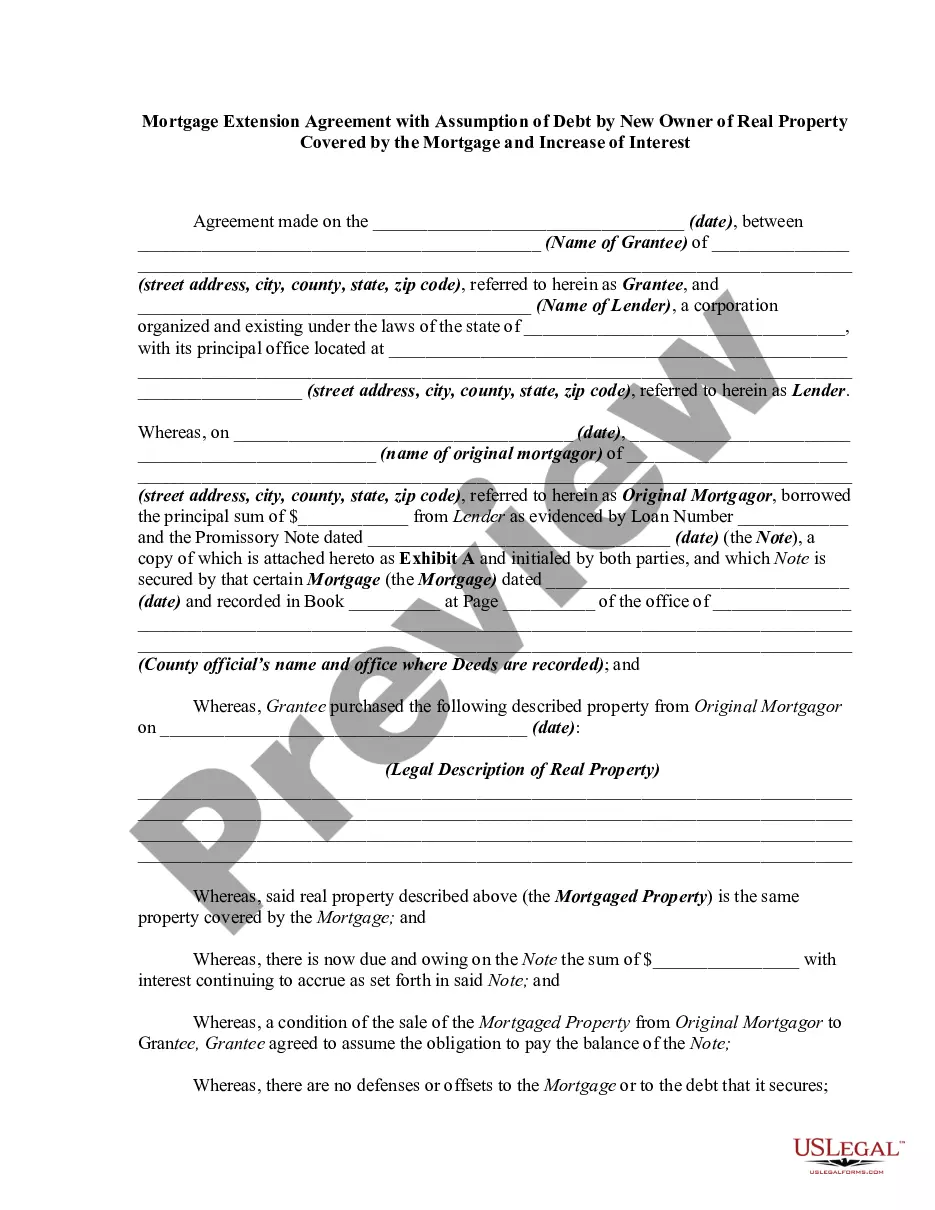

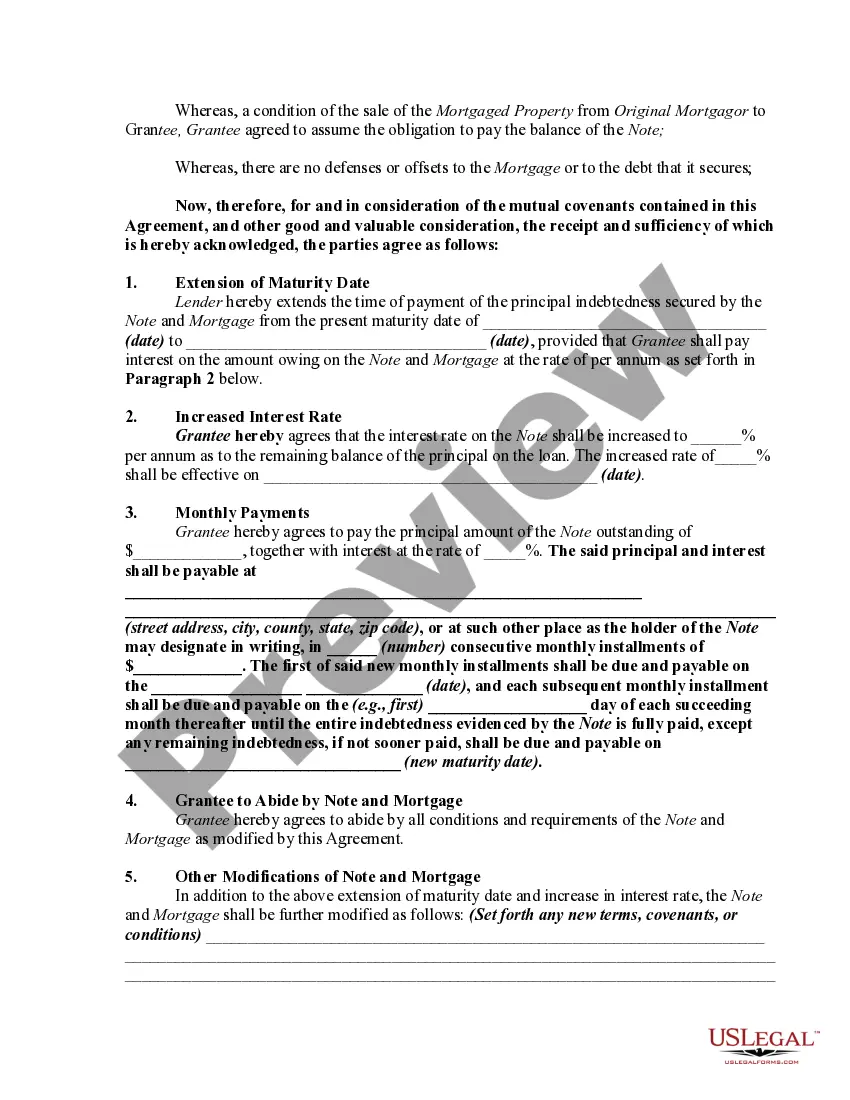

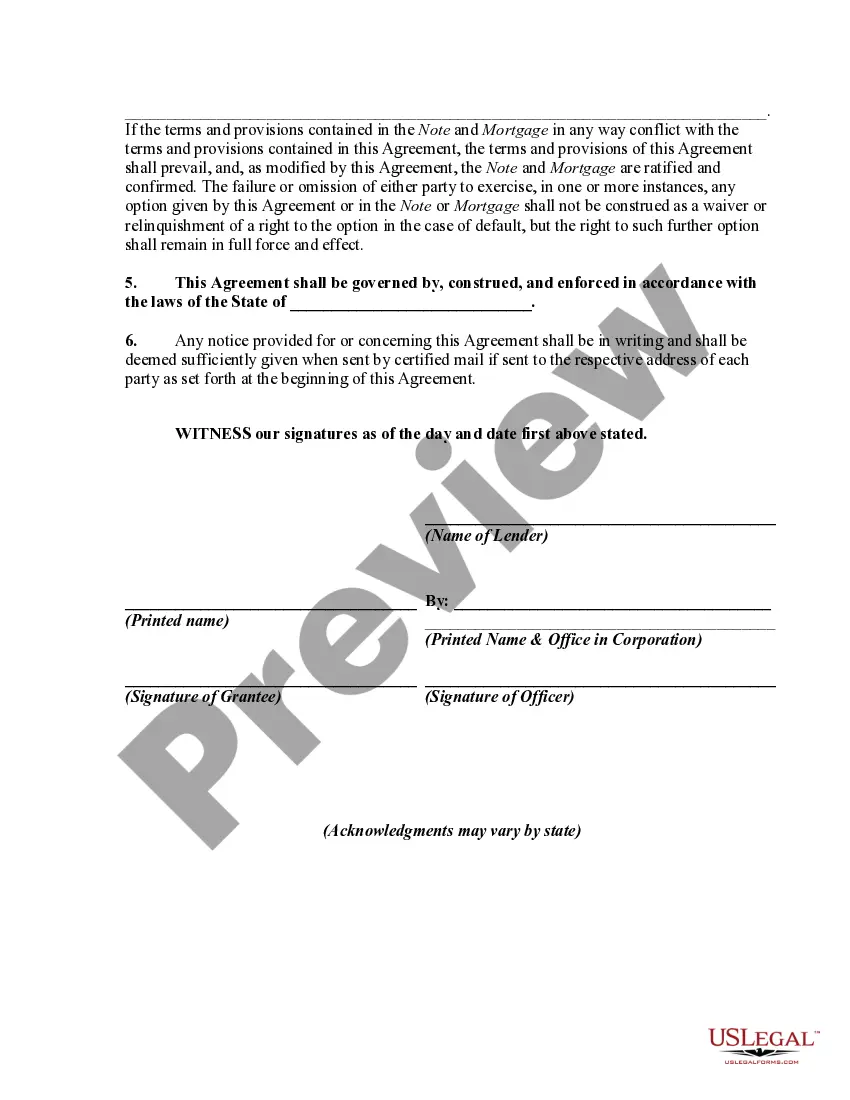

An agreement modifying a loan agreement and mortgage should be signed by both parties to the transaction and recorded in the office of the register of deeds and mortgages where the original mortgage was recorded. Such a modification or extension is contractual in nature and must be supported by consideration. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

A Wake North Carolina Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest is a legally binding agreement that allows a new owner of real property in Wake County, North Carolina, to assume the existing mortgage debt on that property while also increasing the interest rate on the loan. This type of agreement may be necessary when a property is being sold and the new owner wants to take over the existing mortgage, but the lender requires a higher interest rate. The agreement typically includes the following elements: 1. Parties Involved: The agreement identifies the original mortgage lender, the current owner of the property, and the new owner who will assume the mortgage debt. 2. Property Details: The agreement provides a detailed description of the real property that is subject to the mortgage, including its address, legal description, and any relevant identification numbers. 3. Assumption of Debt: The agreement outlines the terms and conditions under which the new owner will assume the mortgage debt, including the outstanding principal amount, interest rate, payment schedule, and any applicable fees or penalties. 4. Mortgage Extension: If the existing mortgage is nearing its maturity date, the agreement may address a mortgage extension, allowing the new owner to extend the loan term. This provision helps ensure that the debt can be repaid over a longer period while providing the lender with an increased interest rate. 5. Escrow Account: The agreement may require the new owner to establish an escrow account for the payment of property taxes, insurance, and other related expenses to protect the lender's interest in the property. 6. Increase of Interest: The agreement specifies the increased interest rate that will be applied to the assumed mortgage debt. This increased rate compensates the lender for taking on additional risk by allowing a new owner to assume the debt. 7. Default and Remedies: The agreement outlines the consequences if either party fails to fulfill their obligations, including default remedies such as foreclosure or other legal actions. Different variations or types of Wake North Carolina Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest may exist depending on the specific terms agreed upon by the parties involved. Some possible variations may include agreements with adjustable interest rates, agreements with balloon payments, or agreements with specific provisions related to refinancing options. Keywords: Wake North Carolina, mortgage extension agreement, assumption of debt, new owner, real property, covered by the mortgage, increase of interest, mortgage lender, payment schedule, escrow account, default remedies, adjustable interest rates, balloon payments, refinancing options.A Wake North Carolina Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest is a legally binding agreement that allows a new owner of real property in Wake County, North Carolina, to assume the existing mortgage debt on that property while also increasing the interest rate on the loan. This type of agreement may be necessary when a property is being sold and the new owner wants to take over the existing mortgage, but the lender requires a higher interest rate. The agreement typically includes the following elements: 1. Parties Involved: The agreement identifies the original mortgage lender, the current owner of the property, and the new owner who will assume the mortgage debt. 2. Property Details: The agreement provides a detailed description of the real property that is subject to the mortgage, including its address, legal description, and any relevant identification numbers. 3. Assumption of Debt: The agreement outlines the terms and conditions under which the new owner will assume the mortgage debt, including the outstanding principal amount, interest rate, payment schedule, and any applicable fees or penalties. 4. Mortgage Extension: If the existing mortgage is nearing its maturity date, the agreement may address a mortgage extension, allowing the new owner to extend the loan term. This provision helps ensure that the debt can be repaid over a longer period while providing the lender with an increased interest rate. 5. Escrow Account: The agreement may require the new owner to establish an escrow account for the payment of property taxes, insurance, and other related expenses to protect the lender's interest in the property. 6. Increase of Interest: The agreement specifies the increased interest rate that will be applied to the assumed mortgage debt. This increased rate compensates the lender for taking on additional risk by allowing a new owner to assume the debt. 7. Default and Remedies: The agreement outlines the consequences if either party fails to fulfill their obligations, including default remedies such as foreclosure or other legal actions. Different variations or types of Wake North Carolina Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest may exist depending on the specific terms agreed upon by the parties involved. Some possible variations may include agreements with adjustable interest rates, agreements with balloon payments, or agreements with specific provisions related to refinancing options. Keywords: Wake North Carolina, mortgage extension agreement, assumption of debt, new owner, real property, covered by the mortgage, increase of interest, mortgage lender, payment schedule, escrow account, default remedies, adjustable interest rates, balloon payments, refinancing options.