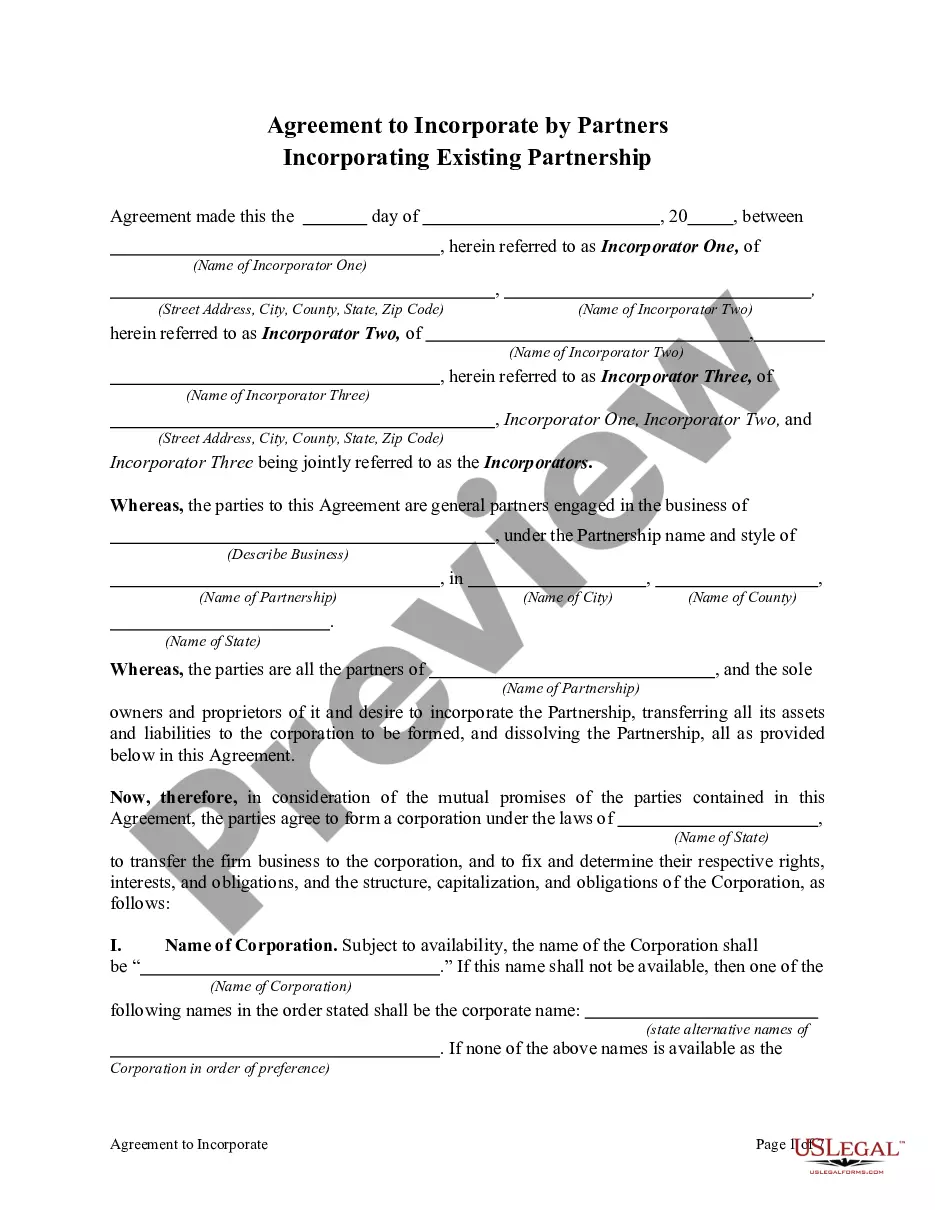

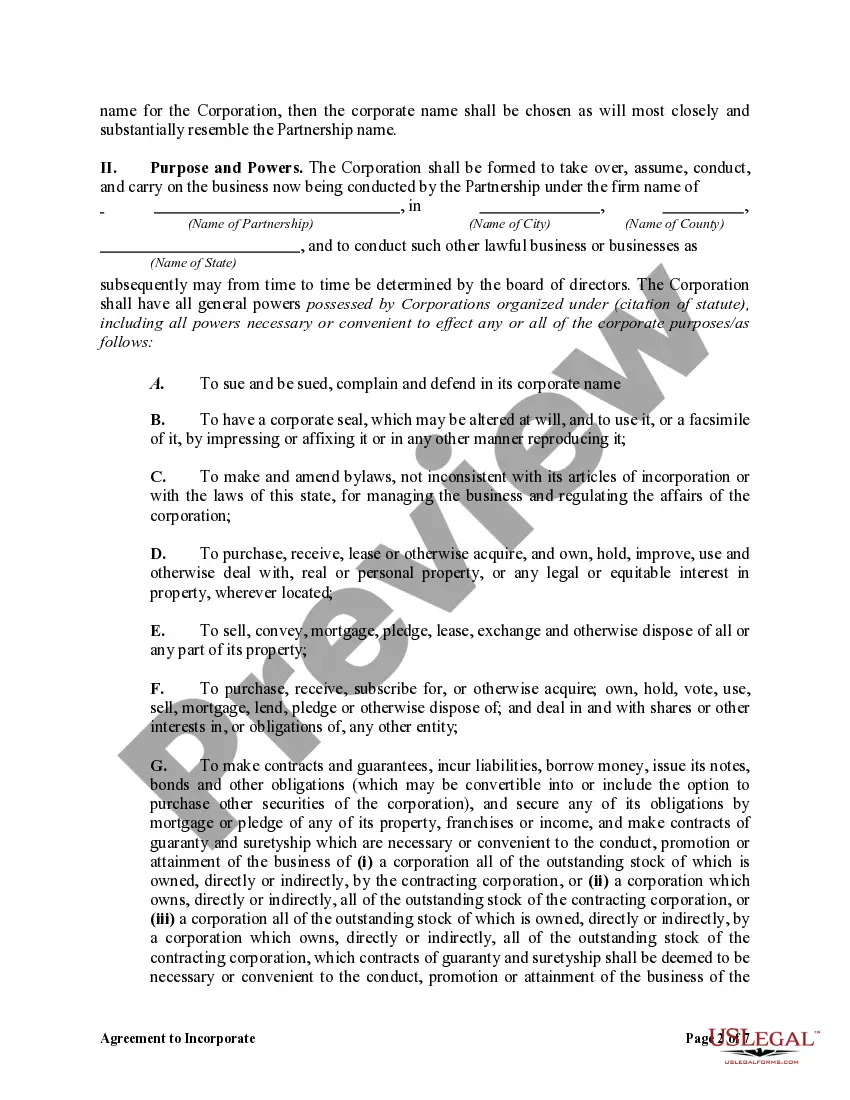

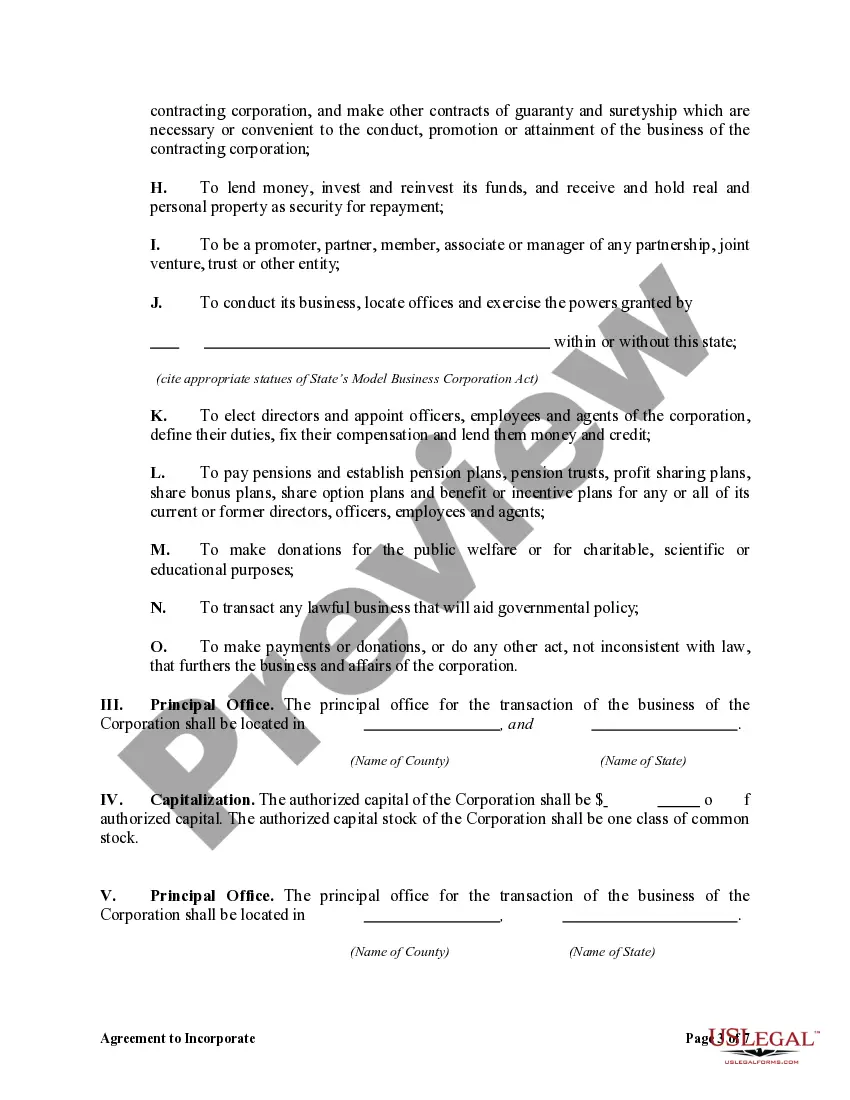

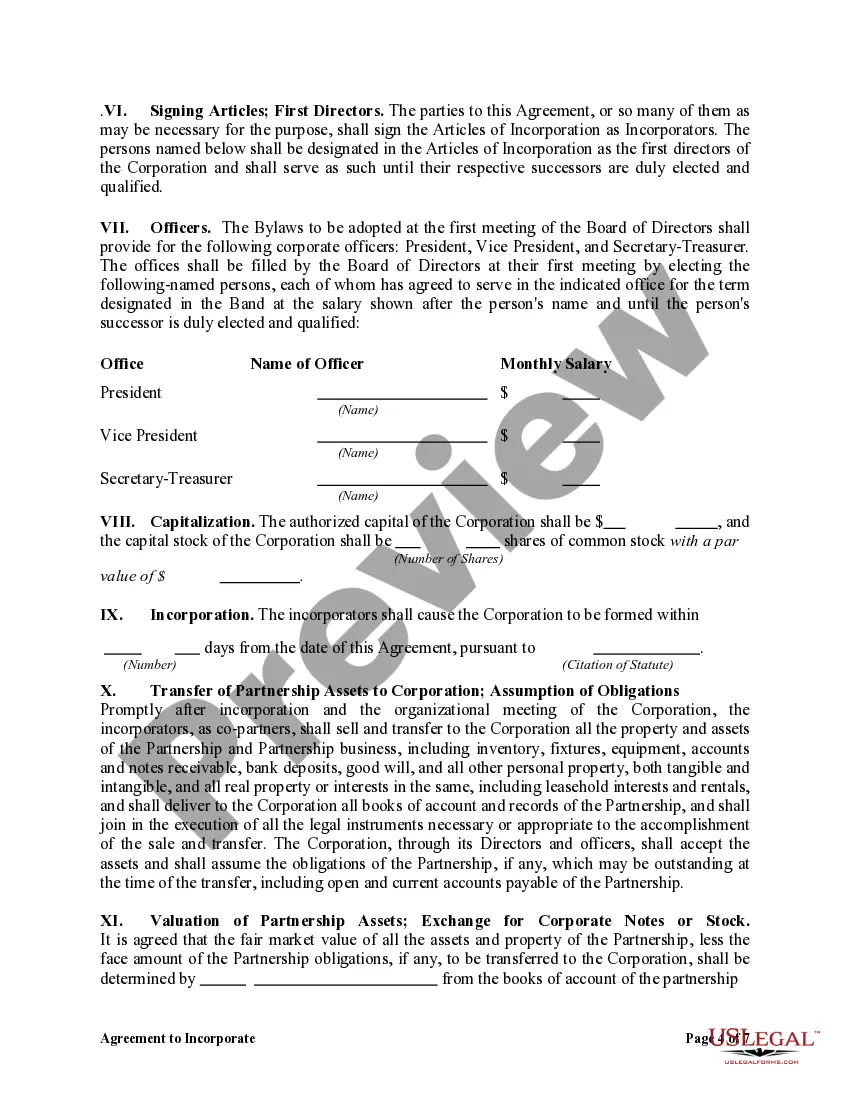

The Nassau New York Agreement to Incorporate by Partners Incorporating Existing Partnership is a legal document that outlines the process and terms for converting a partnership into a corporation in Nassau, New York. This agreement provides a comprehensive framework for partners who wish to transfer their existing partnership business into a corporate entity while preserving the assets and operations of the original partnership. The agreement starts by defining the specific details of the partnership and the proposed corporation. It includes the names and addresses of the partners, the name of the partnership, and the name under which the new corporation will operate. It also outlines the purpose and objectives of the corporation and any changes to the partnership's existing business structure. One of the key aspects of this agreement is the allocation and transfer of assets and liabilities from the partnership to the corporation. It specifies the distribution of partnership assets, including cash, accounts receivable, inventory, real estate, and any other properties. The agreement also addresses the division of liabilities, ensuring that all outstanding debts, loans, and obligations are properly assigned and assumed by the new corporation. The tax implications of the conversion are also covered in this agreement. It discusses the consequences for both the partnership and individual partners, including any tax liabilities, deductions, and benefits associated with the conversion. Partners may choose to consult with tax professionals to ensure compliance with relevant regulations and to optimize their tax strategies during this transition. Additional provisions within the Nassau New York Agreement to Incorporate by Partners Incorporating Existing Partnership may include voting rights and management responsibilities of the new corporation, restrictions on transferring shares among partners, shareholder agreements, and any other relevant clauses that empower the partnership's conversion into a corporation. While there may not be different "types" of Nassau New York Agreement to Incorporate by Partners Incorporating Existing Partnership, variations can arise based on the unique circumstances and preferences of the partners involved. These agreements can be customized to suit the specific needs of the partnership, such as addressing buyout options, profit-sharing arrangements, or other considerations that partners wish to include in the conversion process. In conclusion, the Nassau New York Agreement to Incorporate by Partners Incorporating Existing Partnership is a vital legal document that helps partners meticulously navigate the conversion from a partnership to a corporation. This comprehensive agreement provides clarity and protection for all parties involved, serving as a foundation for a smooth and successful transition into the corporate realm.

Nassau New York Agreement to Incorporate by Partners Incorporating Existing Partnership

Description

How to fill out Nassau New York Agreement To Incorporate By Partners Incorporating Existing Partnership?

Creating paperwork, like Nassau Agreement to Incorporate by Partners Incorporating Existing Partnership, to manage your legal affairs is a tough and time-consumming task. Many cases require an attorney’s involvement, which also makes this task expensive. However, you can take your legal matters into your own hands and deal with them yourself. US Legal Forms is here to the rescue. Our website comes with more than 85,000 legal forms crafted for different cases and life situations. We make sure each document is compliant with the regulations of each state, so you don’t have to be concerned about potential legal pitfalls compliance-wise.

If you're already aware of our services and have a subscription with US, you know how easy it is to get the Nassau Agreement to Incorporate by Partners Incorporating Existing Partnership form. Go ahead and log in to your account, download the template, and personalize it to your needs. Have you lost your document? No worries. You can find it in the My Forms tab in your account - on desktop or mobile.

The onboarding process of new users is just as straightforward! Here’s what you need to do before getting Nassau Agreement to Incorporate by Partners Incorporating Existing Partnership:

- Make sure that your document is specific to your state/county since the regulations for creating legal papers may vary from one state another.

- Learn more about the form by previewing it or going through a brief description. If the Nassau Agreement to Incorporate by Partners Incorporating Existing Partnership isn’t something you were hoping to find, then take advantage of the search bar in the header to find another one.

- Log in or register an account to begin utilizing our website and download the form.

- Everything looks good on your end? Hit the Buy now button and choose the subscription plan.

- Select the payment gateway and type in your payment information.

- Your form is all set. You can try and download it.

It’s easy to locate and purchase the appropriate document with US Legal Forms. Thousands of organizations and individuals are already benefiting from our extensive collection. Sign up for it now if you want to check what other perks you can get with US Legal Forms!