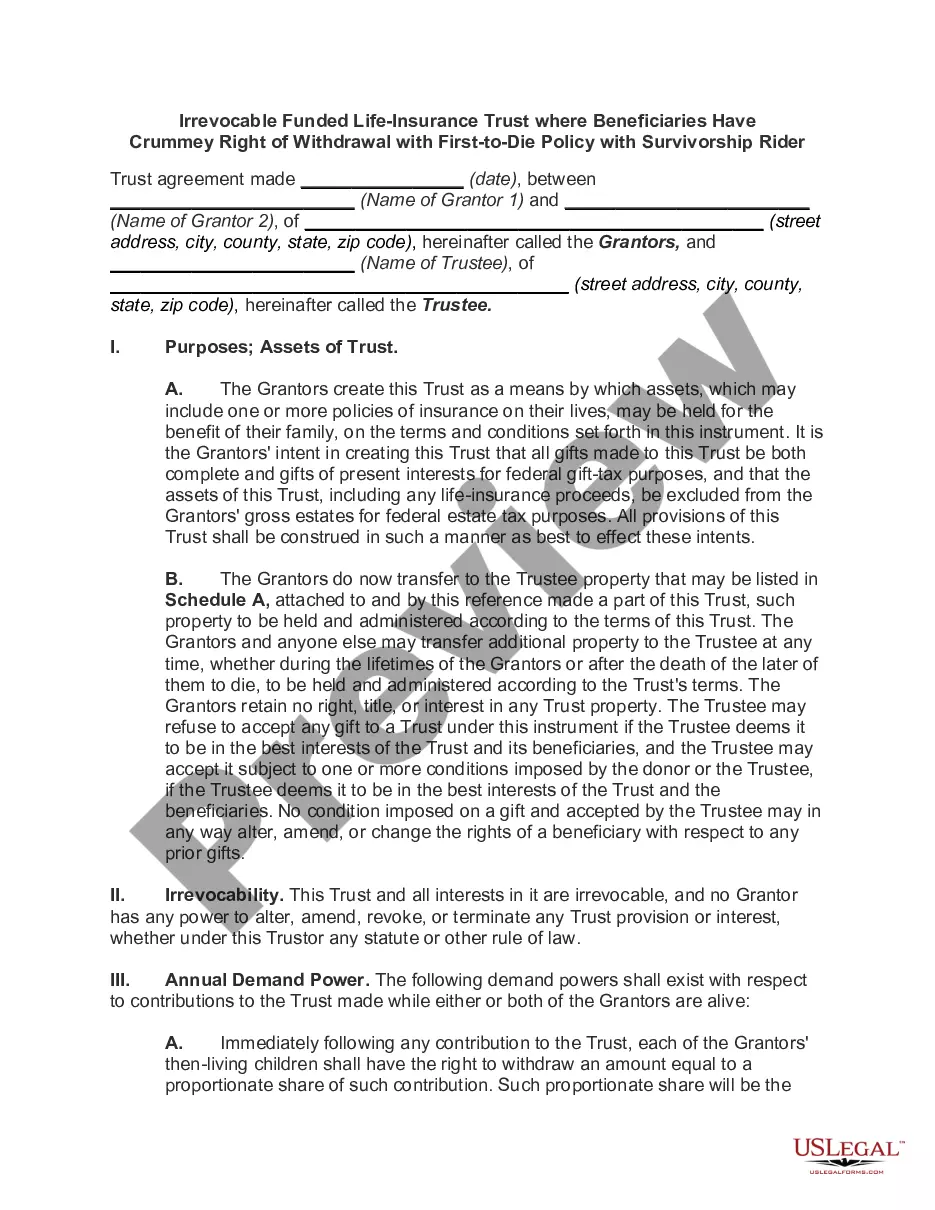

One principal advantage of insurance trusts is that they permit a greater flexibility in investment and distribution than may be effected under settlement options generally included in the policies themselves. Another advantage is that such trusts, like other gifts of insurance policies, may afford substantial estate tax savings.

Fulton Georgia Irrevocable Trust Funded by Life Insurance

Category:

State:

Multi-State

County:

Fulton

Control #:

US-01372BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Irrevocable Trust Funded By Life Insurance?

Are you seeking to swiftly establish a legally-binding Fulton Irrevocable Trust Funded by Life Insurance or perhaps another method to oversee your personal or business matters.

You have the choice of two alternatives: consult a legal professional to prepare a legal document for you or prepare it entirely by yourself. Fortunately, there's an additional option - US Legal Forms. It will assist you in obtaining expertly crafted legal documents without incurring excessive costs for legal services.

If the template doesn’t match your expectations, start the search again using the search bar at the top.

Select the subscription that best meets your requirements and proceed to payment. Choose the format in which you prefer to receive your document and download it. Print, complete, and sign it. If you already have an account, you can simply Log In to it, locate the Fulton Irrevocable Trust Funded by Life Insurance template, and download it. To re-download the form, visit the My documents tab. Using our services makes it simple to find and download legal forms. Additionally, the documents we offer are refreshed by legal experts, which enhances your confidence in handling legal matters. Try US Legal Forms today and experience it yourself!

- US Legal Forms provides a vast collection of over 85,000 state-compliant form templates, which include Fulton Irrevocable Trust Funded by Life Insurance and various form packages.

- We offer templates for numerous scenarios: from divorce documents to real estate forms.

- With over 25 years of experience, we have maintained an impeccable reputation among our clients.

- To become one of our satisfied customers and acquire the necessary document without unnecessary difficulties, follow these steps.

- First, verify that the Fulton Irrevocable Trust Funded by Life Insurance complies with your state's or county's regulations.

- If the document contains a description, ensure you understand its purpose.

Form popularity

FAQ

Steps for establishing a life insurance trust for your children Hire an estates attorney. Connect your accountant and financial planner with your estates attorney to address any tax implications. Select a trustee and backup trustee. Change beneficiaries on your life insurance policies to your child's trust.

For those using life insurance to fund a trust, be sure you have made that clear via beneficiary designations. If the parents pass away, the life insurance policies would pay out to the trust. The designated trustee would then manage the trust assets on behalf of the minor children.

At the time of your death, the death benefit is paid directly to this account. Then, you'll name the trust as the beneficiary when purchasing a life insurance policy. You can also update an existing policy by changing the beneficiary to a trust.

Trusts are not considered individuals; therefore, life insurance proceeds paid to trusts are generally subjected to estate tax. Also, the proceeds payable to a trust may not qualify for the inheritance tax exemption provided by some states for insurance payable to a named beneficiary.

An ILIT is an irrevocable trust that you create to hold a life insurance policy on your life. It is typically used to benefit your spouse and your children by holding the policy proceeds in trust after your death. The main reason people create an ILIT is for estate tax savings.

The trust, upon the grantor's request, buys a life insurance policy on the life of the grantor. The trust is the owner and the beneficiary of the policy. The proceeds of the life insurance policy will be paid to the trust as beneficiary to be distributed in accordance with the trust agreement.

For those using life insurance to fund a trust, be sure you have made that clear via beneficiary designations. If the parents pass away, the life insurance policies would pay out to the trust. The designated trustee would then manage the trust assets on behalf of the minor children.

In order to transfer your policy to a trust for estate tax purposes, you must create an irrevocable life insurance trust and then place the policy inside of the trust. After you transfer the policy, you are no longer the policy owner and the policy benefits will not be included in your estate.

Proceeds of a death benefit payout will not be included as part of your taxable estate if a trust, not an individual owns the policy. For most people without high net worths, naming beneficiaries individually on life insurance policies makes more sense than opening a trust.