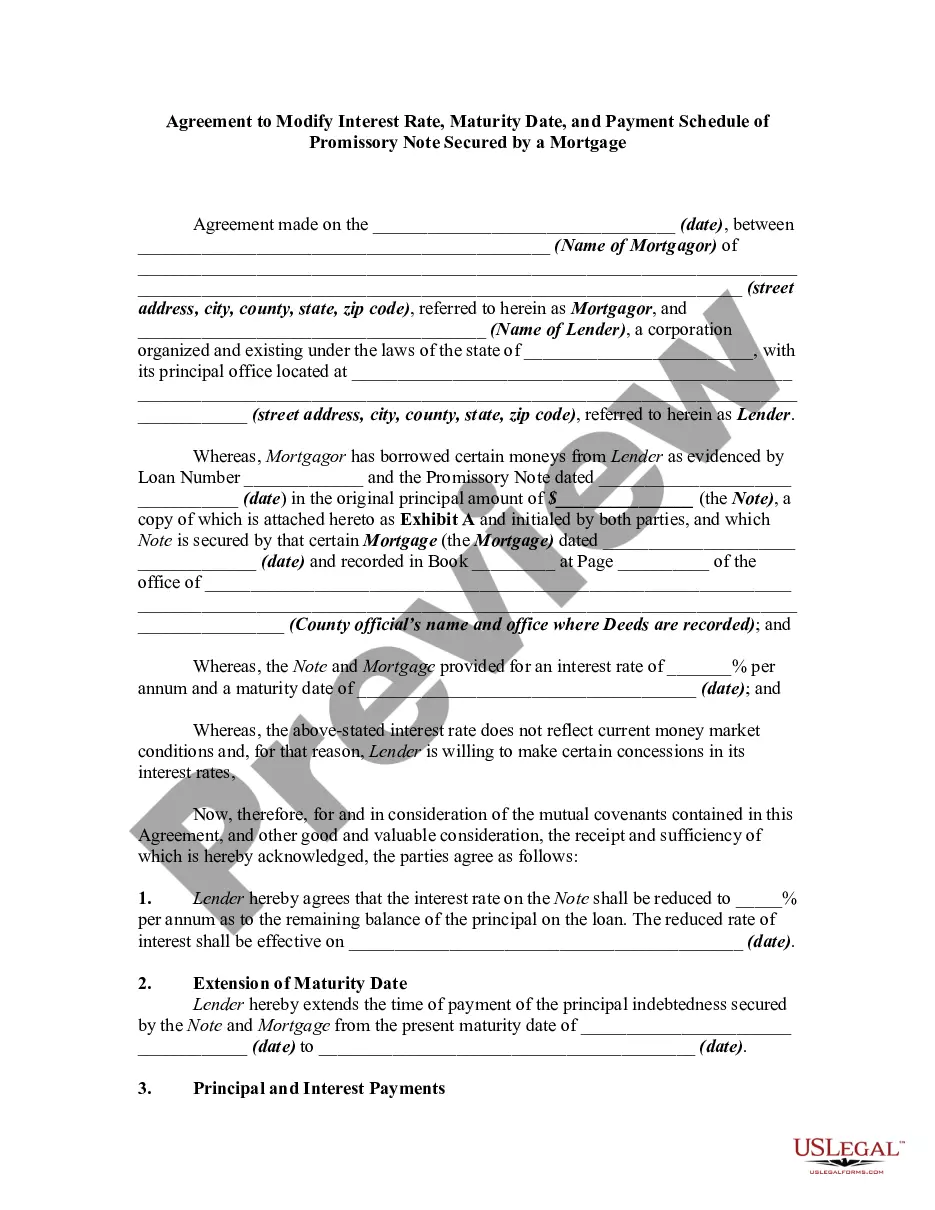

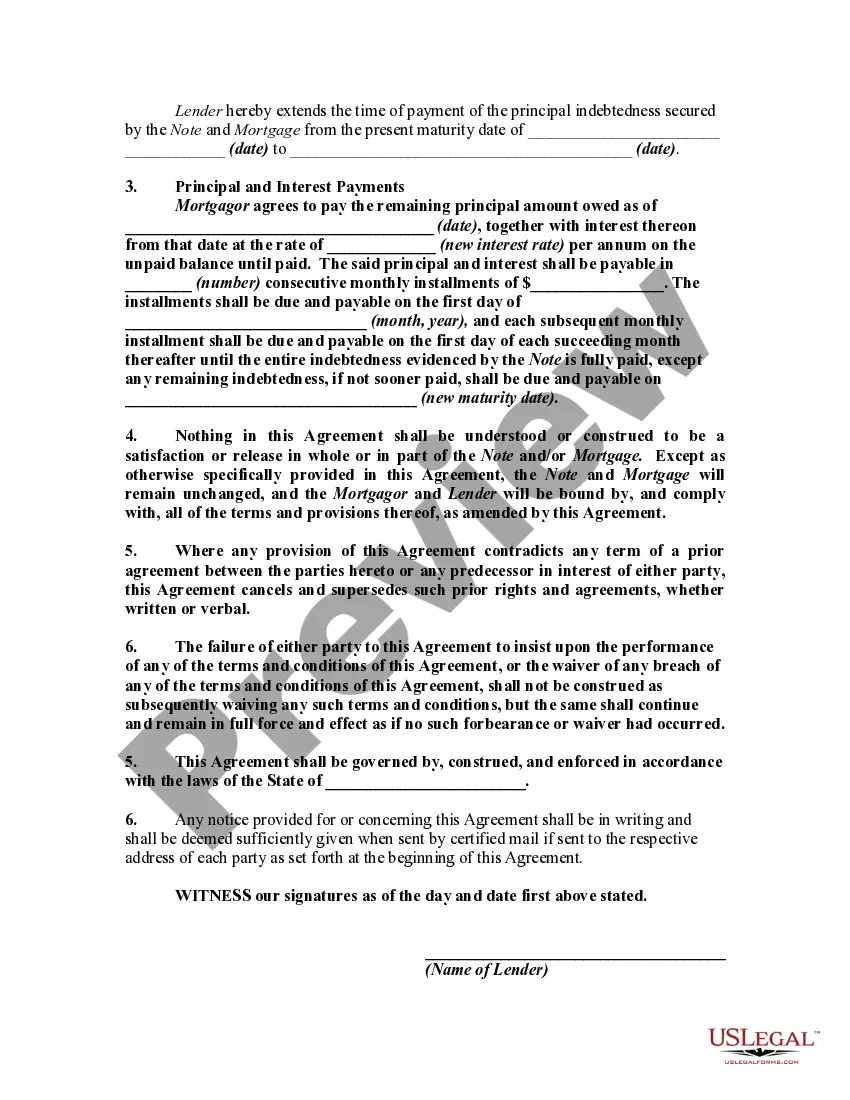

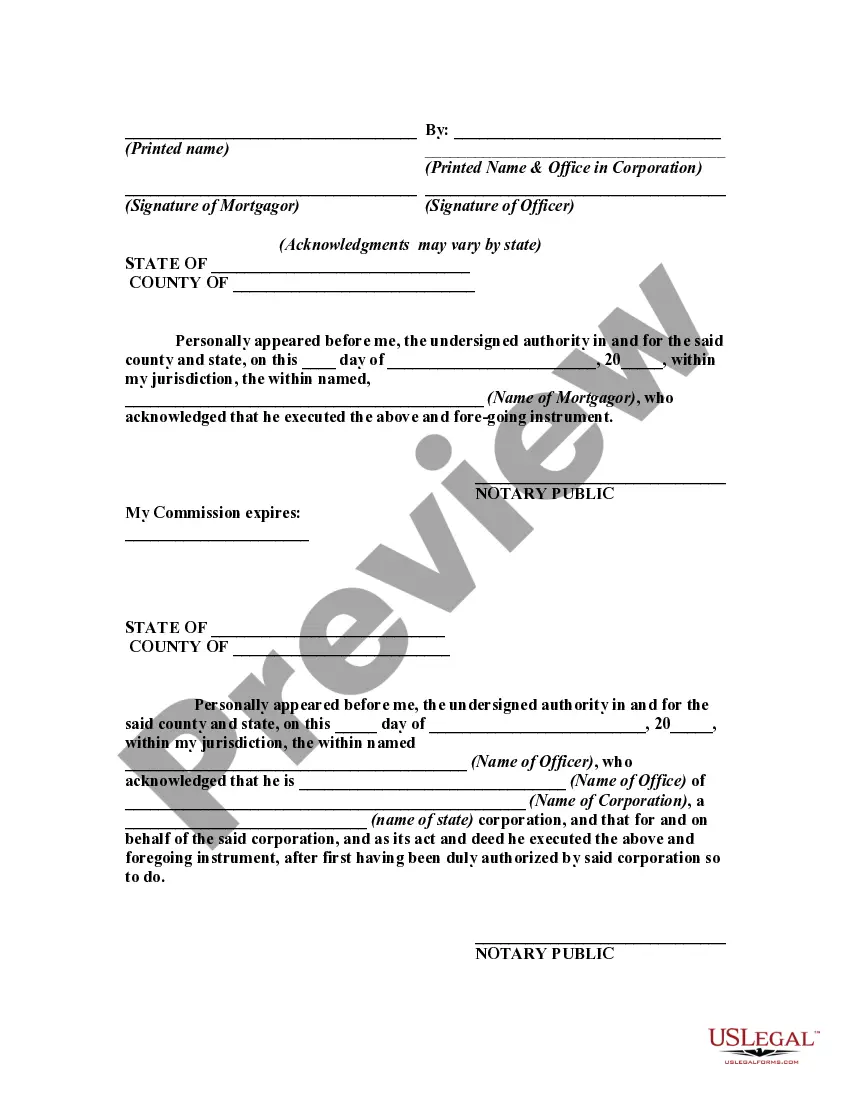

An agreement modifying a loan agreement and mortgage should be signed by both parties to the transaction and recorded in the office of the register of deeds and mortgages where the original mortgage was recorded. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

The Harris Texas Agreement to Modify Interest Rate, Maturity Date, and Payment Schedule of Promissory Note Secured by a Mortgage is a legal document that allows parties to make changes to the original terms of a promissory note secured by a mortgage in Harris County, Texas. This agreement is entered into by the lender and the borrower and outlines the modifications regarding the interest rate, maturity date, and payment schedule of the loan. The purpose of this agreement is to provide flexibility to both parties and help accommodate any changes in financial circumstances or market conditions that may affect the loan. The modifications made will alter the existing terms, ensuring they align with the current needs of the borrower and the capabilities of the lender. By mutually agreeing upon these amendments, the parties can avoid default or foreclosure on the mortgage. The key elements that are typically addressed in the Harris Texas Agreement to Modify Interest Rate, Maturity Date, and Payment Schedule of Promissory Note Secured by a Mortgage include: 1. Interest Rate Modification: This clause allows for a change in the interest rate applied to the remaining balance of the loan. It may involve reducing the rate to make payments more affordable or increasing it to reflect changing market conditions. 2. Maturity Date Extension: The agreement may involve an extension of the maturity date, pushing back the final payment due date. This can help borrowers who are unable to meet the original repayment deadline due to financial constraints. 3. Payment Schedule Revision: The payment schedule is often modified to adjust the monthly installment amount. This could involve reducing the monthly payment to make it more manageable or increasing it to expedite repayment. 4. Prepayment Penalties: If applicable, the agreement should address any changes in prepayment penalties resulting from the modifications made to the interest rate, maturity date, or payment schedule. It's important to note that there may be variations of the Harris Texas Agreement to Modify Interest Rate, Maturity Date, and Payment Schedule of Promissory Note Secured by a Mortgage, tailored to specific situations. These variations could include agreements specifically designed for different types of loans, such as residential mortgages, commercial mortgages, or construction loans. Each variation would contain provisions and clauses that are specific to the particular type of loan being modified. In conclusion, the Harris Texas Agreement to Modify Interest Rate, Maturity Date, and Payment Schedule of Promissory Note Secured by a Mortgage is a legally binding document that allows parties to adjust the original terms of a mortgage loan to better suit their current financial circumstances. It provides a framework for modifying interest rates, maturity dates, and payment schedules, helping borrowers and lenders reach mutually beneficial agreements while avoiding default or foreclosure.