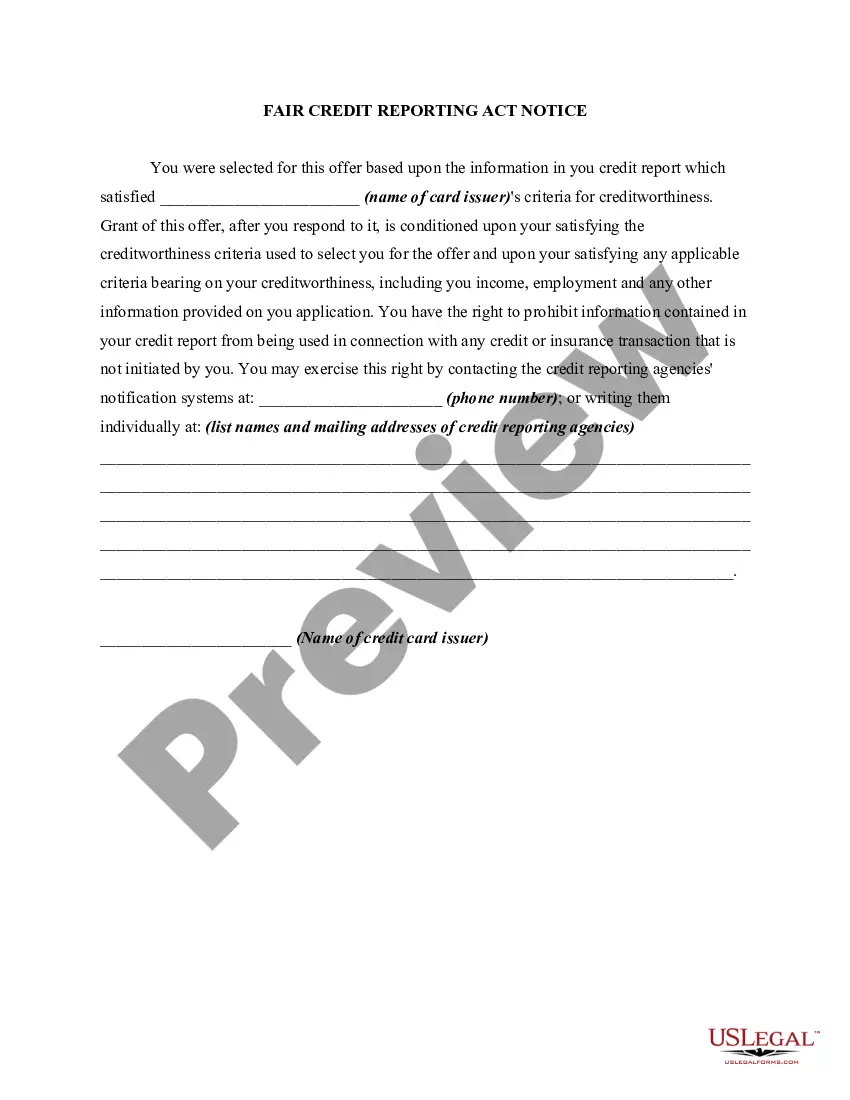

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information. If such a request is made and is received within 60 days after the consumer learned of the adverse action, the user, within a reasonable period of time, must disclose to the consumer the nature of the information.

Phoenix Arizona Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency

Description

How to fill out Notice Of Increase In Charge For Credit Based On Information Received From Person Other Than Consumer Reporting Agency?

What is the typical duration it takes you to draft a legal document.

Since each state has its own laws and regulations pertaining to all aspects of life, finding a Phoenix Notice of Increase in Charge for Credit Derived From Information Obtained From Sources Other Than Consumer Reporting Agencies that meets all local criteria can be daunting, and procuring it from a qualified attorney can often be expensive.

Many online platforms provide the most frequently needed state-specific documents for download, but utilizing the US Legal Forms repository is the most beneficial.

Choose the subscription plan that best meets your needs. Enroll for an account on the platform or Log In to continue to the payment options. Make payment via PayPal or your credit card. Adjust the file format if necessary. Click Download to retain the Phoenix Notice of Increase in Charge for Credit Derived From Information Obtained From Sources Other Than Consumer Reporting Agencies. Print the document or utilize any chosen online editor to complete it digitally. Regardless of how many times you require the purchased template, all samples you have ever saved can be accessed in your profile by clicking the My documents tab. Give it a try!

- US Legal Forms represents the most extensive online database of forms, organized by states and areas of application.

- In addition to the Phoenix Notice of Increase in Charge for Credit Derived From Information Obtained From Sources Other Than Consumer Reporting Agencies, you can discover any particular document to manage your business or personal matters, adhering to your local regulations.

- Experts verify all templates for their legitimacy, ensuring that you can complete your documentation accurately.

- Utilizing the service is incredibly straightforward.

- If you already hold an account on the platform and your subscription is current, you merely need to sign in, select the required template, and download it.

- You can store the file in your account at any later time.

- If you are a newcomer to the website, there will be additional steps to follow before obtaining your Phoenix Notice of Increase in Charge for Credit Derived From Information Obtained From Sources Other Than Consumer Reporting Agencies.

- Review the content of the page you’re visiting.

- Examine the description of the template or Preview it (if available).

- Search for another form using the corresponding option in the header.

- Click Buy Now once you are confident in your selection.

Form popularity

FAQ

Either a statement of the specific reasons for the action taken or a disclosure of the applicant's right to a statement of specific reasons and the name, address, and telephone number of the person or office from which this information can be obtained.

The notice described in paragraph (e)(1)(ii) of this section must be provided to the consumer as soon as reasonably practicable after the credit score has been obtained, but in any event at or before consummation in the case of closed-end credit or before the first transaction is made under an open-end credit plan.

The Fair Credit Reporting Act (FCRA) requires you to obtain a signed background check disclosure and provide adverse action notices.

Risk-based pricing occurs when lenders offer different interest rates and loan terms to borrowers, based on individual creditworthiness. The Risk-Based Pricing Rule requires you to notify consumers if they are getting worse terms because of information in their credit report.

Two federal laws ? the Equal Credit Opportunity Act (ECOA), as implemented by Regulation B, and the Fair Credit Reporting Act (FCRA) ? reflect Congress's determination that consumers and businesses applying for credit should receive notice of the reasons a creditor took adverse action on the application or on an

Application for Specific Terms: In short, when a consumer receives terms they applied for, the risk-based-pricing notice is not required. Adverse Action Notice: If an adverse action notice containing FCRA information is provided to a customer, a risk-based pricing notice is not also needed.

An adverse action notice is to inform you that you have been denied credit, employment, insurance, or other benefits based on information in a credit report. The notice should indicate which credit reporting agency was used, and how to contact them.

An adverse action under the ECOA also includes the termination of an existing credit account, a change in terms of a credit account that are not also made to the others in a class of account holders, and the refusal to grant a request for increased credit on an existing account.

Except in certain circumstances, a CRA may charge a fair and reasonable fee, as determined by the Bureau, for providing a consumer's current credit score or the one most recently calculated for an extension of credit.

A creditor must notify the applicant of adverse action within: 30 days after receiving a complete credit application. 30 days after receiving an incomplete credit application. 30 days after taking action on an existing credit account.