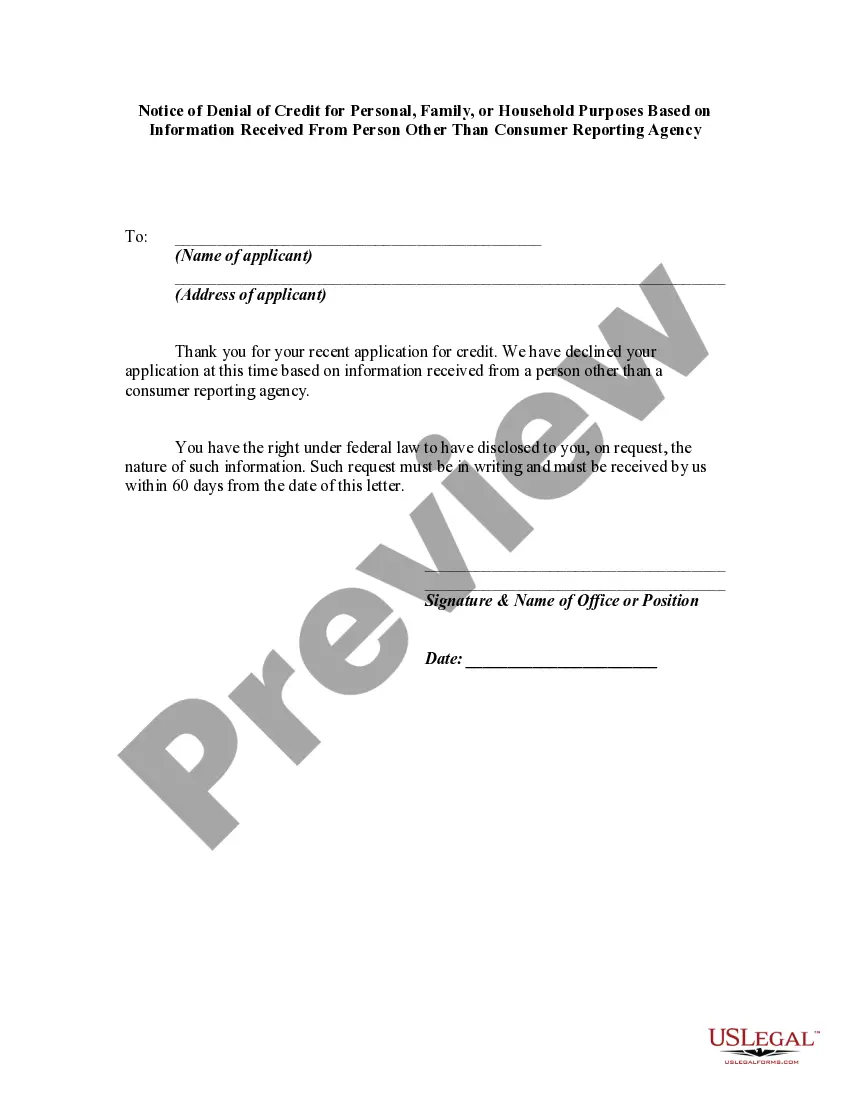

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information.

Philadelphia, Pennsylvania is a vibrant and historic city located in the northeastern part of the United States. With a rich cultural heritage and diverse population, Philadelphia is known for its iconic landmarks, like the Liberty Bell and Independence Hall, which played pivotal roles in American history. The city offers a wide range of attractions, including world-class museums like the Philadelphia Museum of Art and the Franklin Institute, as well as an array of delicious culinary experiences, from cheese steaks to craft beer. In the context of a Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency, Philadelphia residents may encounter various types of notices. These can include: 1. Notice of Denial of Credit based on income: In some cases, lenders may deny credit applications if the applicant's income does not meet their specific requirements or if the income information provided is deemed insufficient. 2. Notice of Denial of Credit due to credit history: This type of notice may be issued if the applicant has a poor credit history, indicating previous instances of late payments, defaults, or high levels of debt. This information is often sourced from credit bureaus or consumer reporting agencies. 3. Notice of Denial of Credit related to employment status: Lenders might base their decision on the applicant's employment status, such as being unemployed or having an unstable job history. If the provided information indicates a lack of stability, it could lead to a credit denial. 4. Notice of Denial of Credit due to insufficient collateral: In certain cases, lenders may require collateral as a guarantee for the credit provided. If the applicant fails to present suitable collateral or if the collateral's value is deemed insufficient, the lender may deny the credit application. It is crucial for individuals who receive a Notice of Denial of Credit for Personal, Family, or Household Purposes to carefully review the information provided and understand the specific reasons for the credit denial. In Philadelphia, residents can seek assistance from consumer protection agencies or credit counseling services to get guidance on addressing the issues that led to the denial of credit.Philadelphia, Pennsylvania is a vibrant and historic city located in the northeastern part of the United States. With a rich cultural heritage and diverse population, Philadelphia is known for its iconic landmarks, like the Liberty Bell and Independence Hall, which played pivotal roles in American history. The city offers a wide range of attractions, including world-class museums like the Philadelphia Museum of Art and the Franklin Institute, as well as an array of delicious culinary experiences, from cheese steaks to craft beer. In the context of a Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency, Philadelphia residents may encounter various types of notices. These can include: 1. Notice of Denial of Credit based on income: In some cases, lenders may deny credit applications if the applicant's income does not meet their specific requirements or if the income information provided is deemed insufficient. 2. Notice of Denial of Credit due to credit history: This type of notice may be issued if the applicant has a poor credit history, indicating previous instances of late payments, defaults, or high levels of debt. This information is often sourced from credit bureaus or consumer reporting agencies. 3. Notice of Denial of Credit related to employment status: Lenders might base their decision on the applicant's employment status, such as being unemployed or having an unstable job history. If the provided information indicates a lack of stability, it could lead to a credit denial. 4. Notice of Denial of Credit due to insufficient collateral: In certain cases, lenders may require collateral as a guarantee for the credit provided. If the applicant fails to present suitable collateral or if the collateral's value is deemed insufficient, the lender may deny the credit application. It is crucial for individuals who receive a Notice of Denial of Credit for Personal, Family, or Household Purposes to carefully review the information provided and understand the specific reasons for the credit denial. In Philadelphia, residents can seek assistance from consumer protection agencies or credit counseling services to get guidance on addressing the issues that led to the denial of credit.