This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

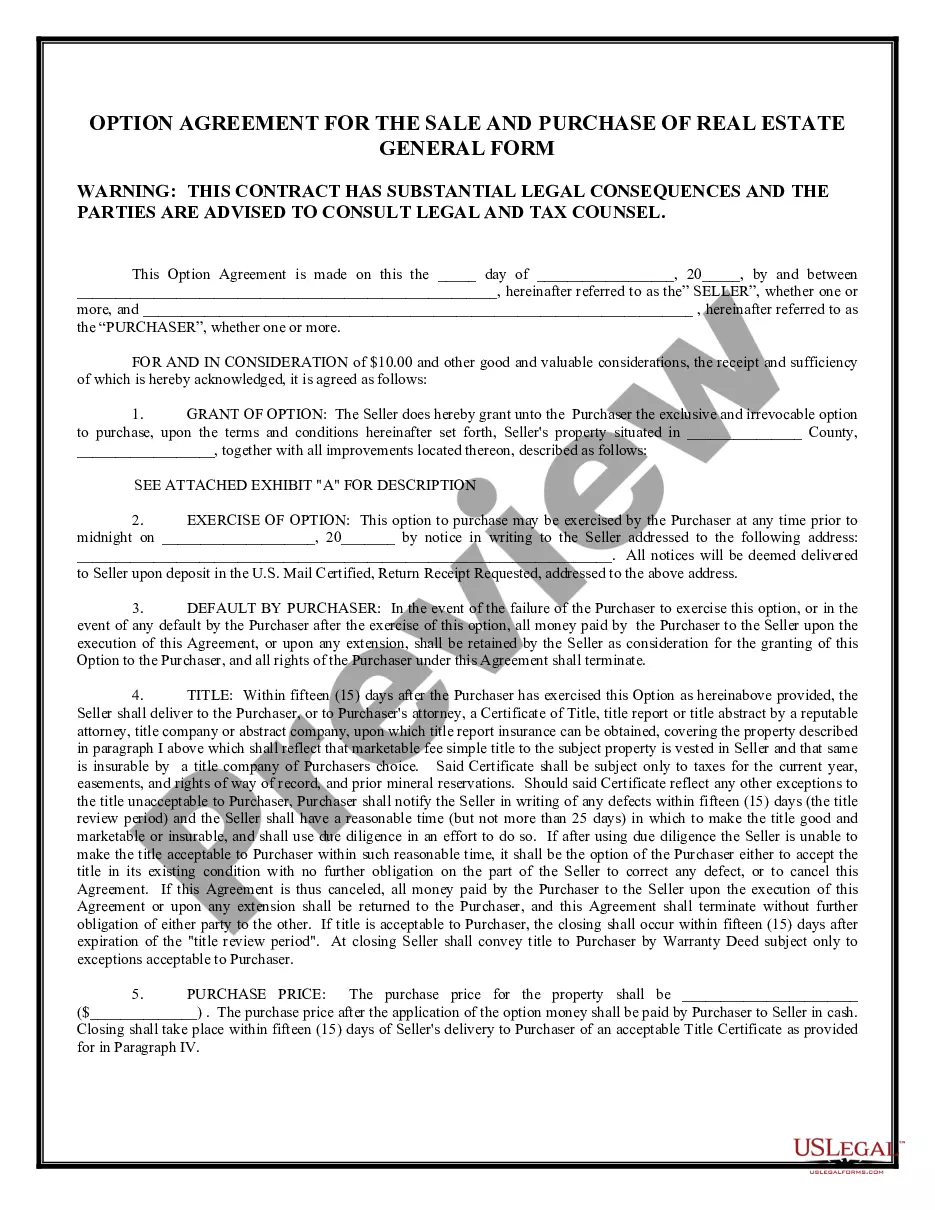

The San Diego California Contract for the Sale of Residential Property Assuming Existing Loan and Giving Seller Purchase Money Mortgage or Deed of Trust is a legal document that outlines the terms and conditions for the sale of a residential property in San Diego, California. This contract is used when a buyer agrees to assume the existing loan on the property and the seller agrees to provide a purchase money mortgage or deed of trust to facilitate the transaction. The contract includes various key elements and provisions to protect the interests of both the buyer and the seller. It clearly defines the parties involved, the property details, the purchase price, and the terms of the assumption of the existing loan. The assumption of the loan is subject to the buyer's qualification and approval from the lender. Additionally, the contract lays out the terms and conditions of the purchase money mortgage or deed of trust provided by the seller. This aspect of the contract specifies the amount of the mortgage, the interest rate, the repayment terms, and any additional provisions agreed upon by the parties. There are several types of San Diego California Contracts for the Sale of Residential Property Assuming Existing Loan and Giving Seller Purchase Money Mortgage or Deed of Trust, which may vary based on specific requirements or preferences of the buyer and seller. These may include: 1. Fixed-Rate Mortgage Contract: This type of contract involves a fixed interest rate for the purchase money mortgage or deed of trust, ensuring a consistent monthly payment over the loan term. 2. Adjustable-Rate Mortgage Contract: In this contract, the interest rate on the purchase money mortgage or deed of trust can fluctuate based on market conditions. This offers potential changes in monthly payments during the loan term. 3. Balloon Payment Contract: This type of contract includes a large payment due at the end of the loan term. The buyer agrees to make regular payments during the loan period, with the final balloon payment at the end. 4. Assumable Loan Contract: This contract allows the buyer to assume the existing loan on the property with the lender's approval, without the need for a new mortgage. The seller is released from the liability of the loan, transferring the responsibility to the buyer. The San Diego California Contract for the Sale of Residential Property Assuming Existing Loan and Giving Seller Purchase Money Mortgage or Deed of Trust is an essential legal document that safeguards the interests of both the buyer and the seller during the property sale transaction. It ensures the smooth transfer of ownership while addressing the financial aspects associated with the existing loan and the purchase money mortgage or deed of trust.