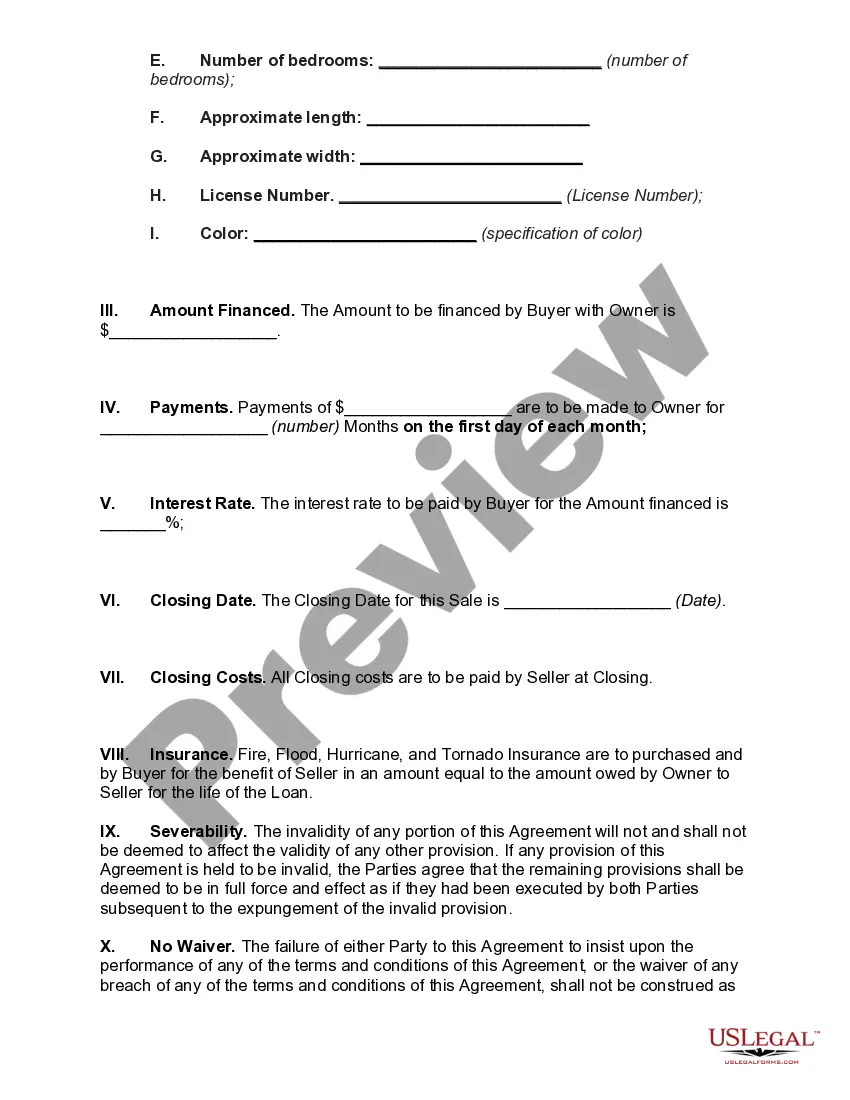

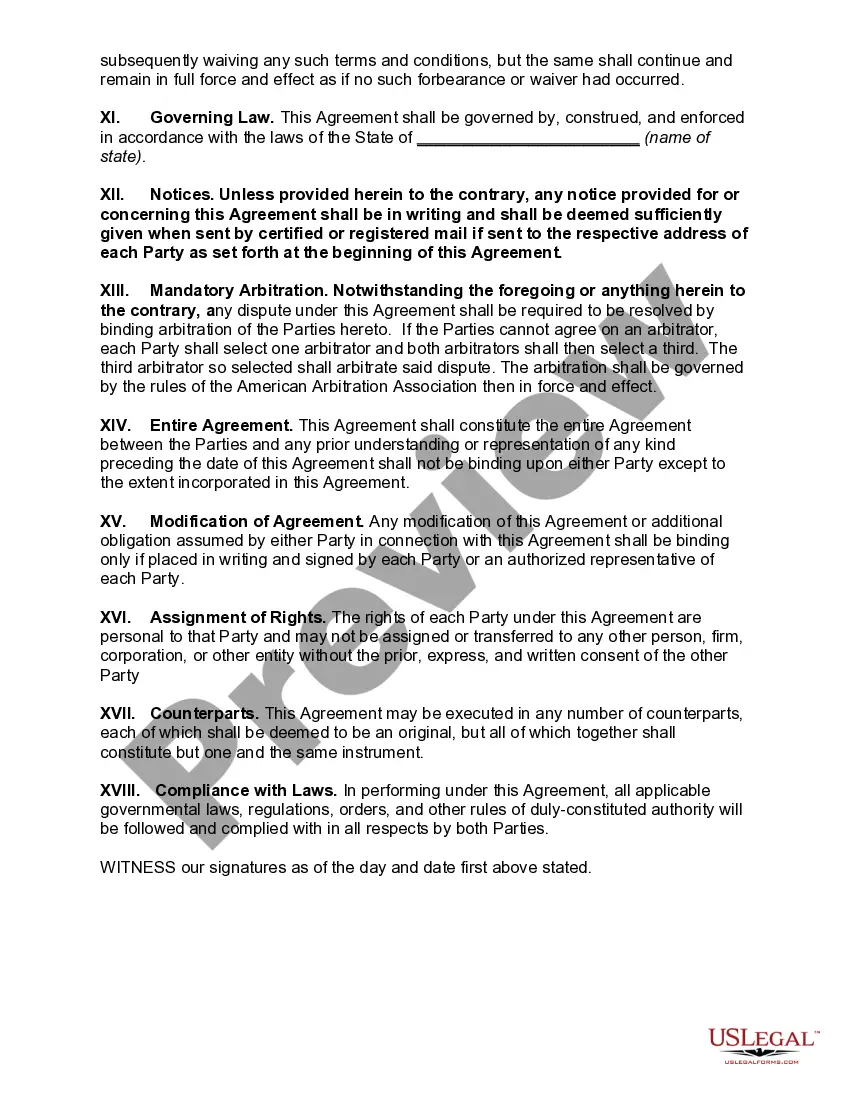

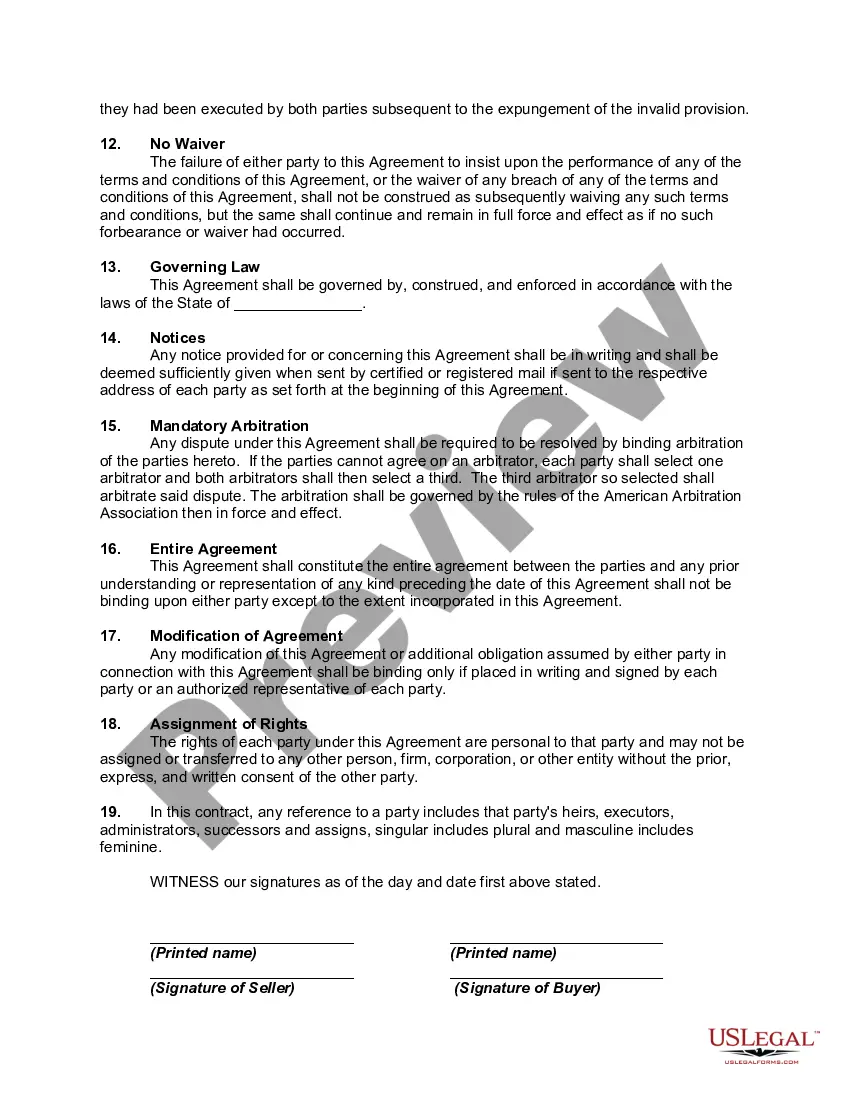

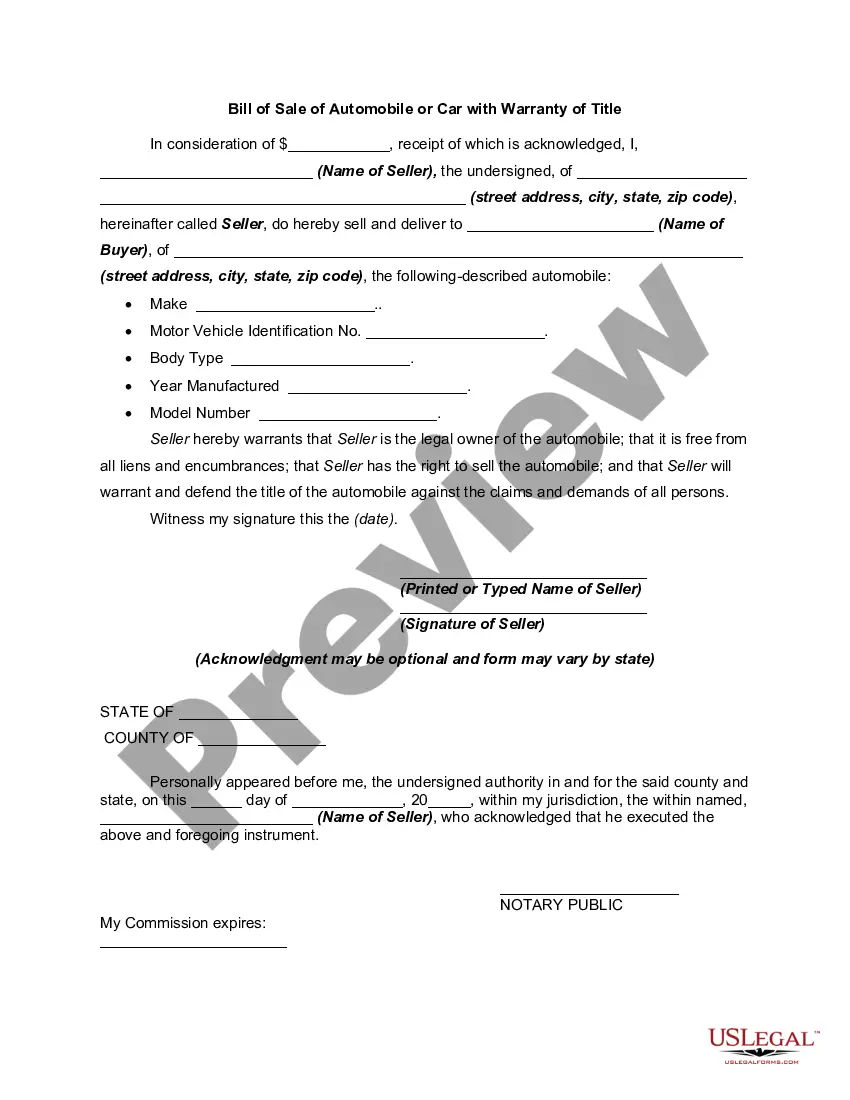

In Mecklenburg County, North Carolina, owner financing contracts for mobile homes provide a convenient alternative to traditional mortgage lending. These contracts allow buyers to purchase a mobile home with direct financing from the seller, eliminating the need for a mortgage loan from a bank or financial institution. This arrangement can be beneficial for both the seller and buyer, as it opens up opportunities for individuals who may not qualify for conventional financing or prefer more flexible payment terms. The Mecklenburg North Carolina owner financing contracts for mobile homes may vary in structure and terms depending on the agreement between the buyer and seller. Here are a few types that are commonly encountered: 1. Installment Sale Contract: This type of owner financing involves a seller acting as the lender and the buyer making regular payments, typically on a monthly basis, to purchase the mobile home over time. A promissory note is usually signed, outlining the terms and conditions of the loan, including the interest rate, repayment period, and any penalties for default. 2. Lease-Purchase Agreement: In this arrangement, the buyer agrees to lease the mobile home from the seller for a predetermined period, with an option to purchase the property at the end of the lease term. A portion of the monthly lease payments may be credited towards the purchase price. This type of contract provides the buyer with time to improve their credit or save for a down payment while living in the home. 3. Contract for Deed: Also known as a land contract or agreement for deed, this financing option involves the seller financing the purchase of the mobile home while retaining legal ownership until the buyer fulfills all payment obligations. Once the contract's terms are completed, ownership is transferred to the buyer. During the contract period, the buyer usually has the right to possess and use the mobile home. Mecklenburg North Carolina owner financing contracts for mobile homes offer advantages to both buyers and sellers. Buyers with less-than-perfect credit scores or insufficient cash for a down payment can still achieve homeownership. Sellers can generate passive income, benefit from interest income, and potentially sell their mobile home faster due to the increased pool of potential buyers. It is essential for both parties to consult an attorney or a real estate professional experienced in owner financing transactions to ensure all legal requirements and obligations are met. Additionally, conducting thorough due diligence, such as obtaining a title search and inspection, is crucial to protect the buyer's interests and avoid potential complications.

Mecklenburg North Carolina Owner Financing Contract for Moblie Home

Description

How to fill out Mecklenburg North Carolina Owner Financing Contract For Moblie Home?

Preparing legal paperwork can be burdensome. In addition, if you decide to ask an attorney to draft a commercial contract, papers for ownership transfer, pre-marital agreement, divorce papers, or the Mecklenburg Owner Financing Contract for Moblie Home, it may cost you a fortune. So what is the best way to save time and money and create legitimate documents in total compliance with your state and local laws and regulations? US Legal Forms is a perfect solution, whether you're searching for templates for your personal or business needs.

US Legal Forms is largest online catalog of state-specific legal documents, providing users with the up-to-date and professionally checked templates for any use case gathered all in one place. Consequently, if you need the current version of the Mecklenburg Owner Financing Contract for Moblie Home, you can easily locate it on our platform. Obtaining the papers takes a minimum of time. Those who already have an account should check their subscription to be valid, log in, and select the sample by clicking on the Download button. If you haven't subscribed yet, here's how you can get the Mecklenburg Owner Financing Contract for Moblie Home:

- Look through the page and verify there is a sample for your area.

- Check the form description and use the Preview option, if available, to ensure it's the template you need.

- Don't worry if the form doesn't suit your requirements - search for the right one in the header.

- Click Buy Now when you find the required sample and pick the best suitable subscription.

- Log in or sign up for an account to purchase your subscription.

- Make a payment with a credit card or via PayPal.

- Opt for the document format for your Mecklenburg Owner Financing Contract for Moblie Home and download it.

Once finished, you can print it out and complete it on paper or import the template to an online editor for a faster and more convenient fill-out. US Legal Forms allows you to use all the documents ever purchased many times - you can find your templates in the My Forms tab in your profile. Try it out now!