This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

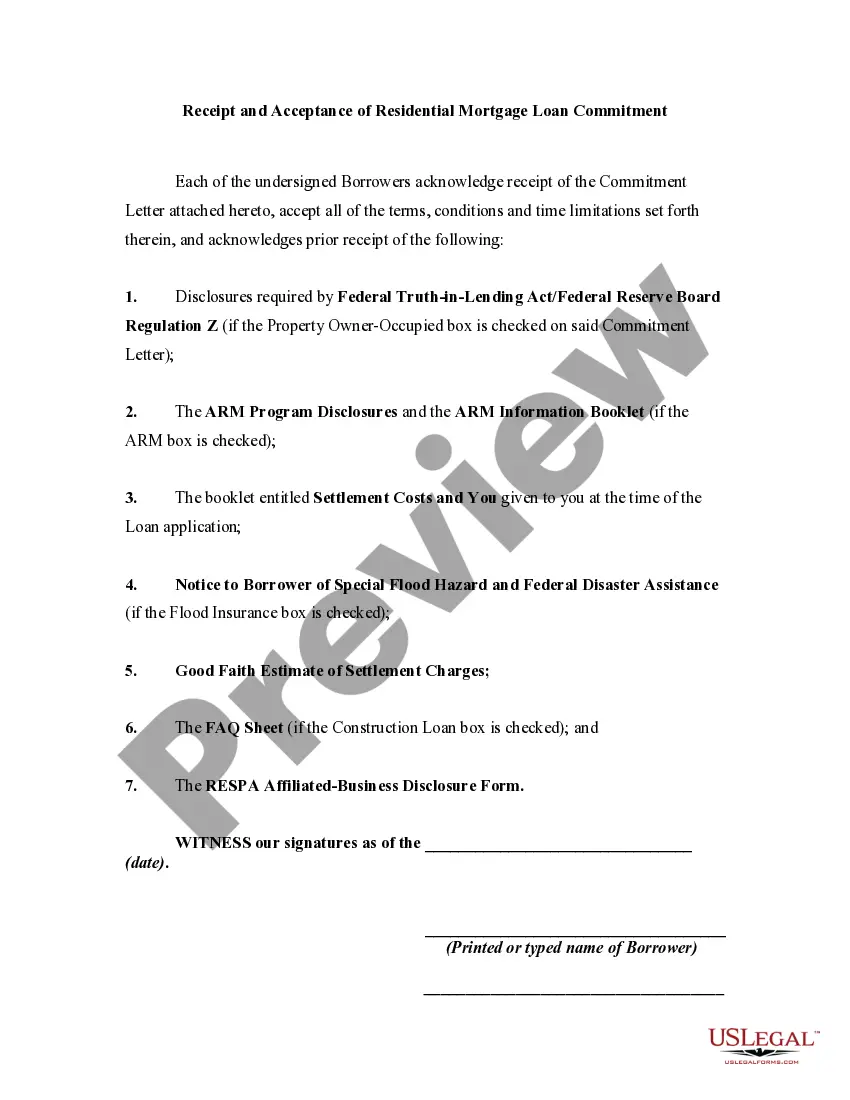

Cook Illinois Receipt and Acceptance of Residential Mortgage Loan Commitment is an important document used in the process of securing a residential mortgage loan in Cook County, Illinois. This document serves as a written agreement between the borrower and the lender, outlining the terms and conditions of the loan commitment. Here we will discuss the contents of this document as well as its significance, types, and other essential details. The Cook Illinois Receipt and Acceptance of Residential Mortgage Loan Commitment typically includes the following key elements: 1. Borrower and Lender Information: This section includes the names, addresses, and contact details of both the borrower and the lender. It may also involve information about the loan officer, loan originator, or mortgage broker involved in the transaction. 2. Property Description: This section provides detailed information about the property being financed, such as its address, legal description, and the type of property (e.g., single-family home, condominium, townhouse). 3. Loan Terms: This section outlines the terms and conditions of the loan commitment, including the loan amount, interest rate, loan term, repayment schedule, and any applicable fees or charges. It may also mention the loan program or type of mortgage, such as conventional, FHA, VA, or USDA. 4. Conditions and Contingencies: This part specifies any conditions or contingencies that must be met by the borrower or the property for the loan commitment to be finalized. These may include requirements related to the borrower's creditworthiness, income verification, property appraisal, title search, and other factors. 5. Lock-In Period: If the borrower has chosen to lock in their interest rate, this section will state the duration of the lock-in period, during which the interest rate will remain unchanged. 6. Expiration Date: The Cook Illinois Receipt and Acceptance of Residential Mortgage Loan Commitment usually includes an expiration date, indicating the latest date by which the borrower must complete the loan closing process. Different types of Cook Illinois Receipt and Acceptance of Residential Mortgage Loan Commitment may exist to cater to specific loan programs or unique circumstances. These variations might include: 1. Conventional Mortgage Loan Commitment: This type of commitment applies to standard mortgage loans that meet the guidelines set by Fannie Mae or Freddie Mac. 2. FHA Mortgage Loan Commitment: This commitment is specific to loans insured by the Federal Housing Administration (FHA), which often provides more flexible qualifying criteria for borrowers. 3. VA Mortgage Loan Commitment: Reserved for eligible veterans, active-duty military personnel, and surviving spouses, this commitment applies to loans guaranteed by the Department of Veterans Affairs (VA). 4. Jumbo Mortgage Loan Commitment: If the loan amount exceeds the conventional loan limits, a jumbo mortgage loan commitment may be required. These commitments have specific terms and criteria for larger loan amounts. The Cook Illinois Receipt and Acceptance of Residential Mortgage Loan Commitment plays a crucial role in the loan process, ensuring that both the borrower and the lender are on the same page regarding the terms of the loan. It acts as a legally binding agreement and provides a framework for a successful mortgage transaction.Cook Illinois Receipt and Acceptance of Residential Mortgage Loan Commitment is an important document used in the process of securing a residential mortgage loan in Cook County, Illinois. This document serves as a written agreement between the borrower and the lender, outlining the terms and conditions of the loan commitment. Here we will discuss the contents of this document as well as its significance, types, and other essential details. The Cook Illinois Receipt and Acceptance of Residential Mortgage Loan Commitment typically includes the following key elements: 1. Borrower and Lender Information: This section includes the names, addresses, and contact details of both the borrower and the lender. It may also involve information about the loan officer, loan originator, or mortgage broker involved in the transaction. 2. Property Description: This section provides detailed information about the property being financed, such as its address, legal description, and the type of property (e.g., single-family home, condominium, townhouse). 3. Loan Terms: This section outlines the terms and conditions of the loan commitment, including the loan amount, interest rate, loan term, repayment schedule, and any applicable fees or charges. It may also mention the loan program or type of mortgage, such as conventional, FHA, VA, or USDA. 4. Conditions and Contingencies: This part specifies any conditions or contingencies that must be met by the borrower or the property for the loan commitment to be finalized. These may include requirements related to the borrower's creditworthiness, income verification, property appraisal, title search, and other factors. 5. Lock-In Period: If the borrower has chosen to lock in their interest rate, this section will state the duration of the lock-in period, during which the interest rate will remain unchanged. 6. Expiration Date: The Cook Illinois Receipt and Acceptance of Residential Mortgage Loan Commitment usually includes an expiration date, indicating the latest date by which the borrower must complete the loan closing process. Different types of Cook Illinois Receipt and Acceptance of Residential Mortgage Loan Commitment may exist to cater to specific loan programs or unique circumstances. These variations might include: 1. Conventional Mortgage Loan Commitment: This type of commitment applies to standard mortgage loans that meet the guidelines set by Fannie Mae or Freddie Mac. 2. FHA Mortgage Loan Commitment: This commitment is specific to loans insured by the Federal Housing Administration (FHA), which often provides more flexible qualifying criteria for borrowers. 3. VA Mortgage Loan Commitment: Reserved for eligible veterans, active-duty military personnel, and surviving spouses, this commitment applies to loans guaranteed by the Department of Veterans Affairs (VA). 4. Jumbo Mortgage Loan Commitment: If the loan amount exceeds the conventional loan limits, a jumbo mortgage loan commitment may be required. These commitments have specific terms and criteria for larger loan amounts. The Cook Illinois Receipt and Acceptance of Residential Mortgage Loan Commitment plays a crucial role in the loan process, ensuring that both the borrower and the lender are on the same page regarding the terms of the loan. It acts as a legally binding agreement and provides a framework for a successful mortgage transaction.