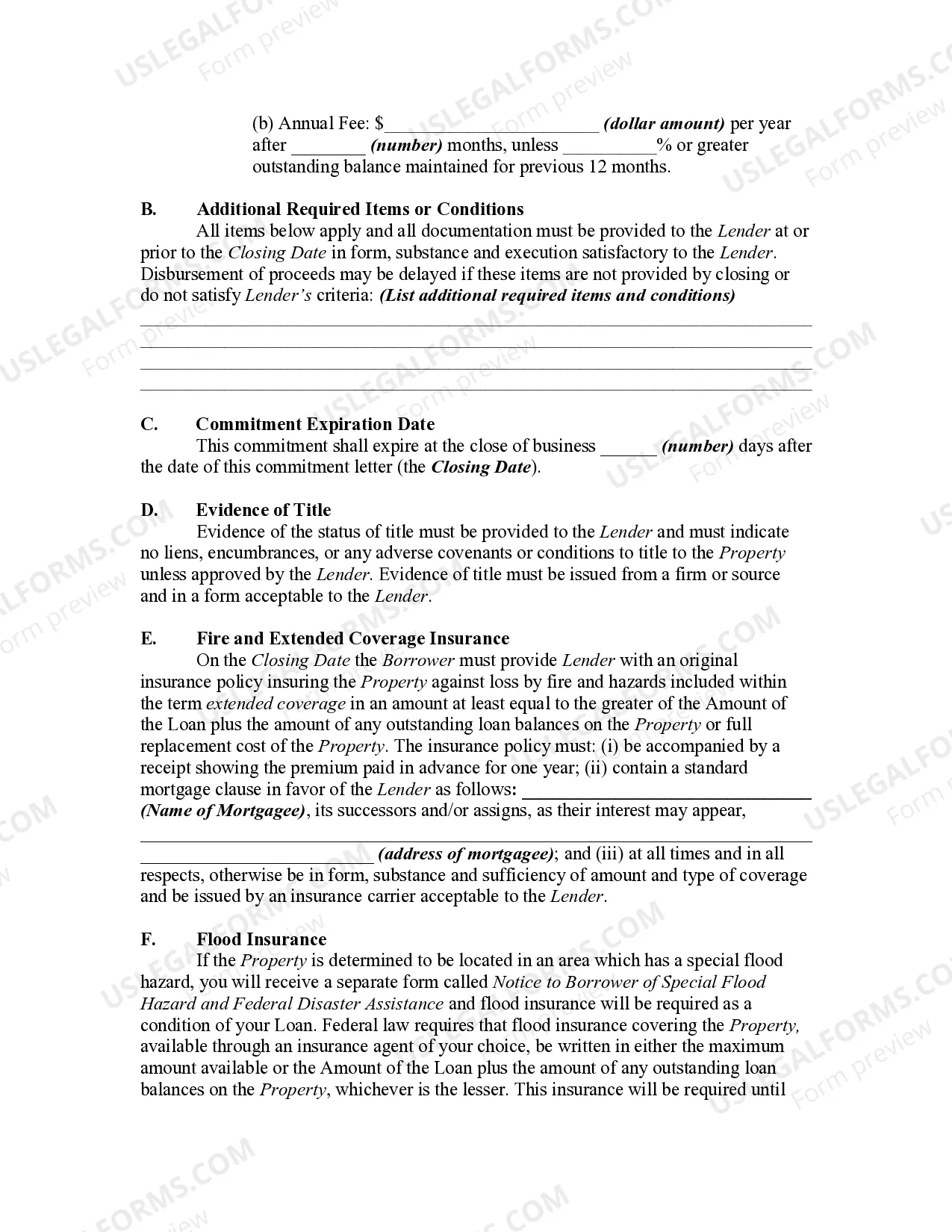

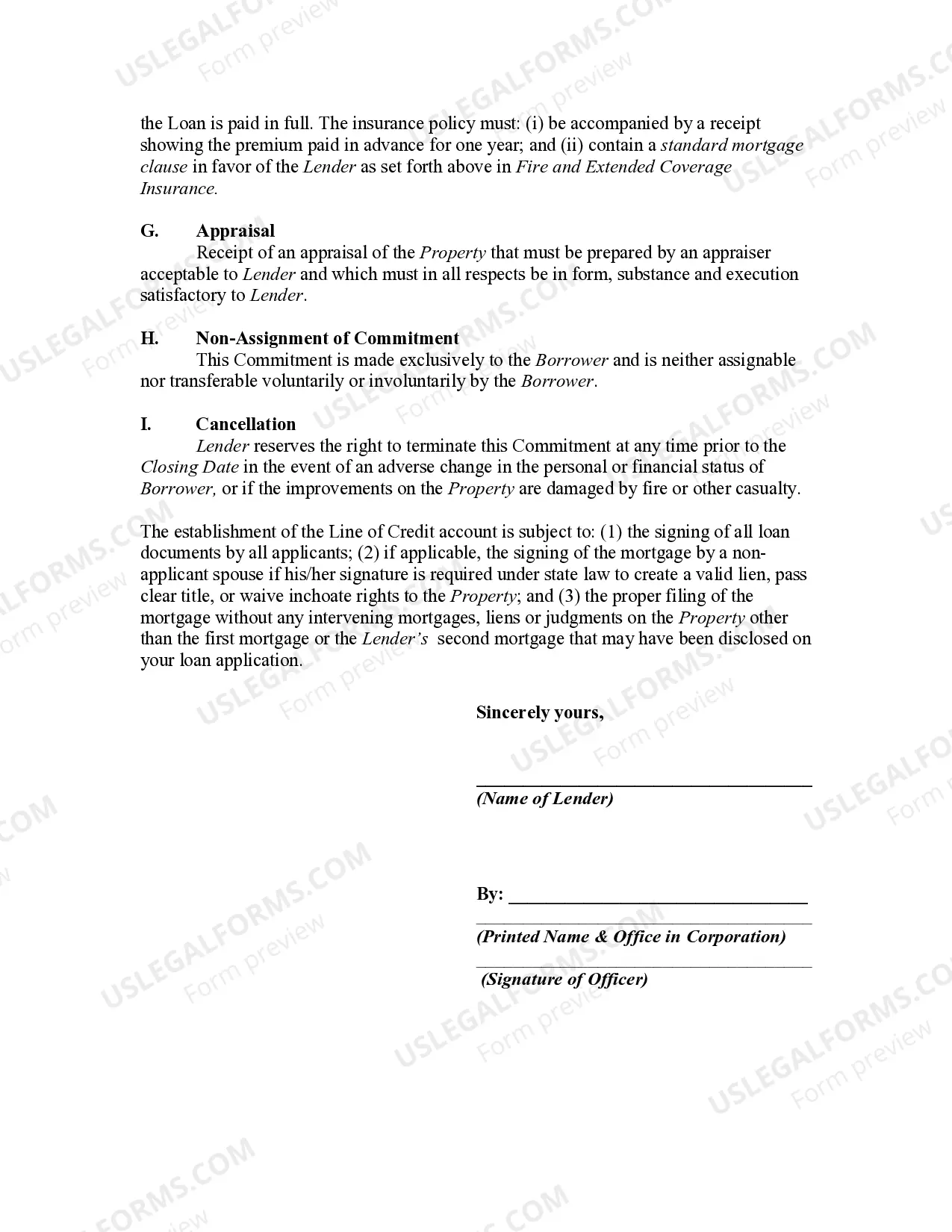

A home equity line of credit is a form of revolving credit in which your home serves as collateral. Because the home is likely to be a consumer's largest asset, many homeowners use their credit lines only for major items such as education, home improvements, or medical bills and not for day-to-day expenses. A home equity line of credit differs from a conventional home equity loan in that the borrower is not advanced the entire sum up front, but uses a line of credit to borrow sums that total no more than the amount, similar to a credit card.

Another important difference from a conventional loan is that the interest rate on a home equity line of credit is variable based on an index such as prime rate. This means that the interest rate can - and almost certainly will - change over time. The margin is the difference between the prime rate and the interest rate the borrower will actually pay.

Queens New York Mortgage Loan Commitment for Home Equity Line of Credit: A Comprehensive Guide Are you a homeowner in Queens, New York, looking for financial flexibility? If so, a Mortgage Loan Commitment for Home Equity Line of Credit (HELOT) might be the perfect solution for you. A HELOT allows homeowners to utilize the equity in their property to secure a line of credit that can be accessed as needed, for various financial purposes. In this detailed description, we will explore what a Mortgage Loan Commitment for HELOT entails, its benefits, and the different types available in Queens, New York. What is a Mortgage Loan Commitment for Home Equity Line of Credit? A Mortgage Loan Commitment for Home Equity Line of Credit is a financial arrangement provided by lenders in Queens, New York, allowing homeowners to borrow against the equity they have built in their property. It is a flexible form of financing that provides borrowers with access to a predetermined credit limit, from which they can withdraw funds whenever required. The credit limit is typically determined based on a percentage of the appraised value of the property, minus any outstanding mortgages. Benefits of a Mortgage Loan Commitment for Home Equity Line of Credit: 1. Flexibility: Helots offer homeowners the flexibility to borrow funds as needed, rather than receiving a lump-sum amount. This enables borrowers to manage their finances more efficiently, using the line of credit for various purposes such as home renovations, debt consolidation, educational expenses, and more. 2. Lower interest rates: Compared to other forms of credit, such as personal loans or credit cards, Helots generally come with lower interest rates, making them a cost-effective option for homeowners seeking access to funds. 3. Tax deductions: In many cases, the interest paid on a HELOT is tax-deductible, potentially providing homeowners with additional financial advantages. 4. Access to larger credit limits: Since a HELOT is secured by the property's equity, lenders are often willing to provide higher credit limits compared to unsecured loans or credit lines. Types of Mortgage Loan Commitment for Home Equity Line of Credit in Queens, New York: 1. Fixed-Rate HELOT: This type of HELOT offers a fixed interest rate throughout the loan term, providing borrowers with stability and predictability in their monthly payments. 2. Adjustable-Rate HELOT: An adjustable-rate HELOT comes with an interest rate that can change periodically, typically in accordance with market rates. Borrowers may benefit from lower initial rates, but should be prepared for potential rate fluctuations. 3. Interest-Only HELOT: With this type of HELOT, borrowers have the option to pay only the interest on the amount borrowed for a specific period, usually the first several years of the loan term. After the interest-only period ends, the borrower will begin making principal and interest payments. In summary, a Mortgage Loan Commitment for Home Equity Line of Credit can be a valuable financial tool for homeowners in Queens, New York. The flexibility, lower interest rates, and potential tax advantages make Helots an attractive option for those looking to access funds against the equity in their property. Consider discussing your specific financial needs and circumstances with a trusted lender or financial advisor to determine which type of HELOT might be the most suitable for you.Queens New York Mortgage Loan Commitment for Home Equity Line of Credit: A Comprehensive Guide Are you a homeowner in Queens, New York, looking for financial flexibility? If so, a Mortgage Loan Commitment for Home Equity Line of Credit (HELOT) might be the perfect solution for you. A HELOT allows homeowners to utilize the equity in their property to secure a line of credit that can be accessed as needed, for various financial purposes. In this detailed description, we will explore what a Mortgage Loan Commitment for HELOT entails, its benefits, and the different types available in Queens, New York. What is a Mortgage Loan Commitment for Home Equity Line of Credit? A Mortgage Loan Commitment for Home Equity Line of Credit is a financial arrangement provided by lenders in Queens, New York, allowing homeowners to borrow against the equity they have built in their property. It is a flexible form of financing that provides borrowers with access to a predetermined credit limit, from which they can withdraw funds whenever required. The credit limit is typically determined based on a percentage of the appraised value of the property, minus any outstanding mortgages. Benefits of a Mortgage Loan Commitment for Home Equity Line of Credit: 1. Flexibility: Helots offer homeowners the flexibility to borrow funds as needed, rather than receiving a lump-sum amount. This enables borrowers to manage their finances more efficiently, using the line of credit for various purposes such as home renovations, debt consolidation, educational expenses, and more. 2. Lower interest rates: Compared to other forms of credit, such as personal loans or credit cards, Helots generally come with lower interest rates, making them a cost-effective option for homeowners seeking access to funds. 3. Tax deductions: In many cases, the interest paid on a HELOT is tax-deductible, potentially providing homeowners with additional financial advantages. 4. Access to larger credit limits: Since a HELOT is secured by the property's equity, lenders are often willing to provide higher credit limits compared to unsecured loans or credit lines. Types of Mortgage Loan Commitment for Home Equity Line of Credit in Queens, New York: 1. Fixed-Rate HELOT: This type of HELOT offers a fixed interest rate throughout the loan term, providing borrowers with stability and predictability in their monthly payments. 2. Adjustable-Rate HELOT: An adjustable-rate HELOT comes with an interest rate that can change periodically, typically in accordance with market rates. Borrowers may benefit from lower initial rates, but should be prepared for potential rate fluctuations. 3. Interest-Only HELOT: With this type of HELOT, borrowers have the option to pay only the interest on the amount borrowed for a specific period, usually the first several years of the loan term. After the interest-only period ends, the borrower will begin making principal and interest payments. In summary, a Mortgage Loan Commitment for Home Equity Line of Credit can be a valuable financial tool for homeowners in Queens, New York. The flexibility, lower interest rates, and potential tax advantages make Helots an attractive option for those looking to access funds against the equity in their property. Consider discussing your specific financial needs and circumstances with a trusted lender or financial advisor to determine which type of HELOT might be the most suitable for you.