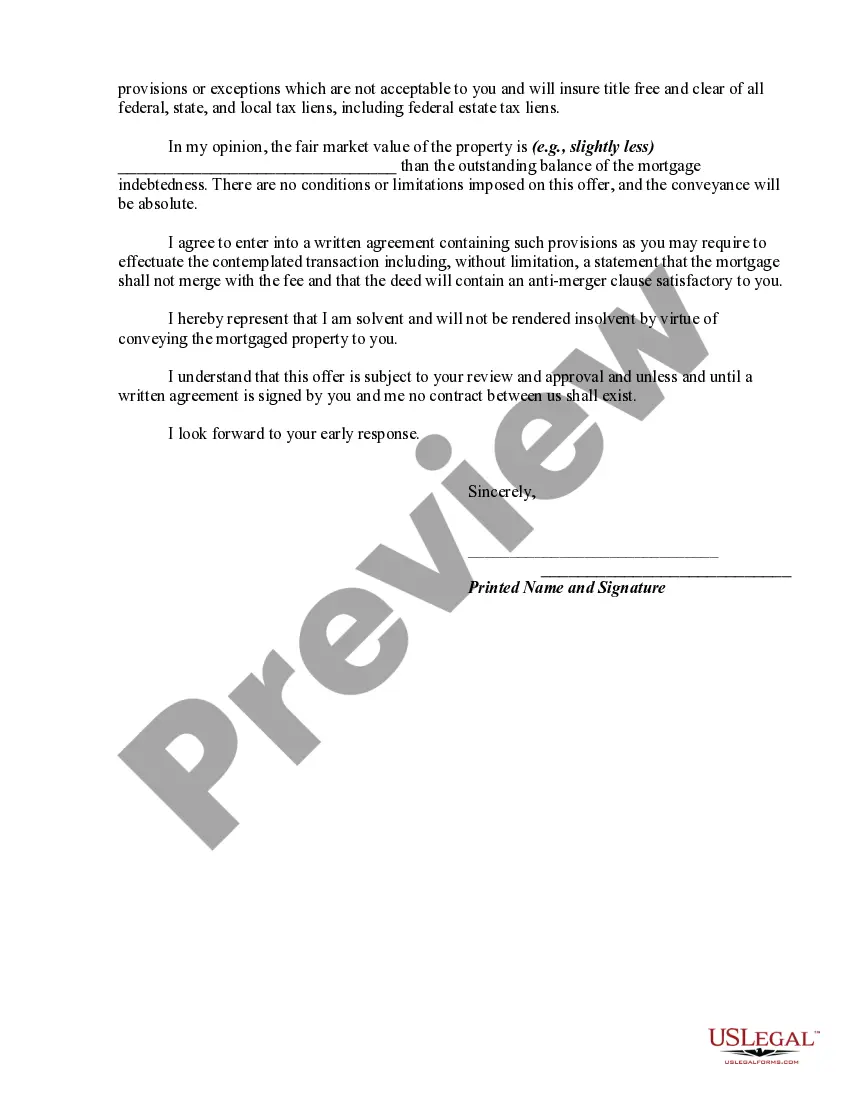

A deed in lieu of foreclosure is a method sometimes used by a lienholder on property to avoid a lengthy and expensive foreclosure process, with a deed in lieu of foreclosure a foreclosing lienholder agrees to have the ownership interest transferred to the bank/lienholder as payment in full. The debtor basically deeds the property to the bank instead of them paying for foreclosure proceedings. Therefore, if a debtor fails to make mortgage payments and the bank is about to foreclose on the property, the deed in lieu of foreclosure is an option that chooses to give the bank ownership of the property rather than having the bank use the legal process of foreclosure.

A borrower of deed in lieu of foreclosure refers to a scenario where a homeowner in Collin, Texas offers their property's deed to the lender as a means of avoiding foreclosure. This alternative option allows the borrower to surrender the property voluntarily to the lender instead of going through the lengthy and potentially damaging process of foreclosure. In Collin, Texas, the offer made by a borrower of deed in lieu of foreclosure comes with several benefits for both parties involved. Firstly, it provides the borrower with an opportunity to mitigate the negative impact on their credit score that foreclosure can bring. Additionally, this arrangement allows the borrower to avoid the potential legal complications and costs associated with formal foreclosure procedures. One type of Collin, Texas offer by a borrower of deed in lieu of foreclosure is a negotiated settlement agreement. In such cases, the borrower and lender work together to agree on the terms and conditions of transferring the property's deed. These negotiations typically involve discussions about any outstanding mortgage debt, potential financial obligations, and the impact on the borrower's credit history. Another type is a financial incentive offer. In this scenario, the lender may offer the borrower a financial incentive, such as a specified sum of money, to encourage them to choose deed in lieu of foreclosure instead of pursuing other options. This incentive can help alleviate some financial burden on the borrower and provide a smoother transition from homeownership to a new living arrangement. It is crucial for borrowers considering a deed in lieu of foreclosure to thoroughly understand the implications and potential consequences of making an offer. Seeking legal and financial advice is highly recommended ensuring that the borrower's interests are protected throughout the process. In conclusion, a Collin, Texas offer by a borrower of deed in lieu of foreclosure is a proactive approach to resolving a difficult financial situation. By voluntarily surrendering the property's deed to the lender, borrowers can avoid the negative repercussions of foreclosure while potentially negotiating more favorable terms. Thorough research and expert guidance are essential when navigating this complex procedure, ensuring the best possible outcome for all parties involved.A borrower of deed in lieu of foreclosure refers to a scenario where a homeowner in Collin, Texas offers their property's deed to the lender as a means of avoiding foreclosure. This alternative option allows the borrower to surrender the property voluntarily to the lender instead of going through the lengthy and potentially damaging process of foreclosure. In Collin, Texas, the offer made by a borrower of deed in lieu of foreclosure comes with several benefits for both parties involved. Firstly, it provides the borrower with an opportunity to mitigate the negative impact on their credit score that foreclosure can bring. Additionally, this arrangement allows the borrower to avoid the potential legal complications and costs associated with formal foreclosure procedures. One type of Collin, Texas offer by a borrower of deed in lieu of foreclosure is a negotiated settlement agreement. In such cases, the borrower and lender work together to agree on the terms and conditions of transferring the property's deed. These negotiations typically involve discussions about any outstanding mortgage debt, potential financial obligations, and the impact on the borrower's credit history. Another type is a financial incentive offer. In this scenario, the lender may offer the borrower a financial incentive, such as a specified sum of money, to encourage them to choose deed in lieu of foreclosure instead of pursuing other options. This incentive can help alleviate some financial burden on the borrower and provide a smoother transition from homeownership to a new living arrangement. It is crucial for borrowers considering a deed in lieu of foreclosure to thoroughly understand the implications and potential consequences of making an offer. Seeking legal and financial advice is highly recommended ensuring that the borrower's interests are protected throughout the process. In conclusion, a Collin, Texas offer by a borrower of deed in lieu of foreclosure is a proactive approach to resolving a difficult financial situation. By voluntarily surrendering the property's deed to the lender, borrowers can avoid the negative repercussions of foreclosure while potentially negotiating more favorable terms. Thorough research and expert guidance are essential when navigating this complex procedure, ensuring the best possible outcome for all parties involved.