A home equity line of credit is a form of revolving credit in which your home serves as collateral. Because the home is likely to be a consumer's largest asset, many homeowners use their credit lines only for major items such as education, home improvements, or medical bills and not for day-to-day expenses. A home equity line of credit differs from a conventional home equity loan in that the borrower is not advanced the entire sum up front, but uses a line of credit to borrow sums that total no more than the amount, similar to a credit card.

Another important difference from a conventional loan is that the interest rate on a home equity line of credit is variable based on an index such as prime rate. This means that the interest rate can - and almost certainly will - change over time. The margin is the difference between the prime rate and the interest rate the borrower will actually pay.

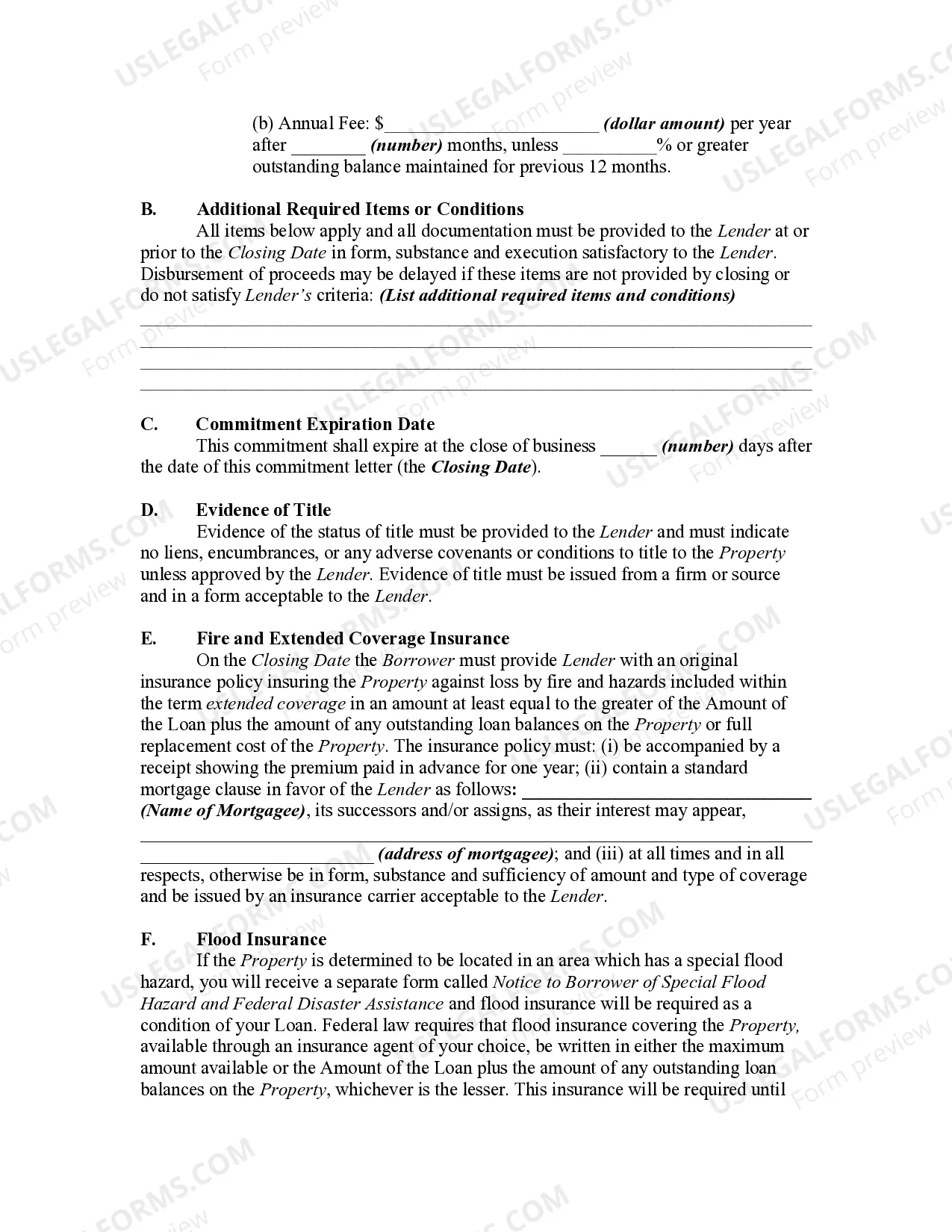

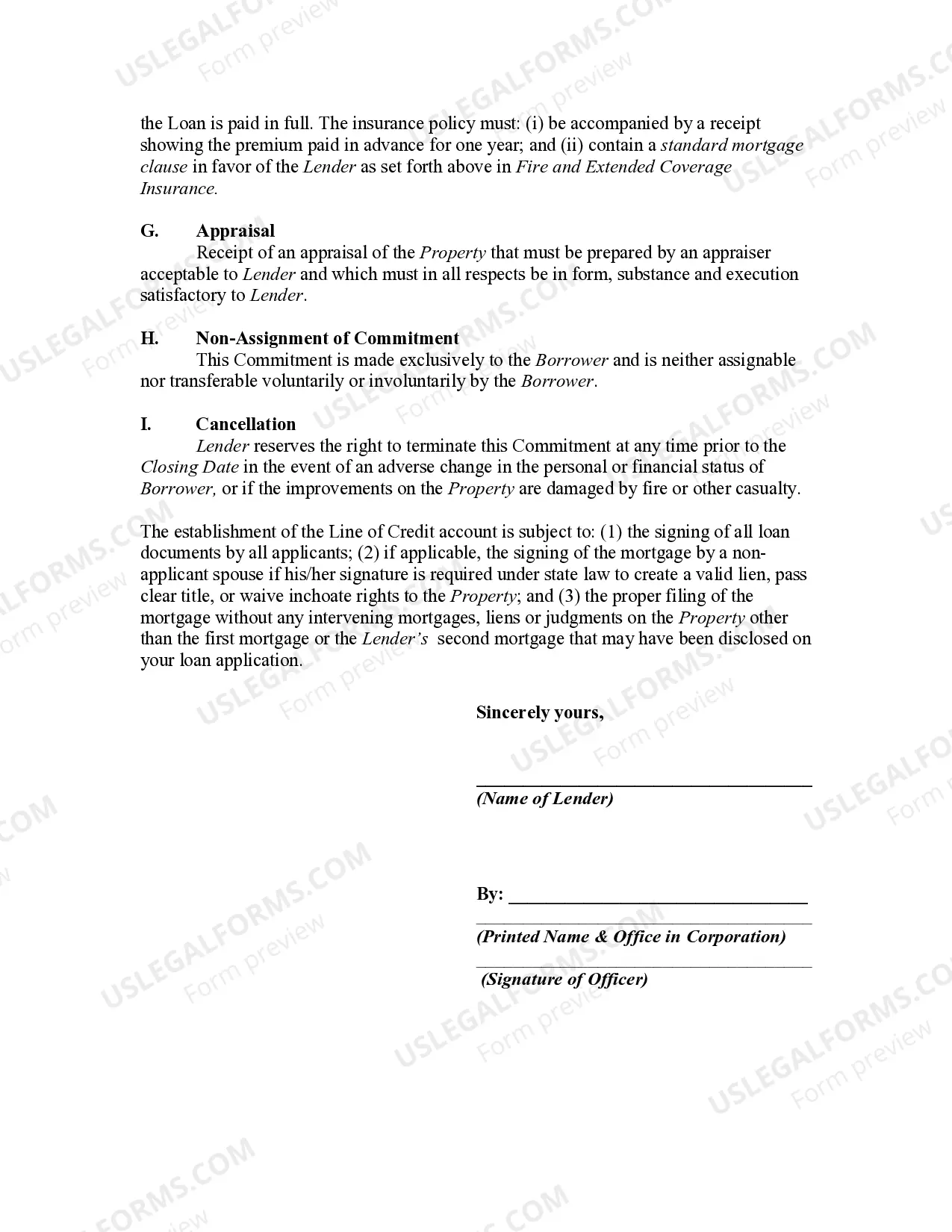

A San Diego California Mortgage Loan Commitment for Home Equity Line of Credit (HELOT) is a legal agreement between a borrower and a lender, specifically for homeowners in the San Diego area, looking to access the equity in their homes for various financial needs. This commitment entails a line of credit that is secured by the borrower's primary residence and allows them to borrow funds up to a predetermined limit using their home's value as collateral. A Mortgage Loan Commitment for HELOT in San Diego comes with specific terms and conditions that determine the borrower's access to funds, repayment schedule, and the interest rates applicable. It is essential to understand the various types and features of a Mortgage Loan Commitment for HELOT to make an informed decision. Here are some common types: 1. Traditional HELOT: This type of commitment allows homeowners to access a certain percentage of their home equity, usually up to 85%. The borrower can draw and repay funds multiple times within the specified draw period, typically ranging from 5 to 10 years. During the draw period, interest accrues only on the borrowed amount. 2. Fixed-Rate HELOT: Unlike the traditional HELOT, this commitment offers a fixed interest rate for a specific period, providing stability in monthly payments. It is an excellent option for borrowers who prefer predictable payments, especially when interest rates are expected to rise. 3. Interest-Only HELOT: With an interest-only HELOT, borrowers have the option to pay only the interest accrued on the borrowed amount during the draw period, typically ranging from 10 to 15 years. This commitment allows for lower monthly payments but requires a lump sum payment or refinancing at the end of the draw period. 4. HELOT with Conversion Option: This commitment allows borrowers to convert all or a portion of their variable-rate HELOT balance into a fixed-rate loan with a predetermined term. It provides flexibility to borrowers who anticipate interest rate hikes and would like to secure a fixed rate in the future. When considering a San Diego California Mortgage Loan Commitment for HELOT, it is essential to evaluate the lender's reputation, fees, and interest rates. Additionally, borrowers should understand the risks associated with variable rates, potential fluctuations in property values, and the responsibility for repayment in case of non-compliance with the loan terms. Seeking professional advice from mortgage brokers or financial advisors can further assist borrowers in making the right decision based on their individual financial circumstances and goals.