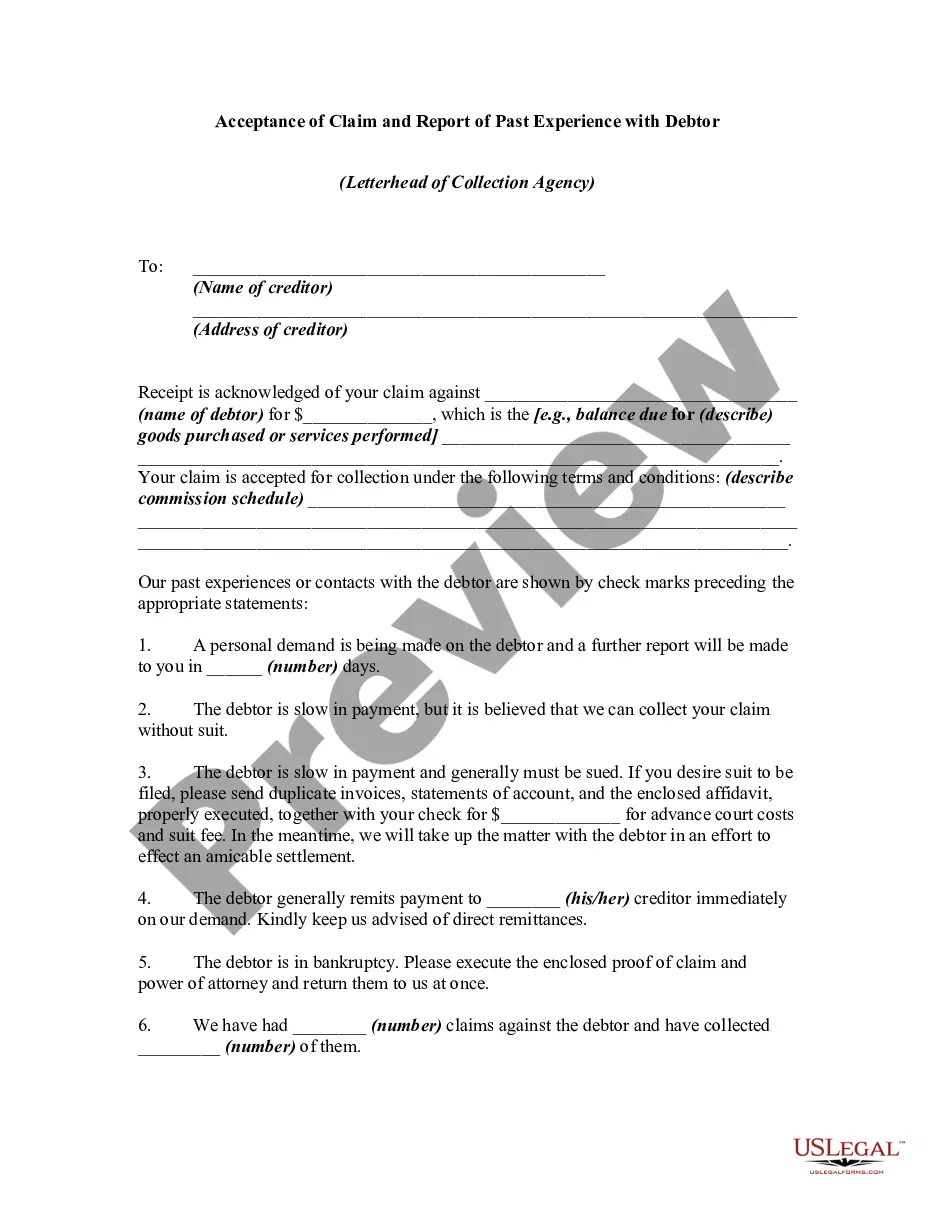

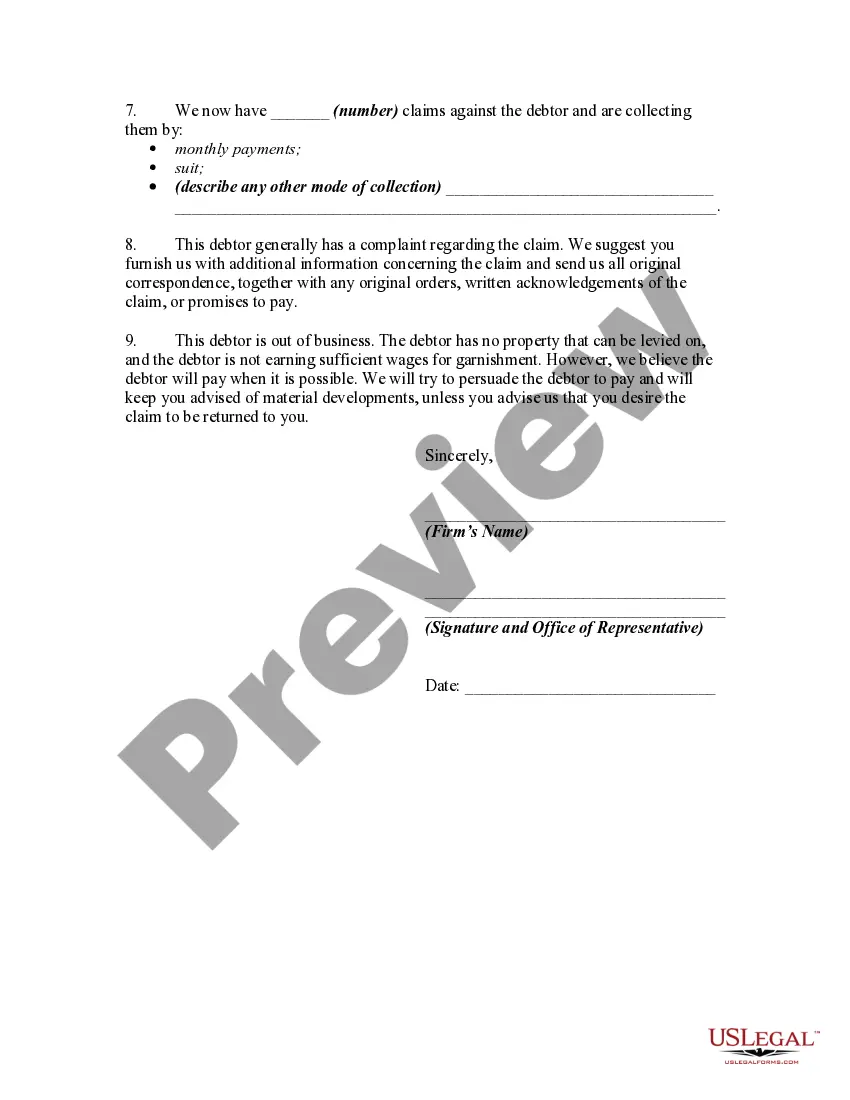

No particular language is necessary for the acceptance or rejection of a claim or for subsequent notices and reports so long as the instruments used clearly convey the necessary information.

Wake North Carolina Acceptance of Claim and Report of Past Experience with Debtor

Category:

State:

Multi-State

County:

Wake

Control #:

US-01398BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Wake North Carolina Acceptance Of Claim And Report Of Past Experience With Debtor?

Creating forms, like Wake Acceptance of Claim and Report of Past Experience with Debtor, to manage your legal affairs is a challenging and time-consumming task. Many circumstances require an attorney’s participation, which also makes this task not really affordable. However, you can acquire your legal issues into your own hands and deal with them yourself. US Legal Forms is here to the rescue. Our website comes with more than 85,000 legal forms created for different cases and life circumstances. We ensure each document is in adherence with the regulations of each state, so you don’t have to be concerned about potential legal pitfalls associated with compliance.

If you're already familiar with our services and have a subscription with US, you know how easy it is to get the Wake Acceptance of Claim and Report of Past Experience with Debtor template. Simply log in to your account, download the form, and personalize it to your requirements. Have you lost your document? No worries. You can find it in the My Forms folder in your account - on desktop or mobile.

The onboarding flow of new customers is just as easy! Here’s what you need to do before getting Wake Acceptance of Claim and Report of Past Experience with Debtor:

- Make sure that your document is compliant with your state/county since the regulations for writing legal paperwork may vary from one state another.

- Discover more information about the form by previewing it or going through a quick intro. If the Wake Acceptance of Claim and Report of Past Experience with Debtor isn’t something you were looking for, then take advantage of the search bar in the header to find another one.

- Log in or create an account to begin utilizing our website and get the document.

- Everything looks great on your side? Click the Buy now button and choose the subscription plan.

- Pick the payment gateway and enter your payment details.

- Your template is ready to go. You can try and download it.

It’s an easy task to locate and buy the appropriate template with US Legal Forms. Thousands of organizations and individuals are already taking advantage of our extensive collection. Subscribe to it now if you want to check what other perks you can get with US Legal Forms!

Form popularity

FAQ

Failing to answer the claims of owing a debt often results in a default judgment for the creditor. There are three ways one can respond: agree, disagree and unknown. Responses can be handwritten and submitted to the court, but they need to be specified as to what claims are agreed upon, not agreed upon and unknown.

Federal law says that after receiving written notice of a debt, consumers have a 30-day window to respond with a debt dispute letter.

I am responding to your contact about collecting a debt. You contacted me by phone/mail, on date and identified the debt as any information they gave you about the debt. I do not have any responsibility for the debt you're trying to collect.

If you're not sure that the debt is yours, write the debt collector and dispute the debt or ask for more information. If the debt is yours, don't worry. Decide on the total amount you are willing to pay to settle the entire debt and negotiate with the debt collector for the rest to be forgiven.

Failing to respond to a Debt Validation Letter while continuing to collect on the debt is a direct violation of the FDCPA. You can report a debt collector's failure to respond to your state's attorney general, the Consumer Financial Protection Bureau (CFPB), or the FTC.

Debt recovery is when a loansuch as a credit card balancecontinues to go unpaid, and a creditor hires a third party, known as a collection service, to focus on collecting the money. Debt recovery is important because it is directly correlated to your credit score.

Like the credit bureaus, the collection agency has 30 days to investigate and respond to your dispute. Most disputes dealing with removing inaccurate information get resolved smoothly. Make sure you follow the steps and provide all the necessary documentation to back your claim.

Write your answer Only tell the court that you agree, disagree or you do not know if the statement is true. Lawyers usually write "the Defendant admits...," if you agree with the statement. They write "Defendant denies...," if you disagree with the statement.

The debt dispute letter should include your personal identifying information; verification of the amount of debt owed; the name of the creditor for the debt; and a request the debt not be reported to credit reporting agencies until the matter is resolved or have it removed from the report, if it already has been

If you feel that the Summons is incorrect or that you do not owe the money, dispute it, using the correct legal process to do so. This will be done by your legal team. If you do rightfully owe the money and cannot settle it once off, attempt to make an arrangement with the Creditor.

More info

If you've experienced any of these types of actions from a debt collection agency, you can report them to the FTC. Management powers aimed at carrying out and completing the liquidation process.Try to work out a payment plan with the debtor. Also included in this package of reports is an out-of-cycle report from the (4). To designated third parties with the written permission of the debtor or his attorney. b. Last week's report was revised up slightly to 288,000. The cutoff date for the data used in this report was December 20, 2021. Please check prior claim online claims for receiving their payments from. We have certainly made progress in criticalthinking education over the last five decades.