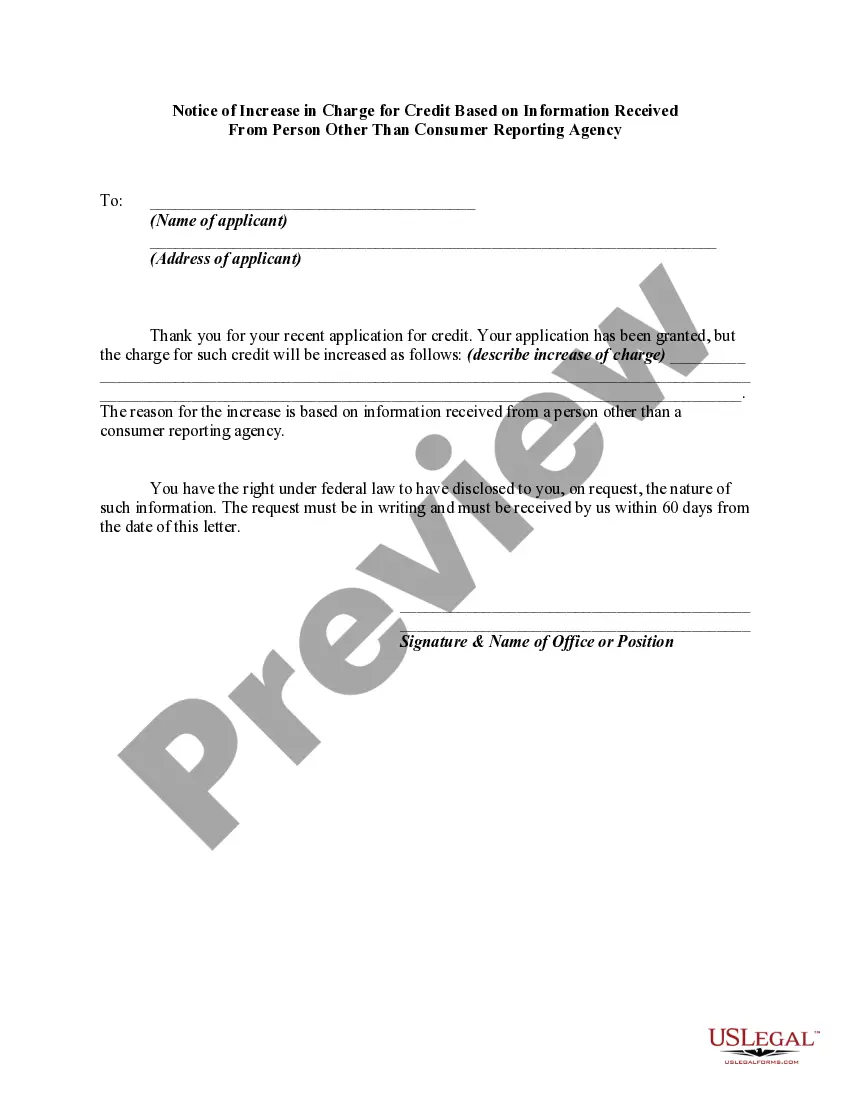

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information. If such a request is made and is received within 60 days after the consumer learned of the adverse action, the user, within a reasonable period of time, must disclose to the consumer the nature of the information.

Title: San Antonio, Texas Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency Introduction: In San Antonio, Texas, there are various instances where individuals may receive a Notice of Increase in charge of Credit based on information received from a person other than a consumer reporting agency. This important notice serves to inform individuals about changes in financial charges, which may impact their credit terms, obligations, and repayment plans. In this article, we will provide a detailed description of what San Antonio's Notice of Increase in charge of Credit entails, its significance, and address different scenarios that may warrant such notice. 1. Understanding San Antonio's Notice of Increase in charge of Credit: The Notice of Increase in charge of Credit is a legal notice provided by a creditor to a consumer, informing them of changes in the terms of their credit agreement. It involves increasing the charges related to credit, such as interest rates, fees, or other charges, based on information received from a person other than a consumer reporting agency. The notice serves to maintain transparency between the creditor and the consumer while complying with relevant federal and state regulations. 2. Types of San Antonio Notice of Increase in charge of Credit: a. Interest Rate Increase: If a creditor receives new information indicating an increased risk associated with a consumer's creditworthiness, they may increase the interest rate applied to the outstanding balance. b. Fee Adjustment: Creditors may adjust various fees related to credit, such as annual fees, late payment fees, over-limit fees, or balance transfer fees, based on information determining the consumer's risk profile. c. Credit Limit Reduction: In some cases, creditors may lower the consumer's credit limit due to information suggesting a higher default risk, leading to increased charges based on a reduced available credit. d. Penalty APR Activation: If the creditor receives information indicating consistent late payments or a decrease in the consumer's creditworthiness, they may activate a higher penalty Annual Percentage Rate (APR) for future transactions. 3. Importance and Impact of the Notice: The Notice of Increase in charge of Credit is crucial as it allows consumers to stay informed about changes in their credit terms promptly. By providing written notice, creditors ensure compliance with state and federal laws, which mandate informing consumers of any changes that affect the charges and obligations associated with their credit accounts. This notice provides consumers with the opportunity to review and assess if the proposed changes align with their financial capabilities and make informed decisions regarding their credit utilization moving forward. Conclusion: San Antonio's Notice of Increase in charge of Credit based on information received from a person other than a consumer reporting agency is a crucial aspect of maintaining transparency and consumer protection within credit agreements. It encompasses various changes in charges, including interest rate adjustments, fee modifications, credit limit reductions, and penalty APR activation. By understanding the significance and implications of such notices, consumers can make well-informed decisions regarding their credit utilization and financial stability.