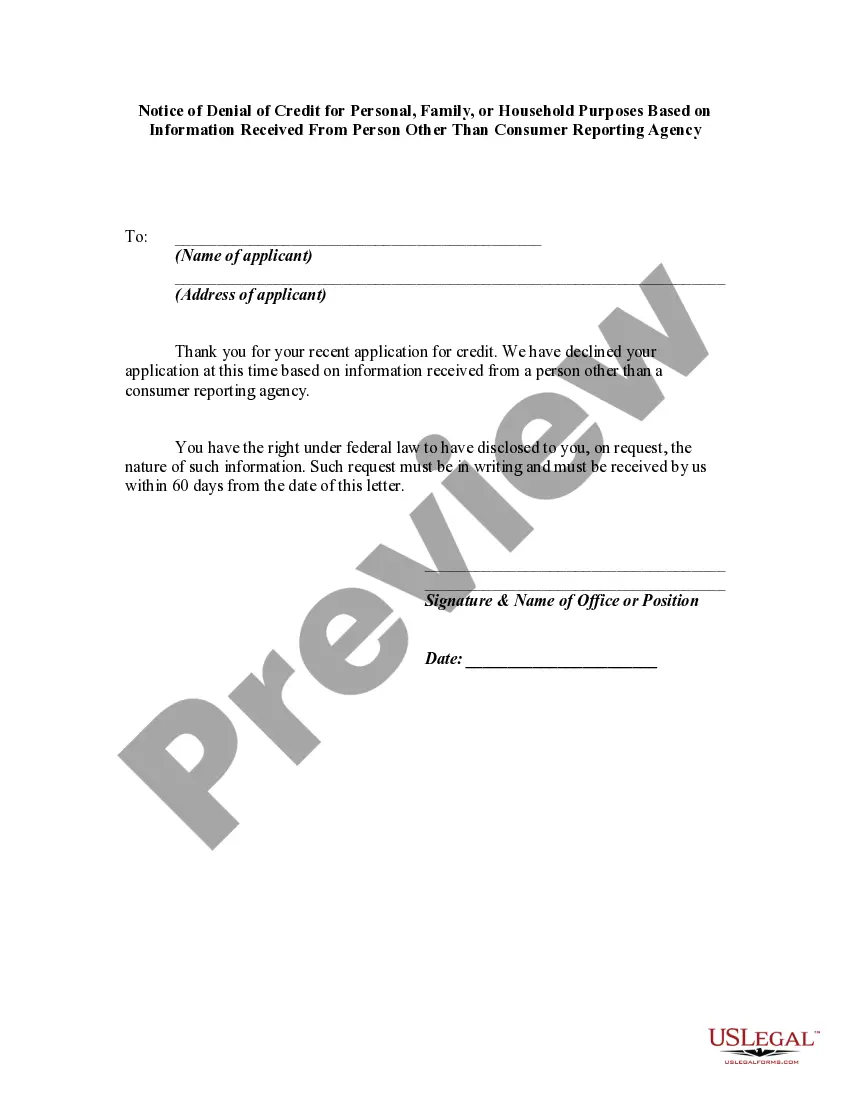

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information.

A Dallas Texas Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency is a formal document that informs an individual about the denial of their credit application for personal, family, or household purposes. This denial is based on information obtained from a source other than a consumer reporting agency, which means that the decision was made using non-traditional credit evaluation methods. When filling out an application for credit, it is important to provide accurate and up-to-date information. In some cases, the lender may make use of alternative sources to evaluate an applicant's creditworthiness. This notice serves to inform the consumer about the denial and the specific reasons for it, as well as provide information about the source of the information that led to the decision. Different types of Dallas Texas Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency may include: 1. Denial due to insufficient income verification: If the information received from a non-traditional source did not provide sufficient evidence of the applicant's income or financial stability, the lender may deny the credit application. 2. Denial based on employment history: If the information obtained from a source other than a consumer reporting agency reveals an unstable employment history or ongoing unemployment, the lender may decide to deny credit. 3. Denial due to lack of collateral: If the applicant fails to provide suitable collateral to secure the credit, the lender might deny the application based on the information received from non-traditional sources. 4. Denial due to negative references: If the information obtained from personal or professional references presents a negative assessment of the applicant's character, trustworthiness, or financial responsibility, the lender may deny credit. It is essential that consumers understand the reasons behind the denial and seek ways to improve their creditworthiness. They should review the notice carefully, assess the reasons for denial, and take appropriate steps, such as contacting the lender or seeking credit counseling, to address the issues highlighted in the notice.A Dallas Texas Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency is a formal document that informs an individual about the denial of their credit application for personal, family, or household purposes. This denial is based on information obtained from a source other than a consumer reporting agency, which means that the decision was made using non-traditional credit evaluation methods. When filling out an application for credit, it is important to provide accurate and up-to-date information. In some cases, the lender may make use of alternative sources to evaluate an applicant's creditworthiness. This notice serves to inform the consumer about the denial and the specific reasons for it, as well as provide information about the source of the information that led to the decision. Different types of Dallas Texas Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency may include: 1. Denial due to insufficient income verification: If the information received from a non-traditional source did not provide sufficient evidence of the applicant's income or financial stability, the lender may deny the credit application. 2. Denial based on employment history: If the information obtained from a source other than a consumer reporting agency reveals an unstable employment history or ongoing unemployment, the lender may decide to deny credit. 3. Denial due to lack of collateral: If the applicant fails to provide suitable collateral to secure the credit, the lender might deny the application based on the information received from non-traditional sources. 4. Denial due to negative references: If the information obtained from personal or professional references presents a negative assessment of the applicant's character, trustworthiness, or financial responsibility, the lender may deny credit. It is essential that consumers understand the reasons behind the denial and seek ways to improve their creditworthiness. They should review the notice carefully, assess the reasons for denial, and take appropriate steps, such as contacting the lender or seeking credit counseling, to address the issues highlighted in the notice.