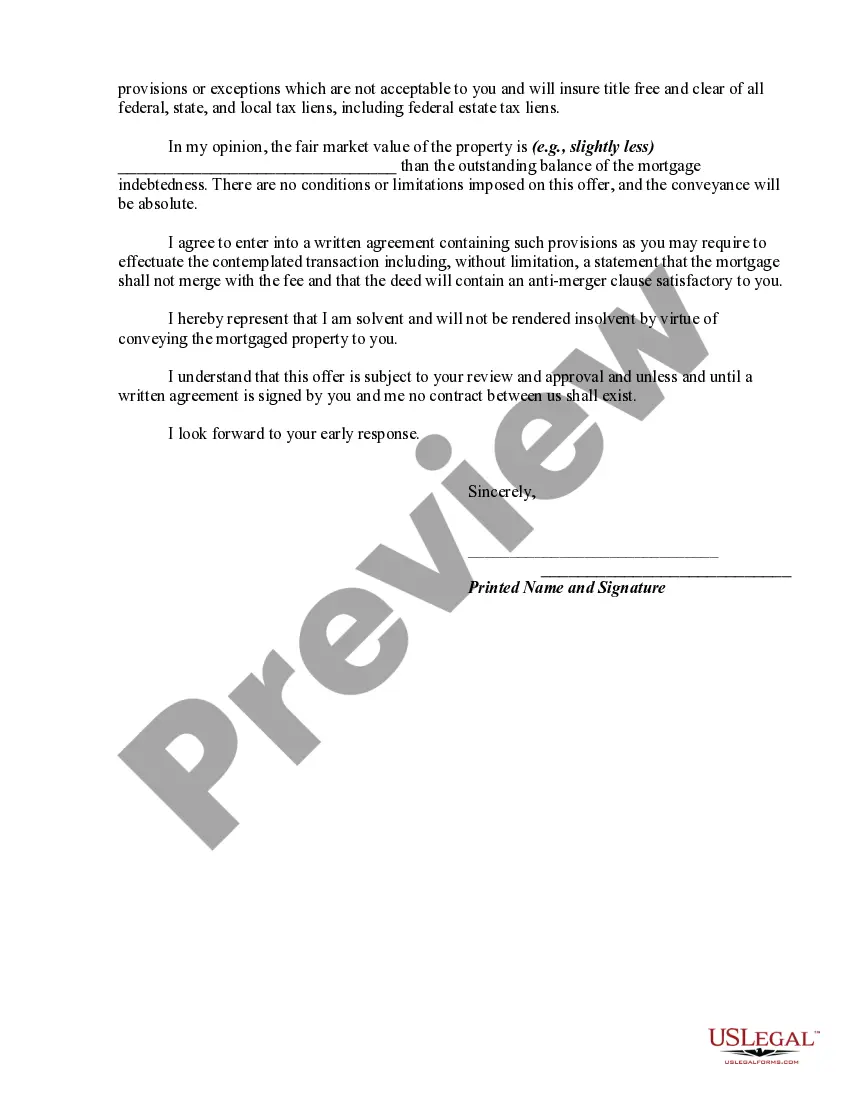

A deed in lieu of foreclosure is a method sometimes used by a lienholder on property to avoid a lengthy and expensive foreclosure process, with a deed in lieu of foreclosure a foreclosing lienholder agrees to have the ownership interest transferred to the bank/lienholder as payment in full. The debtor basically deeds the property to the bank instead of them paying for foreclosure proceedings. Therefore, if a debtor fails to make mortgage payments and the bank is about to foreclose on the property, the deed in lieu of foreclosure is an option that chooses to give the bank ownership of the property rather than having the bank use the legal process of foreclosure.

Mecklenburg North Carolina offers various options for borrowers facing foreclosure, including the option of a Deed in Lieu of Foreclosure. This legal agreement allows the borrower to voluntarily transfer the ownership of their property to the lender instead of going through the lengthy foreclosure process. By doing so, the borrower can avoid the negative consequences of foreclosure, such as damaging their credit score. In Mecklenburg County, there are different types of Deed in Lieu of Foreclosure offers that borrowers can consider based on their specific circumstances. These options include: 1. Traditional Deed in Lieu of Foreclosure: This is the standard agreement where the borrower willingly surrenders the property's title to the lender. The lender will then release the borrower from their mortgage obligation, effectively canceling the loan. This option is typically pursued when the borrower is unable to keep up with their mortgage payments and has exhausted other alternatives. 2. Cash for Keys: In some cases, lenders may offer borrowers a financial incentive to voluntarily leave the property. This arrangement involves the borrower receiving a lump sum payment from the lender in exchange for swiftly vacating the premises and leaving the property in good condition. Cash for Keys can provide borrowers with additional funds to help them transition to a new living situation. 3. Consent Deed in Lieu of Foreclosure: Under this option, the lender agrees to accept the deed to the property even if the borrower still owes more on the mortgage than the property's current value. This alternative can be beneficial for borrowers whose homes have depreciated significantly, preventing them from selling the property for an amount that covers their outstanding loan balance. 4. Cooperative Deed in Lieu of Foreclosure: This type of agreement involves the borrower and lender working together to find a mutually agreeable solution. The borrower cooperates with the lender in listing and marketing the property for sale, while the lender agrees to accept the deed in lieu of foreclosure once a suitable buyer is found. This arrangement allows the borrower to actively participate in the sale process and potentially avoid the credit repercussions of a foreclosure. Borrowers considering a Deed in Lieu of Foreclosure in Mecklenburg North Carolina are advised to consult with a qualified real estate attorney or a housing counseling agency to understand the legal implications, potential tax consequences, and the impact on their credit. Each situation is unique, and it is crucial for borrowers to carefully assess their options before entering into any agreement.