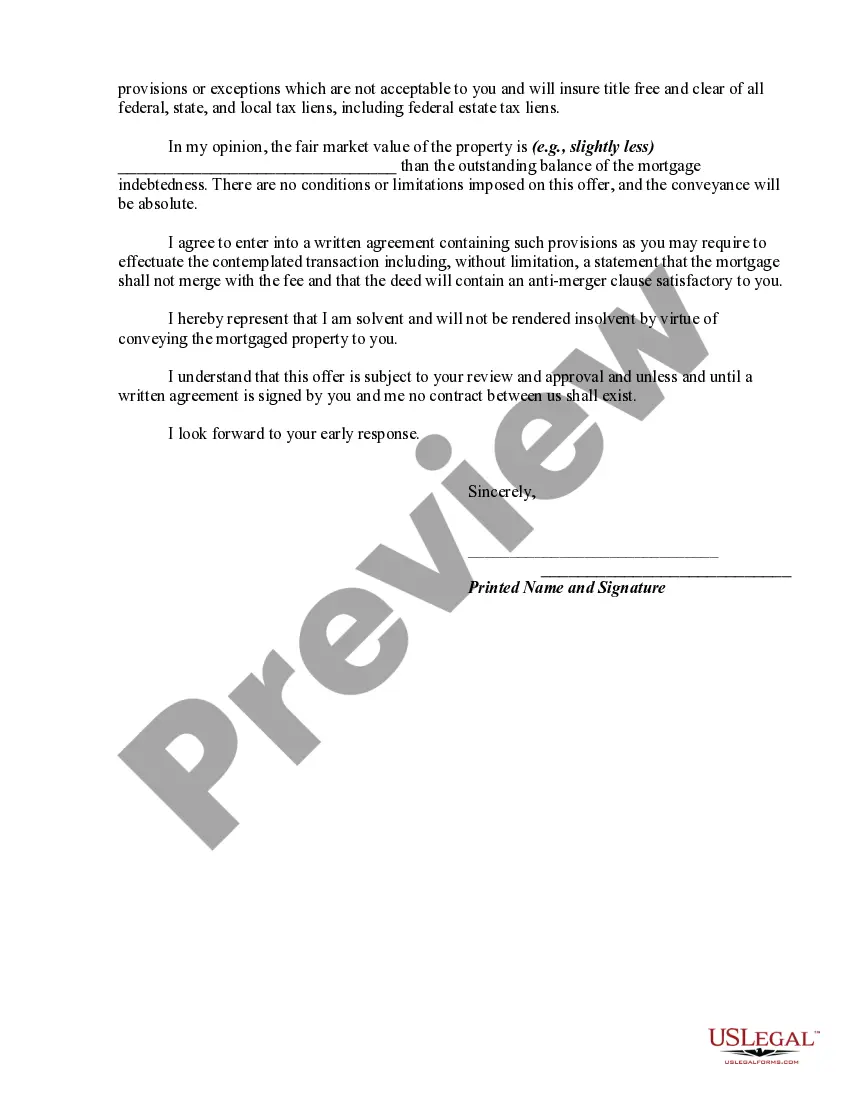

A deed in lieu of foreclosure is a method sometimes used by a lienholder on property to avoid a lengthy and expensive foreclosure process, with a deed in lieu of foreclosure a foreclosing lienholder agrees to have the ownership interest transferred to the bank/lienholder as payment in full. The debtor basically deeds the property to the bank instead of them paying for foreclosure proceedings. Therefore, if a debtor fails to make mortgage payments and the bank is about to foreclose on the property, the deed in lieu of foreclosure is an option that chooses to give the bank ownership of the property rather than having the bank use the legal process of foreclosure.

Cuyahoga County, Ohio, is one of the most populous counties in the state and encompasses a diverse range of communities, including Cleveland, the county seat. In cases where homeowners are facing financial difficulties and are unable to keep up with their mortgage payments, they may consider options like a "Borrower's Deed in Lieu of Foreclosure" to prevent foreclosure. A Borrower's Deed in Lieu of Foreclosure essentially involves the borrower voluntarily deeding their property to the mortgage lender, thereby avoiding the lengthy foreclosure process. This option allows homeowners to avoid the negative consequences associated with foreclosure and potentially negotiate more favorable terms. The Cuyahoga County Clerk of Courts, alongside various financial institutions and legal entities, facilitates the process to ensure transparency and fairness to both borrowers and lenders. The offer made by the borrower in this case is to voluntarily transfer the property back to the lender, releasing them from their mortgage obligation. Different types of Cuyahoga Ohio Offers by Borrower of Deed in Lieu of Foreclosure may include: 1. Standard Deed in Lieu: This is the most common type, where the borrower simply transfers the property back to the lender and walks away from the mortgage obligation. 2. Assumption Deed in Lieu: In this scenario, the lender may allow a third party to assume the mortgage loan and take responsibility for the property, rather than the borrower directly deeding it back. This option can be helpful if there is a qualified buyer available. 3. Negotiated Debt Forgiveness: In some cases, the borrower may negotiate with the lender to have a portion of their outstanding debt forgiven in exchange for deeding the property back. This can provide financial relief to the borrower while still satisfying the lender's claim. It's important to note that each situation is unique, and options available to borrowers may vary based on their specific circumstances and the lender's willingness to engage in alternative solutions to foreclosure. Exploring these options with the assistance of legal and financial professionals is crucial to making informed decisions and potentially mitigating the impact of financial distress.Cuyahoga County, Ohio, is one of the most populous counties in the state and encompasses a diverse range of communities, including Cleveland, the county seat. In cases where homeowners are facing financial difficulties and are unable to keep up with their mortgage payments, they may consider options like a "Borrower's Deed in Lieu of Foreclosure" to prevent foreclosure. A Borrower's Deed in Lieu of Foreclosure essentially involves the borrower voluntarily deeding their property to the mortgage lender, thereby avoiding the lengthy foreclosure process. This option allows homeowners to avoid the negative consequences associated with foreclosure and potentially negotiate more favorable terms. The Cuyahoga County Clerk of Courts, alongside various financial institutions and legal entities, facilitates the process to ensure transparency and fairness to both borrowers and lenders. The offer made by the borrower in this case is to voluntarily transfer the property back to the lender, releasing them from their mortgage obligation. Different types of Cuyahoga Ohio Offers by Borrower of Deed in Lieu of Foreclosure may include: 1. Standard Deed in Lieu: This is the most common type, where the borrower simply transfers the property back to the lender and walks away from the mortgage obligation. 2. Assumption Deed in Lieu: In this scenario, the lender may allow a third party to assume the mortgage loan and take responsibility for the property, rather than the borrower directly deeding it back. This option can be helpful if there is a qualified buyer available. 3. Negotiated Debt Forgiveness: In some cases, the borrower may negotiate with the lender to have a portion of their outstanding debt forgiven in exchange for deeding the property back. This can provide financial relief to the borrower while still satisfying the lender's claim. It's important to note that each situation is unique, and options available to borrowers may vary based on their specific circumstances and the lender's willingness to engage in alternative solutions to foreclosure. Exploring these options with the assistance of legal and financial professionals is crucial to making informed decisions and potentially mitigating the impact of financial distress.