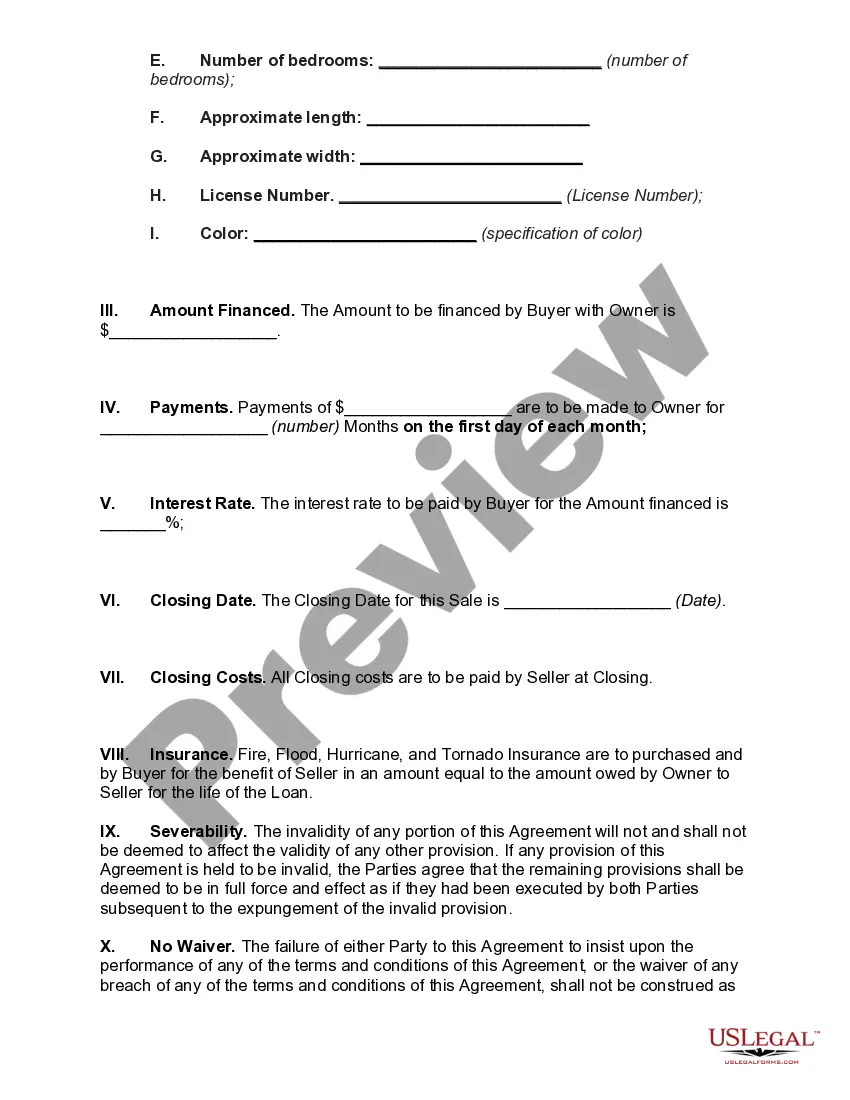

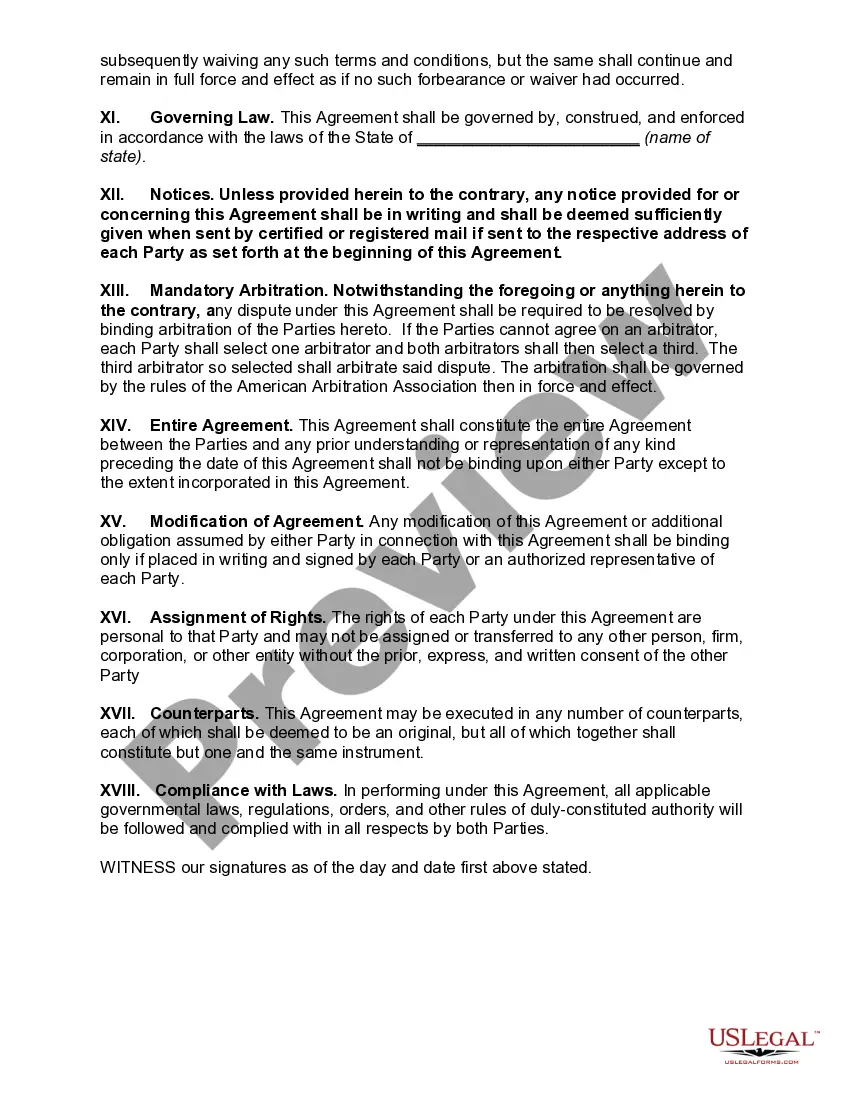

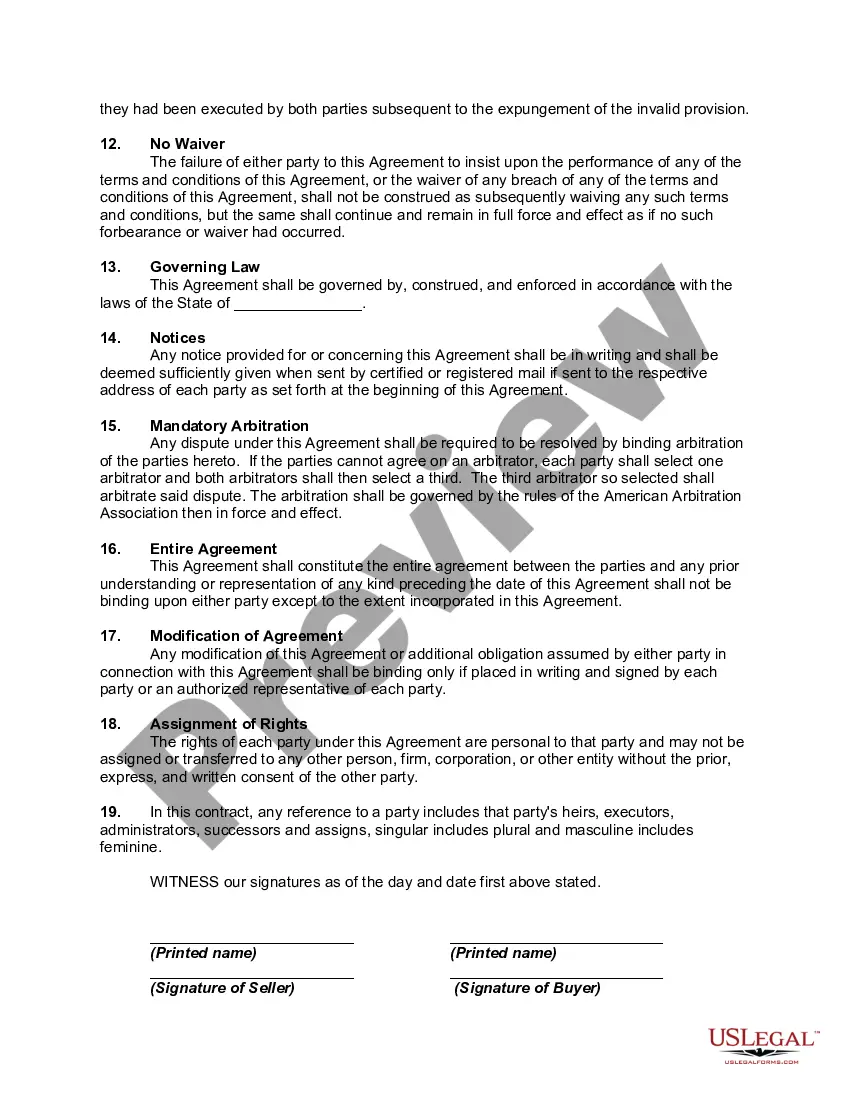

Contra Costa California Owner Financing Contract for Mobile Home: Understanding the Different Types When it comes to purchasing a mobile home in Contra Costa County, California, owner financing can be an excellent option for buyers. This financing method allows individuals to buy a mobile home directly from the current owner, without requiring traditional mortgage lenders. In this detailed description, we will explore what a Contra Costa California Owner Financing Contract for Mobile Home entails and outline the different types available. 1. Standard Owner Financing Contract: The standard owner financing contract for a mobile home in Contra Costa County is a legally binding agreement between the buyer and seller. It outlines the terms of the purchase, including the sale price, down payment, interest rate, repayment period, and any other specific conditions agreed upon by both parties. This type of contract provides greater flexibility for buyers who may not qualify for conventional financing options. 2. Lease Purchase Agreement: In some cases, the owner may offer a lease purchase agreement instead of a traditional owner financing contract. This arrangement allows the buyer to lease the mobile home with the intention of purchasing it at the end of the agreed-upon lease period. A portion of the monthly lease payments may be credited towards the eventual purchase, offering potential buyers more time to secure traditional financing or improve their financial situation. 3. Land Contract or Contract for Deed: Another variation of an owner financing contract is a land contract or contract for deed. With this arrangement, the seller retains the title to the mobile home while the buyer makes regular payments over a specific period. Once the final payment is made, the title is transferred to the buyer. This type of contract protects both parties as it typically includes provisions for default, property maintenance, and other crucial aspects of the buyer-seller relationship. 4. Lease Option Contract: A lease option contract is similar to a lease purchase agreement; however, it offers the buyer more flexibility. In this type of contract, the buyer leases the mobile home with an option to purchase it in the future. The agreed-upon purchase price is set at the beginning, allowing the buyer to secure the property at that price regardless of any market appreciation during the lease period. This can be an appealing option for buyers who want more time to save for a down payment or improve their credit score before purchasing the home. In summary, Contra Costa County, California, offers various types of owner financing contracts for mobile homes, each catering to different needs and circumstances. These contracts provide an opportunity for buyers to achieve homeownership while bypassing traditional mortgage lenders. Whether you opt for a standard owner financing contract, a lease purchase agreement, a land contract, or a lease option contract, ensure that you thoroughly understand the terms and conditions before committing to any agreement.

Contra Costa California Owner Financing Contract for Moblie Home

Description

How to fill out Contra Costa California Owner Financing Contract For Moblie Home?

Laws and regulations in every sphere differ around the country. If you're not an attorney, it's easy to get lost in countless norms when it comes to drafting legal documentation. To avoid costly legal assistance when preparing the Contra Costa Owner Financing Contract for Moblie Home, you need a verified template legitimate for your county. That's when using the US Legal Forms platform is so beneficial.

US Legal Forms is a trusted by millions web library of more than 85,000 state-specific legal forms. It's a perfect solution for professionals and individuals searching for do-it-yourself templates for various life and business scenarios. All the documents can be used many times: once you pick a sample, it remains accessible in your profile for subsequent use. Thus, when you have an account with a valid subscription, you can simply log in and re-download the Contra Costa Owner Financing Contract for Moblie Home from the My Forms tab.

For new users, it's necessary to make a few more steps to obtain the Contra Costa Owner Financing Contract for Moblie Home:

- Take a look at the page content to ensure you found the right sample.

- Utilize the Preview option or read the form description if available.

- Look for another doc if there are inconsistencies with any of your requirements.

- Use the Buy Now button to obtain the document when you find the proper one.

- Opt for one of the subscription plans and log in or create an account.

- Choose how you prefer to pay for your subscription (with a credit card or PayPal).

- Select the format you want to save the file in and click Download.

- Fill out and sign the document on paper after printing it or do it all electronically.

That's the simplest and most cost-effective way to get up-to-date templates for any legal purposes. Locate them all in clicks and keep your paperwork in order with the US Legal Forms!