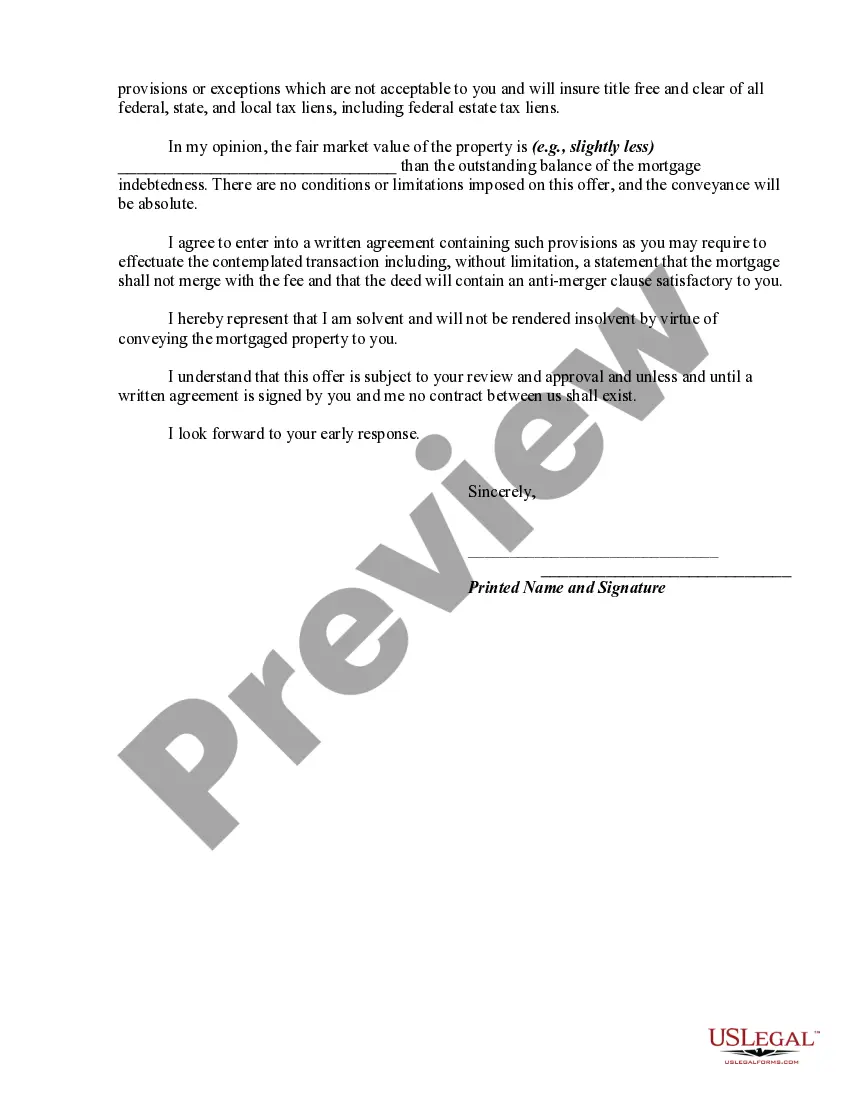

A deed in lieu of foreclosure is a method sometimes used by a lienholder on property to avoid a lengthy and expensive foreclosure process, with a deed in lieu of foreclosure a foreclosing lienholder agrees to have the ownership interest transferred to the bank/lienholder as payment in full. The debtor basically deeds the property to the bank instead of them paying for foreclosure proceedings. Therefore, if a debtor fails to make mortgage payments and the bank is about to foreclose on the property, the deed in lieu of foreclosure is an option that chooses to give the bank ownership of the property rather than having the bank use the legal process of foreclosure.

Maricopa, Arizona Offer by Borrower of Deed in Lieu of Foreclosure: A Deed in Lieu of Foreclosure is a legal agreement between a borrower and a lender that allows the borrower to voluntarily transfer the title of their property to the lender, instead of going through a foreclosure process. Maricopa, Arizona offers this option to borrowers who are facing financial hardship and are unable to keep up with mortgage payments. This allows borrowers to avoid the negative impact of a foreclosure on their credit score and potentially save them from the stress and uncertainties associated with foreclosure. There are different types of Maricopa, Arizona Offers by Borrower of Deed in Lieu of Foreclosure: 1. Traditional Deed in Lieu of Foreclosure: This is the standard type of Deed in Lieu arrangement where the borrower willingly transfers the property title to the lender in exchange for the lender releasing them from the mortgage debt. The borrower must meet specific eligibility criteria set by both state and lender. 2. Cash for Keys: In some cases, lenders might offer borrowers a cash incentive to voluntarily transfer the property through a Deed in Lieu of Foreclosure. This incentive helps cover moving expenses, find alternative housing, or pay off other debts. Cash for Keys can potentially be a win-win solution for both the lender and the borrower. 3. Short Sale Deed in Lieu: In situations where the property is worth less than the outstanding mortgage balance, a Short Sale Deed in Lieu of Foreclosure can be considered. In this scenario, the lender agrees to accept the fair market value of the property or a predetermined amount, rather than initiating a foreclosure process. This option allows the borrower to avoid foreclosure and settle the debt. Maricopa, Arizona recognizes that borrowers facing financial distress may require alternatives to foreclosure, and a Deed in Lieu of Foreclosure is one such alternative. By exploring these options, borrowers can potentially protect their credit scores, reduce stress, and find a more beneficial resolution to their financial challenges.